You’re not just paying to build credit risk analysis software you’re funding a secure lending analytics business through launch and early sales Based on the researched model, known startup planning inputs include $20,000 in initial dev/test server hardware CAPEX, $605,000 in Year 1 payroll, $150,000 in Year 1 marketing, and $9,100 per month in fixed overhead That puts the first operating year budget at about $884,200 before revenue-linked cloud, data, commissions, processing fees, and working capital The operating model also assumes $1,500 CAC, 20% visitor-to-trial conversion, and 150% trial-to-paid conversion in Year 1

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a credit risk analysis software launch.

!

CAPEX only This calculator covers capitalized startup build costs only. It excludes pre-opening expenses, payroll runway, deposits, inventory, working capital, debt service, taxes, sales spend, recurring data subscriptions, post-launch cloud usage, and other operating costs.

Calculate Fuding Needs

Startup cost summary

This table separates startup CAPEX from excluded cash needs so you can size launch funding, build costs, and runway.

Highlighted CAPEX$55,000Base planning example

Excluded cash needs$488,000Outside CAPEX total

Funding need$543,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

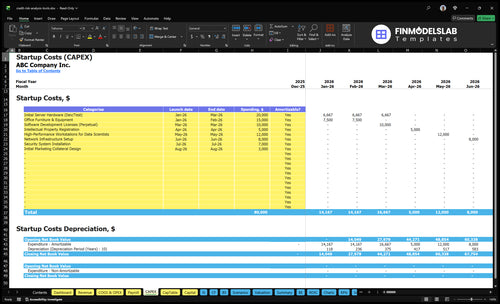

Initial Server Hardware (Dev/Test)

$20,000

Dev/test server build and launch setup

Yes

Software Development Licenses (Perpetual)

$10,000

Build tools and release workflow licenses

Yes

Intellectual Property Registration

$5,000

Filing and legal registration work

Yes

High-Performance Workstations for Data Scientists

$12,000

Staff readiness and analyst equipment

Yes

Security System Installation

$8,000

Physical and systems security setup

Yes

Working Capital Reserve

$488,000

Year 1 payroll, marketing, and monthly overhead to breakeven

Scenario scale matters here because credit risk software can start as a narrow scoring tool or grow into an enterprise platform. More data sources, integrations, and security work push cash needs up fast.

Lean MVP, commercial launch, and enterprise-ready cost bands

Scenario

Lean LaunchMVP pilot

Base LaunchCommercial launch

Full LaunchEnterprise-ready

Launch model

A narrow MVP pilot that scores a small set of borrowers with simple rules and few integrations.

A commercial launch built on the model inputs, with standard scoring, core integrations, and a sales motion.

An enterprise-ready platform with deeper compliance support, richer data coverage, and implementation services.

Typical setup

Use one or two data sources, a basic model, and a small pilot team.

Use the modeled Year 1 build: $20,000 CAPEX, $605,000 payroll, $150,000 marketing, and $109,200 fixed overhead.

Add more feeds, audit-ready controls, hardened security, and onboarding help for larger lenders.

Cost drivers

Limited data sources

basic scoring logic

light integrations

smaller team

minimal compliance

Known CAPEX

Year 1 payroll

marketing budget

fixed overhead

standard cloud and data fees

Compliance support

more data sources

security stack

implementation support

larger team

Planning rangeCAPEX only

$250,000 - $500,000Pilot budget

$850,000 - $950,000Launch budget

$1,100,000 - $1,600,000Enterprise budget

Best fit

Best for a founder testing lender demand with small banks, credit unions, or niche lenders.

Best for a team ready to sell to growth-stage lenders that want a clear pilot-to-contract path.

Best for an experienced team targeting regulated lenders that need enterprise onboarding and stronger controls.

!

Planning note: These ranges are researched planning assumptions, not vendor quotes or fixed budgets.

How much money do I need to start credit risk analysis software?

For Credit Risk Analysis Software, plan on at least $884,200 for Year 1 launch readiness before revenue-linked costs and working capital, not just the $20,000 build spend; tie that funding to What Is The Most Critical Metric To Measure The Success Of Your Credit Risk Analysis Software?. Here’s the quick math: $20,000 + $605,000 + $150,000 + $109,200 = $884,200, and revenue-linked costs add 170% of Year 1 revenue.

