Fintech Startup Costs: Plan Build, Compliance, And $62K Monthly Fixed Burn

A fintech startup cost estimate should start with the product build, then add the launch overhead that simple app quotes miss In the researched model, a regulated base launch carries $62,000 per month in fixed costs, or $744,000 in the first year, before payroll, variable processing, working capital, and credit funding Known first-year staffing assumptions include a $200,000 CEO, $180,000 CTO, and 05 FTE Head of Product at $80,000, so total funding need can exceed the fintech minimum viable product (MVP) cost quickly A fuller lending platform also has to support $115 million of Year 1 loans, $20 million of other interest-earning assets, and compliance, security, licensing, customer acquisition, and runway costs

Calculate Fuding Needs

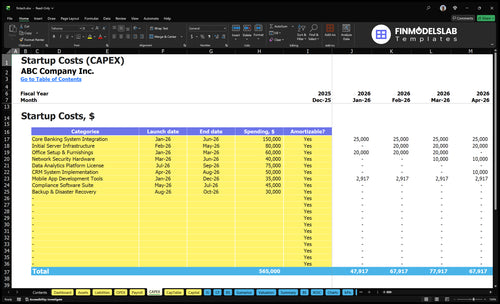

Startup cost summary

This table shows the main startup CAPEX and excluded cash needs for a fintech startup, using model-backed planning assumptions.

Minimum cash need driven by Year 1 losses, payroll, and balance sheet funding

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates only the capitalized startup assets needed to launch the fintech platform, not operating cash or runway.

!

Exclusions This calculator covers capitalized startup assets only. It excludes the model's $62,000 monthly fixed costs, including $15,000 cloud hosting, $10,000 compliance, and $8,000 legal, plus payroll runway, deposits, debt service, inventory, working capital, marketing subscriptions, and other operating expenses.

Costs rise fast as the launch moves from a narrow MVP to a regulated lending platform and then to a larger balance sheet. Compliance, security, integrations, and team size drive the step-up.

Lean, Base, and Full launch cost comparison

Scenario

Lean LaunchNarrow scope

Base LaunchRegulated launch

Full LaunchScaled platform

Launch model

Start with a narrow feature set, limited regulated activity, and fewer data integrations so you can launch faster.

Run a regulated launch with the modeled $62,000 monthly fixed cost and $744,000 first-year fixed overhead.

Run a broader platform with Year 1 scale at $115 million loans, $20 million other interest-earning assets, $25 million customer deposits, and $33 million total liabilities.

Typical setup

Use a small team, basic cloud tools, and core security controls for one simple product path.

Carry the core compliance, legal, security, cloud, and sponsor bank stack needed for a live launch.

Add broader integrations, deeper security, and a larger compliance, credit, and support team.

Cost drivers

Limited compliance

Fewer integrations

Small team

Basic cloud

Compliance/legal

Cloud hosting

Security software

Sponsor bank fees

Core team

Large loan book

Deposit growth

Securities portfolio

Higher compliance

Larger team

Planning rangeCAPEX only

Lower six figuresLight build

$744,000 first yearModel-backed

Nine-figure balance sheetHigh complexity

Best fit

Best for teams testing product demand before they add heavier regulated workflows.

Best for founders launching a real operating model with steady controls and vendor coverage.

Best for teams ready to fund a larger regulated platform and carry more operating load.

!

Planning note: These scenario ranges are researched planning assumptions, not exact vendor quotes or binding pricing.

How to plan funding for a fintech startup?

Plan funding for Fintech Startup by splitting the need into CAPEX, pre-opening expenses, monthly burn, and working capital. Here’s the quick math: the fixed burn is $62,000 a month, or $744,000 a year before payroll, then add $200,000 for the CEO, $180,000 for the CTO, and 0.5 FTE Head of Product at $80,000 in Year 1, while keeping $115 million of Year 1 loans and $20 million of other interest-earning assets separate from operating cash.

Funding buckets

Split CAPEX from cash burn.

List pre-opening costs first.

Track working capital needs.

Keep credit funding separate.

Ask drivers

Set ask by runway period.

Map it to launch month.

Link it to compliance and integration.

Check bank terms and vendor quotes.

What drives the cost of a fintech startup?

