Hospital Indemnity Insurance Agency Startup Costs: $400K CAPEX Plan

For this researched planning case, the cost to start a hospital indemnity insurance agency includes $400,000 of startup CAPEX plus enough funding to cover an $855,000 Year 1 EBITDA loss The first-year budget also includes $450,000 in marketing at a modeled $125 customer acquisition cost, $905,000 in wages, and $236,400 in annual fixed overhead The model reaches breakeven in Month 21, hits minimum cash of -$813,000 in Month 29, and shows payback in Month 55 Treat these as researched startup-planning assumptions, not vendor quotes, guarantees, or legal advice

Hospital Indemnity Insurance Agency CAPEX Calculator Objective

Startup CAPEX Calculator

Estimates capitalized startup assets only for launch; base case totals $400,000 before contingency.

CAPEX only Use this for capitalized startup assets only. It excludes inventory, payroll runway, deposits, debt service, working capital, marketing, subscriptions, and software-as-a-service fees.

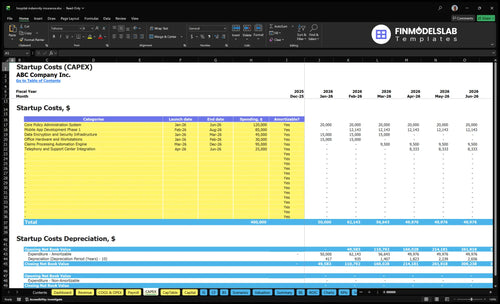

What does this CAPEX screenshot show?

This screenshot shows the CAPEX tab in the Hospital Indemnity Insurance Agency Financial Model Template: startup costs, launch timing, and depreciation/amortization. Open it to validate assumptions.

Key screenshot highlights

- CAPEX: $400,000

- Month 1-60 forecast

- Breakeven in Month 21

- Cash trough Month 29

- Payback by Month 55

What are the biggest startup costs for a hospital indemnity insurance agency?

The biggest startup costs for a Hospital Indemnity Insurance Agency are staffing and customer acquisition, not office furniture. Modeled launch costs include $905,000 in Year 1 wages, $450,000 in Year 1 marketing, and $400,000 in CAPEX, plus $19,700 a month in fixed overhead. Here’s the quick math: that monthly overhead includes $4,500 cloud infrastructure, $6,200 rent and utilities, $2,500 compliance and filing fees, $1,800 professional liability insurance, $1,200 customer support software, and $3,500 legal and audit retainers.

Main launch costs

- $905,000 Year 1 wages

- $450,000 Year 1 marketing

- $400,000 CAPEX

- Producer readiness drives spend

Monthly fixed overhead

- $4,500 cloud infrastructure

- $6,200 rent and utilities

- $2,500 compliance and filing fees

- $1,800 liability insurance

What hidden costs come with starting a hospital indemnity insurance agency?

Starting a Hospital Indemnity Insurance Agency brings hidden monthly costs fast: the core stack already adds up to $9,000 a month from $1,800 professional liability insurance, $2,500 compliance and filing fees, $3,500 legal and audit retainers, and $1,200 customer support software. For the revenue side, see How Much Does A Hospital Indemnity Insurance Agency Owner Make?; the agency sells policies and services applicants, but it does not fund hospital indemnity claim benefits. A useful operating assumption is 60% of revenue for payment processing and claims verification.

Fixed monthly costs

- E&O coverage runs $1,800/month.

- Compliance and filing fees run $2,500/month.

- Legal and audit retainers run $3,500/month.

- Support software runs $1,200/month.

Launch and cash traps

- Background checks add upfront delay.

- Appointment paperwork and continuing education recur.

- Software onboarding and compliance documentation take time.

- Commission lag, failed lead tests, and renewals hit cash flow.

How do I fund a hospital indemnity insurance agency startup?

Fund the Hospital Indemnity Insurance Agency for cash timing, not just launch costs: Year 1 needs $450,000 in marketing, $905,000 in wages, and $236,400 in fixed overhead, with Year 1 EBITDA of -$855,000. The plan should expect Month 21 breakeven, a cash low of -$813,000 in Month 29, and payback around Month 55. Build in extra cushion for owner draw, compliance work, and CAC above $125, since commissions can trail the written policy by weeks.

