Digital Banking Platform Startup Costs: $151M First-Year Runway

Digital Banking Platform

This digital banking platform cost breakdown separates build costs from operating runway and funding need The provided model shows $61,300 in monthly fixed costs and $775,000 in first-year payroll, or about $151 million before variable expenses, CAPEX, customer funds, regulatory capital, and one-time vendor implementation fees It covers technology, compliance, integrations, cybersecurity, launch readiness, CAPEX, pre-opening expenses, and working capital, but it is not a vendor quote or licensing promise

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets for a digital banking platform only, not operating runway or working capital.

!

CAPEX only This calculator excludes monthly SaaS, payroll, retainers, marketing, customer funds, deposits, regulatory capital, debt service, and working capital. Source data also shows $61,300 in monthly fixed costs and $775,000 in first-year payroll, which belong in pre-opening expenses, first-year runway, and total funding need, not CAPEX.

What hidden costs and working capital does a digital banking platform need?

A Digital Banking Platform needs three cash buckets: pre-opening setup, working capital, and regulated balance-sheet funding. For a quick read on owner economics, see How Much Does The Owner Of A Digital Banking Platform Typically Make?; the base model already carries $61,300 in monthly fixed costs and $775,000 in first-year payroll. The big mistake is treating customer deposits, regulatory capital, loan funding, and investment assets like normal startup expenses—they are not.

Hidden pre-opening costs

Pay for compliance audits

Set up fraud monitoring

Buy test environments

Run data security reviews

Working capital needs

Cover customer support readiness

Plan for cloud usage spikes

Meet vendor minimums

Carry insurance and incident response

Here’s the quick math: 15% customer acquisition cost pressure and 3% interchange fees paid both hit early cash flow, so launch spend should stay separate from core operating runway. The first-year model also assumes $30 million in deposits and $31 million in loans plus other interest-earning assets, which means funding and liquidity planning matter from day one.

How should a digital banking platform financial model support funding?

A Digital Banking Platform should show funding needs, not just product appeal: map CAPEX, startup costs, launch timing, hiring runway, and compliance spend into one cash plan, then tie that to deposit and loan growth. Use a $151 million first-year operating runway before variable expenses and CAPEX, with $61,300 in fixed monthly costs, and test Year 1 assumptions like a $11 million loan book, $20 million in other interest-earning assets, and $30 million in deposits. Keep revenue math plain: show 15% customer acquisition costs and 3% interchange fees paid, so investors can see cash need, timing, and risk fast.

Cash plan

$151 million runway

$61,300 fixed monthly cost

Launch timing by cash burn

Compliance costs by phase

Growth model

$11 million loan book

$20 million assets

$30 million deposits

15% CAC and 3% fees

What are the biggest costs to start a digital banking platform?

A Digital Banking Platform’s biggest startup costs are regulated compliance, secure engineering, banking integrations, cybersecurity, and experienced fintech talent. Here’s the quick math: first-year payroll is $775,000, plus $240,000 for the core banking platform license, $180,000 for cloud hosting, $96,000 for regulatory compliance fees, $72,000 for legal counsel, and $60,000 for data security software. Office rent at $4,000 a month is only $48,000 a year, so it is not the main cost driver.

Platform costs

$240,000 yearly core banking license

$180,000 yearly cloud hosting

$96,000 yearly compliance fees

$72,000 legal retainer

Team costs

CEO, $180,000

Head of Technology, $160,000

Lead Software Engineer, $140,000

Compliance Officer, $120,000

Calculate Fuding Needs

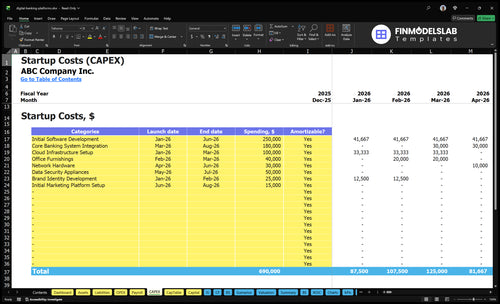

Startup cost summary

This table shows launch build costs for a digital banking platform and the separate cash reserve kept outside CAPEX.

Customer deposits, loan funding, and operating runway

No

Digital Banking Platform Core Five Startup Costs

Digital Banking Platform Development Startup Expense

Build Scope

This cost covers the own app, web portal, admin dashboards, onboarding flows, account workflows, payments UX, QA, release readiness, and internal controls. Start with the Year 1 build team inputs of $160,000 for the Head of Technology and $140,000 for the Lead Software Engineer, or $300,000 combined, before any vendor fees.

