How much money do you need to start a commercial bank depends on three buckets: startup costs, regulatory capital, and balance sheet funding In the researched assumptions, the operating cost floor is about $98K per month, made up of $455K in fixed monthly costs and $525K in monthly disclosed senior payroll That excludes facility buildout, core banking implementation, cybersecurity setup, legal and charter work, and any required capital The first operating year also assumes $185M in loans, $33M in other earning assets, and $125M in liabilities, so a de novo bank startup budget must model both launch spend and balance sheet scale

Calculate Fuding Needs

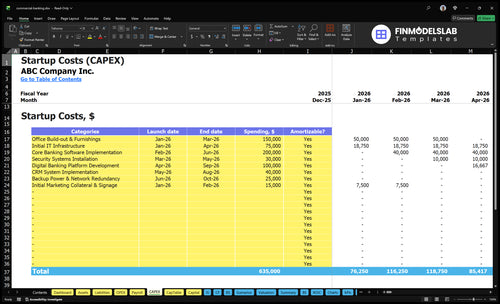

Startup cost summary

This table breaks out startup assets and excluded funding needs for a commercial banking launch.

Highlighted CAPEX$555,000Base planning example

Excluded cash needs$128,010,000Outside CAPEX total

Regulatory Capital, Deposits, and Liquidity Reserve

$128,010,000

Regulatory capital, deposit funding, and loan portfolio liquidity needs

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a commercial banking launch.

!

What this excludes Excludes deposits, regulatory capital, debt service, loan portfolio funding, working capital, payroll runway, recurring rent, and monthly overhead. Recurring tech lines are excluded too, including the $15K monthly core banking system license and $4.5K monthly cybersecurity subscriptions.

What does the Commercial Banking model screenshot show?

Banking setup costs change fast as you move from charter prep to a live market launch. Staff, systems, compliance, and funding all scale up together.

Lean, Base, and Full launch cost bands for commercial banking

Scenario

Lean LaunchOrganizing-stage

Base LaunchSingle-market launch

Full LaunchFull-service launch

Launch model

This is an organizing-stage model built around charter prep, policy work, and vendor selection before a broad launch.

This is a single-market launch with one office, core banking, and the disclosed senior team in place.

This is a full-service launch with broader staffing, deeper compliance, treasury services, and a wider tech stack.

Typical setup

Use limited staff and a narrow system stack, with spend staged into legal, approvals, and vendor work.

Plan around the known $98k monthly baseline burn with one office, core banking license, cybersecurity, and the disclosed senior team.

Add more relationship, credit, treasury, compliance, and operations capacity plus more systems spend.

Cost drivers

Charter prep

policy work

vendor selection

limited staff

One office

core banking license

cybersecurity

senior team

monthly burn

Broader staffing

treasury services

compliance

technology scope

capex buildout

Planning rangeCAPEX only

$100,000 - $250,000Lower capital

$750,000 - $1,500,000Mid capital

$1,500,000 - $3,000,000Higher capital

Best fit

Best for founders testing a banking concept before opening a market.

Best for teams ready to open in one market and fund early runway.

Best for operators building a fuller commercial banking platform from day one.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes or bids, so use them to size funding and test launch scope.

How Much Capital Do You Need To Start A Commercial Bank?

For Commercial Banking, total funding is not the same as startup costs: you need startup expenses, CAPEX, liquidity, operating runway, balance sheet funding, and separate regulatory capital. The disclosed baseline burn is $98K/month, while Year 1 assumptions include $185M in loans, $33M in other earning assets, and $125M in liabilities, so size the full capital stack around What Is The Main Goal For Growth And Success Of Your Commercial Banking Business?.

Capital buckets

Cover $98K/month baseline burn

Fund startup expenses and CAPEX

Plan liquidity before loan growth

Separate regulatory capital from CAPEX

Balance sheet

Support $185M Year 1 loans

Add $33M other earning assets

Model $125M liabilities

Track $455K overhead plus $525K payroll

How Should A Commercial Bank Startup Funding Plan Be Built?

A commercial bank startup funding plan should tie startup costs, CAPEX, the capital raise, and the staffing ramp to deposit growth, loan growth, and the interest spread. For Year 1, use the model inputs of $185M loans, $125M liabilities, and $33M other earning assets, which produce about $15.917M of interest income and roughly $2.588M of interest expense. The plan should also stage compliance timing and runway use, because the model should test timing, not imply licensing approval.