Fintech Startup costs are driven most by regulated product design, secure engineering, bank or payment integrations, compliance review, and specialized talent. Here’s the quick math: a Year 1 fixed stack can run about $45,000 per month before growth costs, using $10,000 compliance, $8,000 legal, $15,000 cloud hosting, $5,000 security software, and $7,000 sponsor bank fees. Then add variable drag like 25% transaction processing fees and up to 30% cloud scaling in Year 1, plus extra review and testing for lending, deposits, payments, identity checks, fraud controls, and data feeds.

Fixed cost drivers

$10,000 monthly compliance

$8,000 legal retainer

$15,000 cloud hosting

$7,000 sponsor bank fees

Variable cost drivers

25% transaction processing fees

30% cloud scaling in Year 1

$5,000 security software

Extra testing for fraud and identity

What are the hidden costs of starting a fintech company?

The hidden costs of starting a Fintech Startup are usually bigger than the app build: one model shows $62,000 a month in fixed commitments before full payroll, with $10,000 for compliance, $8,000 for legal, $5,000 for data security, and $15,000 for cloud hosting. For a related read on cash pressure, see How Much Does The Owner Of Fintech Startup Make? — because working capital also gets tied up by $115 million in Year 1 loan volume and $33 million in Year 1 liabilities. What this estimate hides is customer acquisition scale-up, post-launch losses, transaction fees, and usage-based cloud costs that may never show up in CAPEX.

Core fixed costs

$10,000 compliance monitoring

$8,000 legal review

$5,000 security testing

$15,000 cloud hosting

Scale-up cash drains

Customer support needs cash

Failed integrations waste runway

$115 million Year 1 loan volume

$33 million Year 1 liabilities

Key Takeaways

Software build is capitalized; hosting and support are not.

Legal and compliance run about $216,000 in Year 1.

Cloud and security add $240,000 before scaling costs.

Integration fees and staffing drive launch timing and spend.

Fintech Startup Core Five Startup Costs

Fintech App And Platform Development Startup Expense

Build scope

A fintech app build should cover product design, backend architecture, mobile or web apps, admin dashboard, onboarding, account flows, transaction logic, credit workflows, and pre-launch QA. The build is capitalized software; maintenance, hosting, support, and future releases stay outside startup build cost.

Pricing inputs

Use four fields: capitalized build, implementation, devices, and contingency. Size the scope to Year 1 products: $5 million personal loans, $3 million small business loans, $2 million secured credit lines, $1 million auto refinance, and $500,000 student loan refinance.

Count onboarding and account flows

Add testing and launch fixes

Match tools to product scope

Keep it separate

Don’t bury recurring items in the build. Cloud hosting, support, bug fixes, and new feature releases sit in operating expense, while build work ends at launch-ready code. Ask for a scope split before you price vendors, so one-time engineering and hardware stay separate from monthly run costs.

Split launch work from recurring work

Exclude roadmap features

Keep vendor quotes itemized

Year 1 fit

Here’s the quick math: Year 1 lending scope totals $11.5 million, but this model is an operating and balance sheet plan, not a vendor app-build quote. Use it to size software, implementation, devices, and contingency, then price each module by flow and test step.

Fintech Team And Launch Readiness Startup Expense

Launch team scope

This cost covers pre-opening staffing and launch setup: founders’ technical support, outsourced development, fractional compliance, product management, finance/accounting, customer support setup, launch marketing, sales readiness, and vendor onboarding. Use the model’s salary anchors: $200,000 CEO, $180,000 CTO, $160,000 Head of Product at the listed 05 FTE input, and $150,000 Lead Engineer.

What to budget

The launch stack also includes $3,000 a month for marketing software and $2,000 a month for admin software, or $5,000 monthly total. That is $60,000 a year if you carry it for 12 months. Build the estimate from salary months, FTE mix, implementation quotes, and onboarding fees.

Count months of coverage

Separate setup from runway

Price vendor onboarding quotes

How to keep it tight

Ask one clean question first: is the team building in-house, hiring contractors, or buying implementation support? That choice drives cash need fast. Use contractors for time-boxed launch tasks, but keep compliance and finance ownership clear. One rule: don’t mix launch setup with post-launch payroll runway or ongoing customer acquisition spend.

Runway split

Keep the budget in two buckets: pre-opening build and launch prep, then post-launch payroll runway. If the software stack runs for 3 months before launch, that is $15,000 just for admin and marketing tools. What this estimate hides: benefits, payroll taxes, and any contractor or compliance quotes.