Funding needs

- $450,000 marketing budget

- $905,000 wages budget

- $236,400 overhead budget

- Month 21 breakeven target

Cash risks

- -$813,000 cash trough

- Month 29 minimum cash

- Month 55 payback timing

- Commission lag cuts cash

Hospital Indemnity Insurance Agency Startup Cost Breakdown Table Objective

Startup cost summary

This table shows the main startup assets and the non-CAPEX cash reserve needed before breakeven.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Core Policy Administration System | $120,000 | Policy setup, workflow rules, and carrier integrations | Yes |

| Mobile App Development Phase 1 | $85,000 | Customer self-service design, build, and testing | Yes |

| Claims Processing Automation Engine | $95,000 | Automation rules for claims intake, review, and payout checks | Yes |

| Data Encryption and Security Infrastructure | $45,000 | Security controls, encryption, and protected data hosting | Yes |

| Office Hardware and Workstations | $30,000 | Workstations, devices, and launch office setup | Yes |

| Operating Reserve | $813,000 | Pre-breakeven losses, monthly overhead, and launch runway | No |

Hospital Indemnity Insurance Agency Core Five Startup Costs

Licensing, Compliance, and Appointment Startup Expense

License setup

Use $2,500 per month as the anchor for compliance and filing fees, but keep one-time setup separate: resident producer license, any nonresident licenses, agency entity license, carrier appointments, background checks, and compliance docs. Cost moves with state, producer count, and one-state vs multi-state selling.

Monthly support

Monthly support covers filing calendars, appointment tracking, continuing education, and document control so producers stay authorized before selling supplemental health policies. Here’s the quick math: $2,500 per month is the planning anchor, but the real bill shifts with the license mix and how many producers need active status.

- Track renewal dates by state

- Store appointment proof

- Keep CE records current

Renewals

Renewals are not the same as setup. Budget for license renewals, appointment updates, background check refreshes, and continuing education so each producer stays cleared to sell. The lowest-friction path is one state first; multi-state sales add filings, dates, and admin load fast.

Cost drivers

Costs rise when the agency adds producers, adds states, or expands carrier lines. Keep the budget split into one-time setup, monthly compliance support, renewals, and pre-sale authorization steps. That keeps the $2,500 monthly anchor useful without hiding the extra work behind each new license.

Insurance, Legal, Accounting, and Risk-Control Startup Expense

Credibility First

Before the agency sells or services policies, budget for errors and omissions insurance, which covers professional mistakes in sales or servicing. Use $1,800 per month for professional liability insurance and $3,500 per month for legal and audit retainers. This is operating protection, not CAPEX.

Compliance Setup

Plan for business registration, legal review, accounting setup, compliance consulting, privacy policy review, client disclosure review, and records retention rules. Split one-time setup from monthly support so you can see what starts the agency and what keeps it compliant. One clean rule: if it touches data or commissions, it needs a paper trail.

Keep It Separate

Do not mix these professional fees and risk coverage with CAPEX or recurring software subscriptions. CAPEX is for systems and equipment; these costs protect the agency’s license, disclosures, and audit trail. If you blur them, startup burn looks smaller than it is and cash planning gets sloppy.

Trust Before Volume

These costs buy trust before the agency handles applications, sensitive health data, and commission records. That matters because one bad file or missed disclosure can damage credibility fast. Keep the legal and insurance budget in place from day one, then renew it on schedule.

CRM, Policy Technology, and Secure Systems Startup Expense

Core platform

Hospital indemnity needs a working policy stack from day one. The base build is $370,000 in CAPEX: $120,000 policy admin, $85,000 mobile app phase 1, $45,000 security, $95,000 claims automation, and $25,000 telephony integration. That covers policy administration, quoting, enrollment, support, secure file storage, e-signature, website setup, and commission tracking.

Setup mix

Price it as one-time implementation plus recurring software. The monthly run rate is $5,700: $4,500 cloud and security hosting and $1,200 customer support software. To estimate cleanly, separate vendor build fees, subscription fees, user counts, and integration scope. That keeps CAPEX distinct from operating spend.

Control spend

The cheapest safe path is to launch the core policy admin, quoting, enrollment, and claims flow first, then add app features after the first workflow is stable. Don't fold implementation fees into subscriptions. The usual mistake is paying for extra customization before the support team, file rules, and commission tracking are already working.

Monthly burn

On day one, this stack already carries a fixed tech load of $5,700 a month before marketing or payroll. If claims, support, or secure storage volumes rise, cloud and support seats should be the first line items you recheck. Keep the budget tied to live policy count, not wishful growth.

Lead Generation and Launch Marketing Startup Expense

Launch demand

Customer acquisition is the big swing factor here. Model Year 1 marketing at $450,000, and at a $125 CAC that implies about 3,600 customers if the assumption holds. That spend should cover paid leads, local marketing, SEO setup, landing pages, call tracking, referral partnerships, and compliance-approved ads.

What it covers

Estimate this cost as channel spend plus setup work, or as target customers times CAC. For this agency, the inputs are $450,000 of Year 1 spend, a $125 CAC, and the channels listed above. One clean check: if CAC drifts up, the same budget buys fewer customers and slows policy growth.

- Paid leads and referral fees

- SEO and landing page setup

- Call tracking and ad compliance

Keep CAC tight

Use one message per channel, then watch cost per acquired customer by source. Don’t promise lead quality or conversion rates. Keep compliance-approved ads, use call tracking, and test referral partners in small batches. The goal is simple: protect the $125 CAC so the $450,000 plan does not get swallowed by waste.