Run Rate

Here’s the quick math: the recurring stack is $20,000 a month for the core banking platform license plus $15,000 a month for cloud hosting, or $420,000 a year. Keep custom development separate from operating costs, and only capitalize eligible software if your accounting policy supports it.

Cost Control

Keep the launch narrow. Build only the first product set, then phase in extras after QA and release gates pass. Don't fold support, subscriptions, or maintenance into capitalized software. That keeps the budget clean and avoids overstating startup assets.

Accounting Split

Treat quote-backed implementation fees as possible capitalized software only when they are tied to eligible development work. Everything else—maintenance, hosting, support, and subscriptions—stays operating expense. That split matters because it changes startup cash burn, asset value, and how fast the build pays for itself.

Digital Banking Compliance Startup Expense

Compliance Base

Compliance spend for an all-digital bank starts with legal structure, Bank Secrecy Act (BSA) and anti-money laundering (AML), know your customer (KYC), know your business (KYB), consumer disclosures, privacy, risk policies, and audit readiness. The base inputs here are a Compliance Officer at $120,000, $8,000 monthly regulatory fees, and a $6,000 monthly legal retainer. That sets a $288,000 first-year floor before audits or one-time setup.

Cost Math

Here’s the quick math: $8,000 × 12 = $96,000, and $6,000 × 12 = $72,000. Add the $120,000 Compliance Officer, and you get $288,000 before any audits, policy drafting, or regulator-facing work. This is a fixed launch layer, so it belongs in the pre-opening budget, not in customer-growth spend.

Scope Check

Keep partner-bank compliance separate from charter work. A partner-bank model still needs review, but it is not the same as charter capital, licensing, or approval paths. Start with a narrow scope, because lending, deposits, cards, and business accounts can change filings, controls, and timing fast.

Which states launch first?

Any lending at launch?

Are deposits in scope?

Cards and business accounts?

Partner Bank

A partner bank can help with operations, but it does not replace your own compliance work. No regulatory approval is automatic, so document each product and state decision early. One clean checklist: products, states, lending, deposits, cards, and business accounts.

Banking Platform Integration Startup Expense

Integration scope

Banking as a service (BaaS) is third-party infrastructure that lets a fintech connect to banking tools through APIs. This startup cost covers links to partner bank systems, core banking or ledger services, ACH, debit card issuing, payment processors, identity checks, fraud tools, and reporting. The base model includes a $20,000 monthly core banking platform license, or $240,000 per year.

Cost inputs

Build the estimate from quote-backed line items: one-time implementation and certification fees, plus per-account, per-transaction, and monthly vendor charges. Do not treat customer funds or deposit balances as integration expense. The key decision is which rails launch in MVP versus later phases, because each rail adds setup work, review time, and ongoing cost.

One-time setup fees

Monthly license charges

Usage-based vendor fees

Keep the first launch tight

Start with only the rails needed for day-one accounts and transfers. That keeps you from paying for unused certifications and monthly minimums. If you add cards, fraud tools, or extra reporting later, the bill rises fast. What this estimate hides: partner-bank approval time and volume fees can move the total more than the software quote.

Launch fewer rails first

Delay card issuing if possible

Watch transaction volume closely

MVP rail choice

The real budget question is simple: which banking rails must work at launch? If the MVP only needs account opening, core ledger, and ACH, the integration cost stays leaner than a full stack with debit cards, identity, fraud, and reporting. Each added rail usually brings more fees, more testing, and more compliance review.

Digital Banking Cybersecurity Startup Expense

Cybersecurity First

For a digital bank, cybersecurity is launch-critical. Budget secure cloud architecture, encryption, identity and access controls, monitoring, backup procedures, incident response, and compliance readiness from day one. The base spend here is $15,000 a month for cloud hosting plus $5,000 a month for security software, or $240,000 a year before testing and outside reviews.

Cost Inputs

Estimate this cost from months covered, vendor quotes, and staff time. Include the Head of Technology and engineering team, but don’t double count software build work if it is capitalized. Add quote-backed lines later for penetration tests, security audits, managed detection, cyber insurance, and external readiness reviews.

12 months of hosting

Separate capitalized build work

Add third-party quotes

Keep It Tight

Keep spend lean by bundling security tools, locking scope early, and separating one-time launch work from recurring operations. The clean rule is simple: if a control protects customer data or supports compliance, don’t trim it; if two line items cover the same work, cut the duplicate.

Launch Readiness

This line item is not just IT overhead. It protects onboarding, payments, and deposit flows, and it also supports audit and regulator questions. If controls are not ready before launch, the delay cost usually shows up in lost launch time, not just a bigger budget.