Fintech Legal And Compliance Startup Expense

Compliance Base

A fintech launch needs counsel, regulatory review, and partner checks before the first account opens. Using the model, regulatory compliance at $10,000 a month plus legal counsel at $8,000 a month totals $216,000 in year one. That bucket is planning spend, not legal advice.

Scope Inputs

This line item covers counsel, KYC, AML, privacy policies, vendor contracts, compliance docs, lending review, deposit or bank partner review, and launch approvals. Estimate it with months of coverage, state count, product mix, loan volume, deposit volume, and sponsor bank credit. With year-one assumptions of $115 million loans, $25 million deposits, $5 million institutional funding, and $3 million sponsor bank credit, scope stays large.

Cost Control

Keep the work scoped by product and state. A checking-only launch in a few states costs less than a lending and deposit model with wider exposure. Reuse documented policies, push vendor paper early, and set one approval owner. The usual mistake is underfunding state-by-state review, then paying for rework when the bank partner asks for more controls.

Budget Drivers

The real cost driver is not headcount alone; it's product breadth, state exposure, and partner structure. More lending volume, more customer deposits, and a sponsor bank credit note raise review time and documentation load. For planning, keep this as a separate compliance reserve so legal and launch approvals don't compete with build or funding needs.

Fintech Banking And API Integration Startup Expense

App Build

The build should cover product design, backend architecture, onboarding, account flows, transaction logic, credit workflows, and QA. Price it as capitalized software plus implementation, devices, and contingency. The model also ties scope to Year 1 products: $5 million personal loans, $3 million small business loans, $2 million secured credit lines, $1 million auto refi, and $500,000 student refi.

Legal Spend

Plan for counsel, regulatory review, KYC, AML, privacy policies, vendor contracts, and launch approvals. The model uses $10,000 monthly compliance plus $8,000 legal retainer, or $216,000 in Year 1. Tie effort to $115 million loans, $25 million deposits, $5 million institutional funding, and $3 million sponsor bank credit.

Cloud Security

Separate one-time launch work from recurring cloud and monitoring. The model uses $15,000 monthly cloud hosting and $5,000 monthly security software, or $240,000 in Year 1. Variable cloud scaling adds 30% in Year 1 and 28% in Year 2, so more accounts, fraud checks, and data retention push cost up.

Bank Rails

Cover sponsor bank setup, processor implementation, automated clearing house (ACH), card rails, payment gateways, identity verification, fraud tools, credit data, market data, and financial data aggregation. Price setup, testing, minimum fees, transaction fees, and usage. Use $7,000 monthly sponsor bank fee, $3 million sponsor bank credit in Year 1, and processing fees at 25%, 22%, and 20% across Years 1 to 3.

Launch Team

Budget founders’ technical help, outsourced development, fractional compliance, product management, finance/accounting, customer support setup, launch marketing, sales readiness, and vendor onboarding separately from post-launch payroll runway. The model lists $200,000 CEO, $180,000 CTO, $160,000 Head of Product with 05 FTE in Year 1, plus a $150,000 Lead Engineer and $3,000 monthly marketing platform and $2,000 admin software.

Use contractors for speed.

Keep compliance coverage fractional.

Buy support before hiring full-time.

Fintech Cybersecurity And Cloud Infrastructure Startup Expense

Cloud Setup

Launch costs cover secure hosting, encryption, monitoring, penetration testing, vulnerability scans, access controls, logging, backups, and security policies. Keep the one-time setup separate from monthly cloud and monitoring spend. For planning, the recurring base starts at $15,000 for cloud hosting plus $5,000 for data security software.

Cost Drivers

The first-year recurring total is $240,000 or $20,000 per month. Here’s the quick math: $15,000 cloud hosting + $5,000 security software = $20,000 monthly. Add 30% variable cloud scaling in Year 1 and 28% in Year 2 as transactions, accounts, fraud checks, audit readiness, and data retention grow.

Manage It

Use separate budget lines for launch setup, then recurring cloud and monitoring. Don’t treat monthly cloud usage as CAPEX unless accounting supports it. The cleanest control is to get monthly vendor quotes, set usage alerts, and review log retention and scan frequency before you scale traffic or open more accounts.

Budget Check

Plan the launch with a hard split: one-time setup on day one, then a recurring run rate of $20,000 per month before scaling. If transaction volume rises faster than expected, the cloud bill moves with it, so keep a reserve for higher fraud monitoring, backups, and audit demands.