- Track CAC by source

- Cut weak channels fast

- Keep compliance review first

Price mix

The revenue model has to work against low monthly premiums. With Bronze at $35, Silver at $55, and Gold at $85 per month, each acquisition has to earn back the $125 CAC over time. That makes plan mix and retention part of the marketing budget math, not separate issues.

Staffing, Producer Onboarding, and Office Readiness Startup Expense

Staffing Cost Base

Year 1 staffing is modeled at $905,000 in wages, before contractor commissions, training, and working capital. That covers one CEO at $185,000, one Chief Actuary at $165,000, two Claims Adjusters at $75,000 each, three Customer Success Representatives at $55,000 each, one Lead Software Engineer at $145,000, and one Marketing Manager at $95,000.

Setup Inputs

This cost also includes licensed producer onboarding, training materials, customer support readiness, follow-up steps, records handling, laptops, phones, and remote work setup. Here’s the quick math: count headcount, price each salary, add onboarding tools, and layer in office hardware. Physical office CAPEX is modeled at $30,000, with rent and utilities at $6,200 per month.

- Separate wages from commissions

- Track one-time and monthly costs

- Budget before policy sales start

Cost Control

Keep thi s line tight by staging hires, using standard onboarding packs, and buying laptops and phones in batches. Don’t bury office costs inside payroll, and don’t mix contractor commissions with wages. What this estimate hides is timing: if onboarding takes longer than planned, you still carry the $6,200 monthly rent and utilities.

- Hire to workload, not hope

- Reuse training for each producer

- Review remote tools before scaling

Office Readiness

Office readiness is the bridge between licensing and first sales. Budget for workstations, secure files, support scripts, and claims follow-up tools before launch, because this team handles sensitive health data and commission records. One clean rule: buy once, document everything, and keep access controls simple from day one.

Lean, Base, and Full Hospital Indemnity Agency Startup Cost Scenario Table Objective

Scenario Table

Scenario scale changes fast in this agency because state licensing, producer count, compliance, and support all lift startup cash. Lean cuts scope; Base matches the model; Full adds scale and overhead.

| Scenario | Lean LaunchHome-Based | Base LaunchBase Case | Full LaunchMulti-Producer |

|---|---|---|---|

| Launch model | Launch in fewer states with a small producer bench, remote-first service, and only the core policy and claims tools. | Use the model setup: multi-state launch with the modeled producer footprint, in-office support, and the full core tech stack. | Expand to more states with more producers, heavier paid acquisition, and extra compliance and support capacity. |

| Typical setup | Keep office needs light and trim compliance, support, and system scope to the minimum needed. | Run from the modeled office setup with full compliance, security, support software, and the planned core systems. | Add more claims staff, more customer support, broader compliance coverage, and larger infrastructure. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | Below base caseLower funding | Model caseModel funding | Above base caseHigher funding |

| Best fit | Best for founders testing demand before a broader licensed rollout. | Best for a founder who wants to follow the model closely and track toward Month 21 breakeven. | Best for teams pushing growth faster and willing to carry more overhead and cash burn. |

Planning note: These scenario ranges are researched planning assumptions, not exact vendor quotes.

Related Products

- Hospital Indemnity Insurance Agency Porter's Five Forces Analysis

- Hospital Indemnity Insurance Agency BCG Matrix

- Hospital Indemnity Insurance Agency Business Model Canvas

- What Are The 5 Core KPIs For Hospital Indemnity Insurance Agency Business?

- Hospital Indemnity Insurance Agency Business Plan Template in Pre-Written Word

- How Increase Hospital Indemnity Insurance Agency Profitability?

- What Are Operating Costs For Hospital Indemnity Insurance Agency?

- Hospital Indemnity Insurance Agency Financial Model Template in Excel

- How Much Hospital Indemnity Agency Owners Make: $185K-$227M

- Open A Hospital Indemnity Insurance Agency In 45 To 90 Days

- How To Write A Business Plan For Hospital Indemnity Insurance Agency?

- Hospital Indemnity Insurance Agency Marketing Mix

- Hospital Indemnity Insurance Agency Marketing Plan

- Hospital Indemnity Insurance Agency Business Proposal

- Hospital Indemnity Insurance Agency PESTEL Analysis

- Hospital Indemnity Insurance Agency Pitch Deck Example Editable PPTX

- Hospital Indemnity Insurance Agency Business SWOT Analysis

- Hospital Indemnity Insurance Agency Value Proposition Canvas

Frequently Asked Questions

The model shows breakeven in Month 21, so the agency needs runway beyond opening costs Base startup CAPEX is $400,000, Year 1 EBITDA is -$855,000, and minimum cash reaches -$813,000 in Month 29 That means funding should cover setup, early losses, and a cushion for slower commission timing