Year 1 model

Start with $185M loans.

Use $125M liabilities.

Add $33M other earning assets.

Show $15.917M income and $2.588M expense.

Funding plan checks

Match funding to startup costs.

Stage CAPEX with hiring.

Link deposits to loan growth.

Test timing, not licensing approval.

What Hidden Costs Of Starting A Commercial Bank Should Founders Budget For?

If you’re starting Commercial Banking, budget for the slow pre-open cash burn first: approval delays, examiner feedback cycles, compliance buildout, vendor due diligence, audit readiness, insurance, training, and payroll before revenue, and see How Much Does The Owner Of Commercial Banking Make? for context. The hard costs called out here include $3,000 a month for Federal Deposit Insurance Corporation insurance premiums, $35,000 a month for professional services, and $5,000 a month for marketing. What this does not cover is the balance sheet build: regulatory capital, liquidity reserves, deposit funding, and $185 million in Year 1 loan funding.

Pre-open cash costs

$3,000 monthly FDIC premiums

$35,000 monthly services retainer

$5,000 monthly marketing spend

Budget for training and payroll early

Excluded funding needs

Regulatory capital is not overhead

Liquidity reserves must stay on balance sheet

Deposit funding is separate from launch costs

Year 1 loan funding is $185 million

Key Takeaways

Charter planning needs board, counsel, and exam feedback.

Core tech costs start at $60K monthly.

Keep capital spending separate from rent and payroll.

Payroll alone is $630K yearly before add-ons.

Commercial Banking Core Five Startup Costs

Regulatory Formation And Chartering Startup Expense

Charter scope

Chartering spend is mostly legal counsel, regulatory consultants, application prep, board governance, policy drafting, and compliance program design. Treat Federal Deposit Insurance Corporation (FDIC) application preparation as a planning item only. Keep these costs separate from regulatory capital, which is needed to support opening, not to pay advisors or filing work.

Cost inputs

The estimate depends on the state or federal charter path, board readiness, and how many examiner feedback cycles you expect. Here’s the quick math: use counsel quotes, consultant scope, and month-based staffing for the pre-opening period. One line item covers application drafting; another covers organizing expenses and policy work.

Choose the charter path first

Price each workstream separately

Model feedback and rewrite cycles

Keep it lean

Save money by narrowing the scope before vendors start drafting. One lead counsel and one regulatory lead usually beat a wide team with overlapping work. The main waste is rework, so lock board materials early, clean up policy drafts before submission, and avoid paying twice for the same examiner response.

Approve one document owner

Reduce duplicate reviews

Track changes by version

Timing risk

Pre-opening timeline drives this cost fast. If the charter review runs longer, counsel, consultants, and board work keep billing before launch. Build the budget by month, not just by total, so you can see the cash hit from delayed feedback, board fixes, or a slower path to opening day.

Professional Services, Risk, Insurance, And Audit Startup Expense

Launch controls

$35K monthly professional services, plus $3K in Federal Deposit Insurance Corporation (FDIC) insurance premiums and $5K in general marketing, puts this launch bucket at about $43K per month or $516K a year. It covers auditors, accountants, outside compliance review, loan policy work, internal controls, bond coverage, vendor due diligence, and community outreach.

Estimate inputs

Price this as a pre-opening services block, not capex. Use months of coverage, fixed retainer quotes, the scope of audit-readiness work, and the number of vendor reviews or policy drafts needed before opening.

Count pre-open months

Separate one-time from recurring

Quote the review scope

Keep scope tight

Cut waste by splitting one-time filing work from recurring review, getting fixed-fee bids, and limiting marketing to launch needs. Don’t underbuy controls; weak policies, thin insurance, or shallow vendor checks can slow approval and deal flow. A clean file beats a cheap monthly bill.

Fix scope before signing

Ask for named deliverables

Review fees each month

Credibility work

Audit-readiness is part of opening because regulators, investors, and counterparties will look for policy drafts, internal controls, insurance, and board oversight before they trust the balance sheet. Build the review trail now, while the team is small and the workflow is still easy to fix.

