Credit Risk Assessment Startup Costs: $80K+ CAPEX And $11M Runway

Plan for at least $80,000 in listed CAPEX and about $1105 million in first operating year funding before revenue-linked data, cloud, commission, and validation costs This researched planning view covers software buildout readiness, data access, compliance, model validation, security, staffing, and sales launch, but it is not a vendor quote or lender-specific legal guidance The outcome is a startup budget that separates CAPEX, pre-opening expenses, working capital runway, and total funding need

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for a credit risk assessment service, before payroll and other operating cash needs.

!

CAPEX scope note This calculator excludes monthly payroll, data subscriptions, cloud usage, insurance premiums, marketing, working capital, deposits, debt service, and inventory because they are not capitalized startup assets. Capitalized software development depends on accounting policy and build scope.

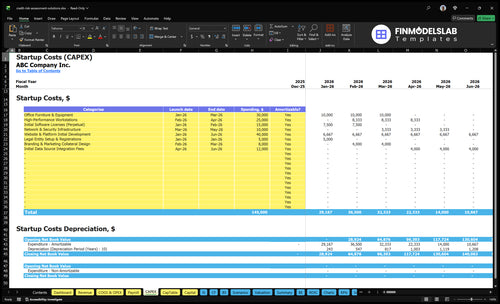

What does this CAPEX screenshot show?

This Credit Risk Assessment model screenshot shows CAPEX: startup costs, launch timing, amounts, and depreciation/amortization; review assumptions now.

Screenshot highlights

$80k CAPEX listed

Launch timing shown

Pricing tiers validated

Credit Risk Assessment Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

How much money do I need to start a credit risk assessment company?

You need about $1.105 million to start a Credit Risk Assessment company for the first operating year before revenue-linked costs. For what drives success after launch, tie this budget to What Is The Most Important Indicator For Credit Risk Assessment Business Success?, because the right spend depends on use case, customer type, data access, compliance burden, and enterprise sales timing.

Base budget

$80,000 CAPEX, about 7.2%

$695,000 wages, about 62.9%

$180,000 fixed overhead, about 16.3%

$150,000 marketing, about 13.6%

Launch choice

Lean advisory can defer automation

Platform needs data integrations early

Compliance and model governance stay required

Enterprise sales timing raises cash need

How should I fund a credit risk assessment startup after estimating costs?

Fund Credit Risk Assessment with at least $1.105 million before revenue-linked costs, then add a working-capital buffer sized to sales-cycle length and customer onboarding timing. Price Year 1 around $150 subscription tiers, $180 usage reports, $120 API packages, and $300 premium add-ons, with $1,500 customer acquisition cost and a $150,000 marketing budget. Build break-even around gross margin after 12% data licensing, 5% cloud processing, 8% commissions, and 3% validation, and keep financing tied to runway, compliance milestones, and enterprise sales readiness.

Funding floor

$1.105 million first-year floor

Add working capital buffer

Size it to sales cycle

Use onboarding timing, too

Unit economics

$150 subscription tiers

$180 usage reports

$120 API packages

$300 premium add-ons

Why do credit bureau data integration costs and model development costs get expensive?

Credit Risk Assessment gets expensive because you pay for data rights, provider onboarding, API testing, certification, data mapping, sample file testing, security reviews, and usage-based fees; model work adds feature engineering, scoring logic, validation, documentation, monitoring design, and QA. Here’s the quick math: data acquisition and licensing are assumed at 12% of revenue in Year 1 and 6% by Year 5, while per-assessment model validation adds 3% of revenue in Year 1. Pricing still varies by provider, use case, volume, customer type, and certification requirements.

Data costs

Data rights and licensing drive spend.

Onboarding takes time and staff hours.

API tests and sample files add rework.

Security and certification slow launch.

Model costs

Feature engineering needs clean inputs.

Scoring logic needs repeated tuning.

Validation adds 3% in Year 1.

Monitoring and QA keep costs recurring.

Calculate Fuding Needs

Startup Cost Summary

This table shows startup CAPEX and excluded launch cash for a credit risk assessment service.

Highlighted CAPEX$122,000Base planning example

Excluded cash needs$672,000Outside CAPEX total

Funding need$794,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Website & Platform Initial Development

$40,000

Core platform build scope and model workflow complexity

Yes

Office Furniture & Equipment

$30,000

Workspace fit-out and equipment count

Yes

High-Performance Workstations

$25,000

Analyst and engineer workstation spec

Yes

Initial Software Licenses (Perpetual)

$15,000

License breadth and seat count

Yes

Initial Data Source Integration Fees

$12,000

Number of bureau and data integrations

Yes

Minimum Cash Buffer

$672,000

Month 1 to Month 6 payroll, fixed overhead, and launch spend before breakeven

No

Credit Risk Assessment Core Five Startup Costs

Software Platform And Analytics Buildout Startup Expense

Launch Build

The launch build should capitalize the scoring engine, user dashboards, APIs, rules engine, reporting workflows, QA testing, data ingestion, audit logs, and launch-ready architecture. Use $15,000 for perpetual software licenses and $25,000 for high-performance workstations. Treat the website and first platform build as a separate capitalized software input.