Digital Banking Platform Launch Startup Expense

Pre-open team

This startup expense covers the work needed before the first customer signs up: product, engineering, compliance, operations, support, and marketing. Year 1 payroll is $775,000 across six roles, including $85,000 for the Marketing Manager and $90,000 for the Head of Customer Support. Keep it separate from run-rate payroll after launch.

How to size it

Estimate this cost from named salaries plus launch months of coverage. Use the known $775,000 Year 1 payroll, then add launch-only spend tied to onboarding, disclosure prep, release testing, and support setup. Do not fold in long-term operating payroll or transaction fees, or the launch budget will look cleaner than the cash need.

Use named salary inputs first

Add launch-only setup work

Keep ongoing costs separate

Launch cost pressure

After growth starts, economics change fast. Plan for 15% customer acquisition costs and 3% interchange fees on card spend. The fix is simple: slow paid acquisition until early retention is clear, and keep channel spend separate from transaction-volume costs so you can see true payback.

Readiness gates

Do not open the gates until support scripts, fraud queues, consumer disclosures, and release testing pass review. That is the line between a controlled launch and a messy one. If any gate slips, the cost shows up in support load, chargeback risk, and delayed revenue.

Compare 3 Startup Cost Scenarios

Scenario table

Lean, base, and full launches change cost fast because product scope, compliance, security, support, and integrations scale differently. The base case follows the model's Year 1 deposit and loan starting point.

Lean, base, and full launch cost comparison for a digital banking platform.

Scenario

Lean LaunchMVP validation

Base LaunchCompliant first launch

Full LaunchMulti-product scale

Launch model

Starts with an MVP that validates core banking flows before adding lending or investments.

Matches the model's first-year deposit and loan base for a compliant first launch.

Builds a broader platform with more products, stronger compliance, and larger support capacity.

Typical setup

Launch one region with core account tools, payments, and a narrow product set.

Launch the modeled deposit and loan base with compliant banking, payments, and standard support.

Launch across more account types with card issuing, lending, fraud controls, and deeper security.

Cost drivers

One market

fewer account types

fewer integrations

deferred lending

lighter compliance

Checking and savings

$30M deposits

$11M loans

standard compliance

core support

More account types

card issuing

lending and mortgages

fraud tooling

deeper security

Planning rangeCAPEX only

Quote-backed lower bandLower cost

$1.5M base runwayModel anchor

Quote-backed upper bandHigher scope

Best fit

Best for founders testing demand before a wider rollout.

Best for teams that want a solid first launch with the model's Year 1 funding base.

Best for teams planning a wider product set and heavier control needs from day one.

!

Planning note: Scenario ranges are researched planning assumptions, not exact vendor quotes.

The provided model does not include a quote-backed MVP build cost, so do not treat the $151 million as a full MVP price It is the known first-year operating runway before CAPEX, variable costs, and capital needs The model includes $61,300 in monthly fixed costs, $775,000 in first-year payroll, and 18% variable expenses tied to customer acquisition and interchange fees paid

Plan runway beyond the build period because compliance, testing, vendor setup, and user acquisition rarely move in a straight line The model shows $61,300 of fixed costs every month and $775,000 of first-year payroll That means the first operating year needs about $151 million before CAPEX, variable expenses, regulatory capital, customer funds, and any quote-backed implementation fees

Not always, but the model does not prove which path is right A partner-bank model can avoid some charter steps, but it still needs compliance, legal, security, and integration spend The model includes $8,000 per month in regulatory compliance fees, $6,000 per month for legal counsel, and a $120,000 Compliance Officer before any charter-related capital or approval costs

Budget cybersecurity as a launch requirement, not as a later upgrade The model includes $15,000 per month for cloud hosting and $5,000 per month for data security software, or $240,000 per year combined You should still price penetration testing, monitoring, incident response planning, vulnerability management, and security readiness reviews separately because those one-time costs are not quoted in the data

Customer deposits are funding or balance sheet liabilities, not normal startup expenses The Year 1 model assumes $10 million in checking deposits, $15 million in savings deposits, and $5 million in money market accounts Those balances support the banking model, while startup costs cover payroll, compliance, cloud, licenses, security, legal, integrations, and launch readiness

About the author

Ethan Carter

Founder-Focused Content Writer

Ethan Carter is a founder-focused content writer at Financial Models Lab, specializing in business expense analysis and what it really costs to operate a startup. He writes practical founder checklists for people starting with limited capital, helping them plan realistically before money is invested and connect business ideas with workable startup budgets.

Choosing a selection results in a full page refresh.