Pre-Opening Staffing And Leadership Startup Expense

Not CAPEX

Pre-opening staff is working capital or a pre-opening expense, not CAPEX. For a commercial bank, the disclosed payroll floor starts with $250K for the CEO, $200K for the Chief Credit Officer, and $180K for the Head of Relationship Management, for $630K per year before taxes, benefits, and added hires.

What It Covers

This cost covers the pre-launch team: CEO, CFO, compliance, operations, lending, deposit operations, risk, IT, recruiting, onboarding, and training. Here’s the quick math: the three disclosed salaries total $630K a year, or about $52.5K per month. Add payroll taxes, benefits, and any extra hires to size the cash need.

Use salary quotes, not guesses.

Map hires to launch dates.

Budget for onboarding weeks.

How To Control It

Keep the team lean until the charter, systems, and policies are ready. Delay non-core hires, use contractors for short gaps, and tie bonuses to launch milestones. The big mistake is counting salary as one-time CAPEX; it hits cash every month. If onboarding drags, runway shortens fast.

Hire in launch sequence.

Track burn monthly.

Do not overbuild headcount.

Cash Runway Check

This staffing line should sit in the launch cash plan beside chartering, systems, and legal spend. If the bank wants a pre-opening runway, use the $630K salary base plus taxes, benefits, recruiting fees, onboarding, and training, then layer in the months of coverage needed before first revenue.

Premises, Branch Buildout, And Security Startup Expense

Branch buildout scope

Branch buildout is the physical CAPEX: leased office improvements, customer service space, teller or cash-handling areas, access control, surveillance, alarms, signage, furniture, and equipment. Keep that separate from rent deposits and recurring occupancy costs. The budget needs quotes for square feet, finish levels, security hardware, and fit-out work, plus a clear list of what is included in the landlord’s shell versus tenant work.

Occupancy costs

For planning, use $12K monthly branch office rent and $25K monthly utilities and maintenance as recurring occupancy costs, not startup buildout. Here’s the quick math: if launch takes 6 months before full activity, occupancy alone can run $222K before payroll and tech. That means the pre-opening budget needs both rent runway and fit-out cash.

Separate deposit from buildout spend

Budget months before opening

Track rent and utilities monthly

Security and fit-out

Security drives a real slice of the bill because cash-handling branches need tighter controls than a standard office. Ask for quotes on doors, cameras, alarms, badge access, and any vault-related work. The main cost drivers are branch size, cash volume, service model, and whether the space needs a teller line or a full secure back office.

Price cameras and alarms by site

Match controls to cash volume

Avoid overbuilding unused space

Launch questions

Before you spend, lock four choices: one-site launch or future branches, expected cash handling, target branch size, and whether a vault is needed. If the first site is a test market, keep the fit-out lean and leave room for expansion. The wrong layout is expensive to fix after opening, especially once walls, security, and equipment are installed.

Banking Technology And Cybersecurity Startup Expense

Monthly tech run rate

Core banking and cybersecurity are the biggest recurring lines here. At $15K a month for the core system and $45K a month for security subscriptions from Month 1 through Month 60, the base run rate is $60K a month, or $3.6M over 60 months, before transaction-linked fees and one-time setup.

Startup build costs

One-time spend covers implementation fees, vendor onboarding, data protection setup, disaster recovery design, and any software you capitalize instead of expense. Here’s the quick math: separate upfront build costs from monthly subscriptions, then estimate by quote, user count, systems connected, and months of rollout. That keeps launch cash needs clean.

Separate setup from subscriptions

Get quotes by module

Track capitalized software

Transaction-linked fees

Treasury management and loan servicing add variable cost in Year 1. Use transaction volume, service mix, and fee schedules to estimate the load: 30% for treasury management and 40% for loan servicing. What this estimate hides is volume growth, so model these as a percent of activity, not a flat monthly number.

Model by transaction volume

Use separate fee buckets

Watch Year 1 mix shifts

Control the burn

Cut cost by staging launch in phases: core banking first, then online banking, treasury, and payment links after controls are stable. Ask for implementation scope in writing, push vendor onboarding into milestones, and avoid paying for unused modules. If security tools are overbuilt on day one, you’ll burn cash fast without improving day-one readiness.