Base Funding

CAPEX: $20,000

Payroll: $605,000

Marketing: $150,000

Fixed overhead: $109,200

Launch Cushion

Cloud costs: 50% of revenue

Data costs: 60% of revenue

Commissions: 40% of revenue

Processing overage: 20% of revenue

What are the biggest cost drivers for credit risk analysis software?

Year 1 staffing is the biggest cost driver in Credit Risk Analysis Software: the listed team totals $605,000 in payroll before data or cloud spend. After that, data acquisition and licensing at 60% of revenue and cloud hosting at 50% of revenue are the next heavy costs. The scoring engine gets expensive fast when you add bureau files, alternative data, loan performance datasets, testing, audit logs, and repeatable model documentation.

Year 1 payroll

CEO: $180,000

Lead Data Scientist: $150,000

Senior Software Engineer: $140,000

Sales Manager: $100,000

Half-time Customer Success Manager: $35,000

Variable cost drivers

Data licensing: 60% of revenue

Cloud hosting: 50% of revenue

Data inputs: bureau and alternative files

Compliance load: testing and audit logs

What hidden costs come with starting credit risk analysis software?

Starting Credit Risk Analysis Software usually costs more than the build itself, because you need legal review, privacy policies, data-use agreements, FCRA, ECOA, and GLBA review, plus adverse-action workflow support before launch; for a quick owner-income benchmark, see How Much Does The Owner Of Credit Risk Analysis Software Typically Make?. The recurring base is already $4,200 per month from a $1,000 legal and accounting retainer, $500 insurance, $700 cybersecurity subscriptions, and $2,000 in R&D software and tools, before data trials, model documentation, onboarding, and the $35,000 half-time Year 1 Customer Success Manager.

Pre-launch costs

Legal review before any sale

Privacy and data-use agreements

FCRA, ECOA, GLBA review

Model docs and data trials

Monthly burn

$4,200 fixed monthly base

$35,000 half-time CSM for onboarding

Customer onboarding needs real capacity

Runway must cover post-launch delays

Key Takeaways

Build and server setup should be capitalized when allowed.

Data licensing and usage fees scale with revenue.

Compliance needs contracts, governance, and monthly legal support.

Payroll, sales, and marketing drive first-year cash burn.

Credit Risk Analysis Software Core Five Startup Costs

Core Product Development Startup Expense

MVP Build

Core product development is usually CAPEX or capitalized software if your accounting policy allows it. Budget for MVP build, borrower risk workflows, dashboard design, admin tools, scoring logic, QA, and production readiness, plus $20,000 of dev/test server hardware as setup CAPEX. Tie staffing to $150,000 for a Lead Data Scientist and $140,000 for a Senior Software Engineer.

Cost Inputs

Estimate this cost from scope, not guesses: model complexity, number of borrower workflows, lender dashboard depth, API needs, QA scope, and launch readiness. The fastest way to overspend is to build extra screens or edge cases before the pilot needs are clear. One clean rule: more workflow branches means more build hours and more testing.

Count MVP borrower workflows

Map required API links

Define QA pass criteria

Scope Control

Keep the first release tight so the team can ship, test, and harden the product without wasting build time. Start with the minimum dashboard depth, the minimum scoring logic, and the minimum admin tools needed for pilots. That cuts rework, but only if security, audit trails, and lender-facing explanations stay in scope.

Launch Check

Production readiness should cover QA sign-off, error handling, access controls, and release checks before any pilot goes live. If the model needs more borrower data, more rule layers, or more explanation text, the budget rises fast because each piece adds review time and test cycles. The key question is simple: what must work on day one, and what can wait?

Staffing, Implementation, And Launch Readiness Startup Expense

Launch team

Launch staffing covers founders, a Lead Data Scientist, a Senior Software Engineer, compliance support, customer success setup, pilot onboarding materials, a website, demos, and initial sales outreach. Treat founder pay and ongoing payroll as working capital unless you book pre-opening contractor spend. For Year 1, the payroll anchor is $605,000.

Year 1 budget

The Year 1 payroll total splits into CEO $180,000, Lead Data Scientist $150,000, Senior Software Engineer $140,000, Sales Manager $100,000, and half-time Customer Success Manager $35,000. Add a $150,000 marketing budget and $1,500 CAC; here’s the quick math, that budget supports about 100 customers if CAC holds. Check the funnel assumptions before launch.