Estimate It

Estimate this line from vendor quotes, build months, and the scope locked for launch. The capitalized software amount should stand apart from recurring cloud spend, with base infrastructure at $3,000 per month and usage-based cloud processing at 5% of Year 1 revenue. That split keeps CAPEX clean.

Get license and workstation quotes.

Map launch features to modules.

Exclude cloud run-rate costs.

Keep Scope Tight

Keep savings in the launch scope, not in shortcuts. Freeze roadmap extras until after go-live, and do not push maintenance into startup CAPEX unless it is separately approved. The clean rule is simple: if the work is needed to launch, capitalize it; if it supports later upgrades, treat it as follow-on spend.

Approve changes in writing.

Delay nonlaunch features.

Track maintenance separately.

Run Cost Split

Future roadmap work and maintenance are not launch CAPEX unless separately approved. After launch, expect recurring $3,000 monthly base cloud infrastructure plus 5% of Year 1 revenue for cloud processing, so the real budget test is build cost versus run cost. That line should stay visible in every forecast.

Data Acquisition And Bureau Integration Startup Expense

Data Feed Costs

Data access is the live fuel for underwriting. Budget for bureau access, alternative data, data licensing, API setup, vendor onboarding, sample testing, security questionnaires, data mapping, and usage-based fees. For planning, hold 12% of revenue in Year 1, then 10%, 8%, 7%, and 6% in Years 2-5.

Budget Formula

Use revenue, not guesswork. Here’s the quick math: Year 1 data cost = 12% × revenue; that falls to 6% by Year 5. The budget moves with volume, permissible purpose, customer type, refresh frequency, and certification needs. Keep these as recurring operating spend, not launch CAPEX.

Cost Controls

Scope controls save real money. Start with the fewest data feeds that support approval decisions, then add sources only when they improve loss rate or approval rate. Cut sample-test churn by mapping fields early and batching security reviews. One missed rule can cost more than the feed.

Start with core bureau data

Batch vendor onboarding

Refresh only when needed

Recurring Spend

Treat recurring bureau and data fees as opex (operating expense), not CAPEX (capital spending). Only one-time integration work belongs in launch build cost; ongoing access, refreshes, and licensing keep hitting monthly cash flow. If lenders require production access or tighter certification, the budget moves up fast, so lock the data scope before launch.

Compliance, Legal, And Risk Governance Startup Expense

What It Covers

Compliance spend covers entity setup, customer contracts, privacy policy, data use terms, FCRA review, ECOA and fair lending review, adverse action workflow design, model governance documentation, and vendor terms. Scope depends on whether outputs affect consumer credit decisions, lender requirements, and the use case, so the first legal pass should map the exact decision path.

Year 1 Base

Here’s the quick math: $2,500 a month for legal and compliance support equals $30,000 a year, and a 0.5 FTE compliance analyst at $90,000 annual salary adds $45,000. That puts known Year 1 spend at $75,000 before filing fees, outside counsel spikes, or lender-specific redlines.

Keep It Tight

Use one template set for the first launch: one entity, one customer contract, one privacy policy, one data use addendum, and one vendor pack. Don’t pay for broad edits before a lender asks for them. The real savings come from narrowing the workflow, not from skipping the FCRA or fair lending review.

Scope Triggers

If the score influences underwriting, pricing, or adverse action notices, the legal load rises fast. Lender customers may ask for model governance documentation, vendor terms, and proof of fair lending review. That’s where the $75,000 base can climb, because each new use case adds lawyer hours and analyst time.

Cybersecurity, Cloud Infrastructure, And Audit-Readiness Startup Expense

Security setup

For a credit risk assessment startup, the first spend is the security setup, not just app code. The budget starts with $10,000 for network and security infrastructure CAPEX, then adds secure hosting, encryption, access controls, monitoring, backup systems, data retention controls, penetration testing, incident response planning, and SOC 2 readiness work.

Cloud run rate

Model cloud in two layers: a fixed $3,000 monthly base, plus usage-based processing at 5% of Year 1 revenue. Here’s the quick math: $3,000 x 12 = $36,000 before usage fees. Keep initial setup separate from recurring cloud, monitoring subscriptions, and formal audit costs.

Cost inputs

To price it, use months of coverage, workload volume, data retention period, and quote-backed tool counts. Security spend moves with production data access, application programming interfaces (APIs), and vendor review depth. If you skip backups or monitoring, you may save money upfront but raise incident and diligence risk later.

Keep it lean

Use one secure cloud stack, not separate tools for each client. Start with role-based access, encrypted storage, and tested backups, then add premium monitoring only when lender contracts require it. What this estimate hides: formal audits and enterprise vendor questionnaires can add real time and cost, even when software spend stays flat.

Expert Staffing And Model Validation Startup Expense

Team budget

Year 1 staffing runs $695,000: CEO $180,000, lead data scientist $160,000, senior software engineer $150,000, sales manager $120,000, 0.5 customer success manager $40,000, and 0.5 compliance analyst $45,000. That covers pre-launch readiness, not every future hire. Keep QA support and external validation resources separate so launch payroll stays clear.

Validation cost

Model validation is a usage cost, not fixed payroll. Plan for 3% of revenue in Year 1, then 1% by Year 5. Here’s the quick math: at $1 million of revenue, Year 1 validation is $30,000. Use assessment volume × validation rate, plus outside review when lenders want formal checks.

Hire timing

Treat launch staffing as readiness and Month 13 hires as scale. The first team proves the scoring model, sales motion, and compliance flow; later hires like a marketing specialist and data engineer belong after launch. One mistake is funding full headcount too early and starving validation, QA, and client onboarding.

Protect quality

Cut cost with contract validation and tight QA gates, but don’t trim the controls lenders inspect. Keep external validation, test scripts, and audit logs in the budget; they cost less than fixing model errors after go-live. The real lever is sequencing hires so payroll matches signed demand, not wishful pipeline.

Compare 3 Startup Cost Scenarios

Scenario table

Credit risk assessment costs rise as you add data feeds, compliance, security, and enterprise sales readiness. Lean keeps the build simple; Full assumes a deeper platform and bigger team.

Lean, base, and full launch cost bands for a credit risk assessment service

Scenario

Lean LaunchLow-automation prototype

Base LaunchModerate-automation platform

Full LaunchHigh-automation enterprise

Launch model

Founder-led advisory with a simple scoring prototype, limited automation, and a small set of data inputs.

Balanced subscription launch with moderate automation, standard reporting, and a small operating team.

Enterprise-ready platform with high automation, multiple data integrations, deeper controls, and a larger go-to-market team.

Typical setup

One core product, one or two data sources, light compliance review, and minimal infrastructure.

A working scoring platform with core integrations, the listed $80,000 CAPEX, $695,000 wages, $180,000 fixed overhead, and $150,000 marketing.

A broader build with more integrations, stronger security, deeper compliance work, and more sales and support capacity.

Cost drivers

Prototype build

founder-led sales

fewer data feeds

light compliance

lower CAPEX

CAPEX $80k

wages $695k

fixed overhead $180k

marketing $150k

Multi-source integrations

deeper compliance

stronger security

larger build

enterprise sales team

Planning rangeCAPEX only

$650,000 - $850,000Lowest burn

$1,050,000 - $1,200,000Model floor

$1,600,000 - $2,100,000Full build

Best fit

Best for a founder-led test with low automation, few data sources, and early buyers who only need a basic risk read.

Best for teams that need a usable product, several data sources, clear compliance, and customers ready for subscription pricing.

Best for enterprise buyers that want high automation, many data sources, strong compliance, and a polished rollout.

!

Planning note: These scenario ranges are researched planning assumptions, not exact vendor quotes or guaranteed budgets.

A minimum viable launch depends on how much automation you need, but the researched base floor is about $1105 million for the first operating year before revenue-linked costs That includes at least $80,000 in listed CAPEX, $695,000 in wages, and $150,000 in Year 1 marketing A lean advisory launch can defer some platform work, but not compliance or data governance

Working capital should cover the early ramp-up period because lender and fintech sales rarely close like small retail purchases The model carries $15,000 in monthly fixed overhead, about $57,917 in monthly Year 1 payroll, and a $150,000 annual marketing budget That means base cash burn can reach about $85,400 per month before revenue-linked data, cloud, commission, and validation costs

You may need provider approval before using bureau data in a production service, but approval requirements vary by provider, use case, volume, and customer type Do not budget from a universal quote In the model, data acquisition and licensing are treated as 12% of revenue in Year 1, while onboarding, testing, and security reviews should be budgeted before live customer delivery

For a platform-led credit risk assessment startup, the first critical hires are usually risk, data, and engineering roles The researched Year 1 team includes a lead data scientist at $160,000, senior software engineer at $150,000, and 05 compliance analyst at $45,000 If the launch is advisory-led, compliance review and model validation support may matter before a full engineering build

Early compliance should not be treated as a small filing cost The model includes a $2,500 monthly legal and compliance retainer, a 05 compliance analyst at $45,000 in Year 1, and $1,200 monthly accounting and audit services Scope rises if outputs affect consumer credit decisions, require adverse action workflows, or trigger lender-specific vendor reviews

About the author

Felix Ward

Entrepreneurship Researcher

Felix Ward is an entrepreneurship researcher at Financial Models Lab who focuses on expense and revenue planning for people opening a new small business. He turns practical business questions into clear planning steps, with a special focus on first-year business planning. Known for making business planning easier for non-finance readers, he writes in a calm, structured, and approachable way.

Choosing a selection results in a full page refresh.