Launch math

Use the stated funnel as a planning check: 20% visitor-to-trial and 150% trial-to-paid conversion. That second rate needs a clear definition before pilots, because it can hide double counting or expansion revenue. Keep sales commissions at 40% of revenue, and budget the team around that cut so gross margin isn’t overstated.

Pre-launch control

Keep the build tight: one website, one demo flow, one pilot package, and one customer success script before you spend on scale. If onboarding drags, payroll burns before revenue lands, so the real risk is timing, not just headcount. That makes launch readiness a cash plan, not just a hiring plan.

Compliance, Legal, And Model Governance Startup Expense

Prelaunch Legal

Use this as a pre-launch gate, not legal advice. Budget $1,000/month for legal and accounting retainer, or $12,000/year, to cover entity setup, customer contracts, privacy policies, data-use agreements, FCRA, ECOA fair lending, GLBA safeguards, adverse-action review, and model documentation. Put the work in place before launch so lender and vendor paperwork is ready.

Cost Inputs

Size this line by months of coverage, number of contracts, number of vendor agreements, and the scope of model governance docs for borrower default risk logic and lender-facing explanations. The legal review is a planning category only, and it does not guarantee regulatory approval or customer acceptance.

Count pre-launch agreements first

Price 12 months of coverage

Separate setup from ongoing support

Spend Control

Cut waste by drafting core contracts and data-use terms once, then reusing them across pilots with counsel review. Keep model documentation tight: one score explanation, one adverse-action flow, one data map. Don’t skip lender-facing explanations; that often triggers rework and pushes compliance spend higher than the first quote.

Reuse contract templates

Review adverse-action language early

Keep one data map

Review Limits

Clean paperwork still won’t guarantee lender buy-in. Compliance review lowers risk, but it does not ensure approval or customer acceptance, so keep the $1,000/month retainer active and align the model file, disclosures, and underwriting logic before the first pilot.

Data Licensing And Integration Startup Expense

Data Scope

This budget covers credit bureau access, alternative data, bank transaction data, and loan performance feeds, plus API setup, testing, and data governance. Split the spend into one-time integration work and recurring data charges. In Year 1, model acquisition and licensing at 60% of revenue, with usage-based processing overage at 20%.

Pricing Ladder

Price usage by tier, not by guesswork. Plan for 50 Basic transactions at $150 each, 200 Pro at $100, and 1,000 Enterprise at $75. Here’s the quick math: transaction revenue depends on mix, but the pricing ladder should match volume, latency, and data depth.

Setup Costs

One-time setup pays for data mapping, vendor connections, testing, and controls. Recurring spend pays for feeds, pulls, and overages. Keep those lines separate in the model, or you’ll overstate launch cash needs. By Year 5, data acquisition and licensing should fall to 50% of revenue if volume scales and vendor terms improve.

Governance

Data governance matters because lenders will ask how each score is built and refreshed. Lock access, log every pull, and document source rules before pilots start. The main mistake is buying broad data too early; phase in only the fields you use, then trim idle feeds and high-overage calls.

Security, Cloud, And Reliability Startup Expense

Setup Costs

The first check is setup, not monthly cloud spend. Budget $20,000 for dev/test server hardware as CAPEX, then treat encryption, access controls, logging, monitoring, backups, and SOC 2 readiness as separate launch work. Lenders want proof of audit logs, uptime monitoring, and data protection before pilots, because those controls show borrower data is handled safely.

Monthly Run Rate

Separate build costs from recurring spend. Use cloud hosting and infrastructure at 50% of revenue in Year 1, declining to 40% by Year 5. Add $700 per month for cybersecurity subscriptions and $1,500 per month for general software licenses. The key inputs are revenue, months live, and how fast pilot traffic grows.

Model cloud off revenue.

Keep subscriptions monthly.

Resize after pilot usage.

Keep It Lean

Keep controls lean in dev/test, then turn on logging, backups, and access reviews before pilots. Don’t buy duplicate tools or overbuild cloud capacity too early. The best savings come from matching security tools to live workflows and trimming unused capacity after each pilot, while keeping the required controls in place.

Use one tool per control.

Review spend after each pilot.

Drop idle cloud resources fast.

Pilot Gate

Before a pilot, lenders expect access controls, audit logs, uptime monitoring, encryption, backups, and documented data protection. Penetration testing and SOC 2 readiness help prove the platform is reliable enough for borrower data. If these are missing, the buyer adds more risk review and the sales cycle slows.