You’re planning cash before policies turn into commissions, so the insurance agency startup budget should separate equipment, pre-opening costs, and working capital In the researched model, fixed overhead runs $5,000 per month without office rent or $8,650 per month with a small office, plus $350,000 in first-year marketing These insurance agency opening expenses are planning assumptions for the first operating year, not vendor quotes or guaranteed totals

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for an insurance agency launch.

!

What's excluded This calculator covers only capitalized startup assets. It excludes licensing fees, marketing spend, payroll runway, rent deposits, insurance premiums, software subscriptions, debt service, working capital, inventory, and ongoing operating costs. Office rent, utilities, and office supplies from the fixed-cost context stay outside CAPEX: rent is $3,000 per month, utilities are $400 per month, and office supplies are $250 per month.

What should the Insurance Agency startup cost screenshot show?

How much money do I need to start an insurance agency?

You don’t need one fixed amount to start an Insurance Agency; you need enough for CAPEX, or one-time setup costs, plus pre-opening expenses and working capital, based on What Is The Main Goal You Want To Achieve With Your Insurance Agency?. A home-based launch carries lower CAPEX and about $5,000/month in non-office fixed overhead, while a small office moves fixed overhead to $8,650/month.

Lean Launch

Start home-based to lower CAPEX

Plan $5,000/month non-office overhead

Cover software, legal, insurance, marketing

Fund working capital before sales ramp

Bigger Launch

Add $3,000 rent

Add $400 utilities

Add $250 office supplies

Model $340,000 payroll and $350,000 marketing

What hidden costs should I expect when opening an insurance agency?

If you're opening an insurance agency, the hidden cost is usually not equipment; it’s the cash gap before commissions arrive. Read the earnings side in How Much Does The Owner Of An Insurance Agency Typically Make?, but budget separately for working capital, CAPEX (equipment and setup), and pre-opening costs like licensing, background checks, E&O, and website launch. In Year 1, plan for $500 a month for business insurance, $2,000 for legal and accounting, $1,000 for marketing subscriptions, and compliance fees at 10% of revenue, even if you expect 90% of Year 1 commissions.

Before you open

State licensing can delay launch.

Background checks cost time and cash.

E&O premiums hit before revenue.

Rent deposits and setup fees come first.

After launch

$500 monthly business insurance.

$2,000 legal and accounting each month.

$1,000 marketing software subscriptions.

Payroll can start before commissions do.

Compliance costs

Compliance fees modeled at 10% of revenue.

Renewals add ongoing admin work.

Software onboarding takes cash upfront.

Commission revenue may lag spending.

Cash planning

Separate working capital from CAPEX.

Track pre-opening expenses separately.

Budget for website launch and marketing ramp-up.

Expect costs before first policy closes.

What are the biggest costs to start an insurance agency?

The biggest startup costs for an Insurance Agency are $350,000 in Year 1 marketing, $340,000 in Year 1 payroll, and $8,650 per month in fixed overhead. Tech adds about $1,500 per month for software, and office choice can swing the budget by $3,650 per month once rent, utilities, and supplies are included. Here’s the quick math: paid acquisition assumes $500 producer CAC and $20 customer CAC, so launch spend is mostly about distribution, staffing, and access.

Big cash drivers

$350,000 Year 1 marketing

$340,000 Year 1 payroll

$8,650 monthly overhead

Carrier access and appointments

Tech and space costs

$1,500 monthly software

Agency system, CRM, rater

Secure email, phone, website

$3,650 office budget swing

Calculate Fuding Needs

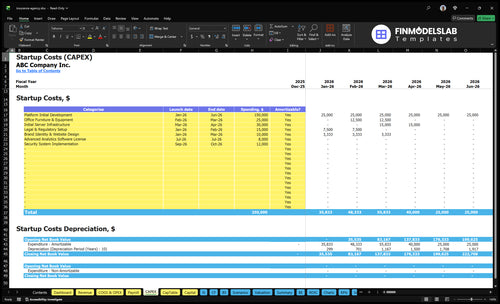

Startup Cost Summary Table

This table breaks out insurance agency startup CAPEX and the excluded opening cash buffer needed for payroll, marketing, and overhead.

Highlighted CAPEX$230,000Base planning example

Excluded cash needs$881,000Outside CAPEX total

Funding need$1,111,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Platform Initial Development

$150,000

Build scope and months of development

Yes

Office Furniture and Equipment

$25,000

Home office vs leased space setup

Yes

Initial Server Infrastructure

$30,000

Server capacity and security spec

Yes

Legal and Regulatory Setup

$15,000

State filing and compliance complexity

Yes

Brand Identity and Website Design

$10,000

Brand scope and launch design depth

Yes

Working Capital Reserve

$881,000

Payroll, marketing, and fixed overhead runway

No

Insurance Agency Core Five Startup Costs

Licensing And Compliance Startup Expense

License Budget

Licensing and compliance is a real launch cost, not paperwork noise. Budget state fees, pre-licensing education, producer exams, background checks, entity registration, agency license filings, appointment paperwork, compliance setup, and continuing education. The model carries regulatory compliance at 10% of revenue in Year 1, easing to 8% by Year 5.

What It Covers

This cost changes by state, line of business, and headcount. Build it from the number of states, exam fees, background checks, filing fees, and renewal cycles. Keep state licensing separate from carrier production rules and aggregator rules. Ask which lines will be sold: life and health, property and casualty, and specialty.

Count states first.

Price each exam separately.

Plan renewals early.

Keep It Lean

File only the licenses you need now, then batch education and exams by state. Put continuing education on a calendar before renewal dates hit. Do not bundle carrier onboarding into the state budget. One clean rule: if it does not change your right to sell, keep it out of licensing cost.

Batch filings by state.

Separate carrier paperwork.

Track CE deadlines.

Line Mix Risk

The hidden risk is speed. If you want to sell across life and health, property and casualty, and specialty at once, approvals can stack up and delay first revenue. Build the compliance plan before launch, then match appointments and paperwork to the first product line you can legally sell.

E&O And Business Insurance Startup Expense

Pre-Opening Coverage

Before you bind or advise on policies, E&O and business insurance belong in startup spend, not CAPEX. The source model starts at $500 per month from Month 1, and payroll roles in Month 1 can also trigger workers’ compensation, depending on state and hiring structure.

What It Covers

Budget this line for professional liability, general liability, cyber liability, workers’ compensation if hiring, and any bond or compliance coverage. Here’s the quick math: coverage cost is driven by policy type, state rules, headcount, and when payroll starts. Separate these premiums from office equipment and leasehold improvements.

Price each policy by type.

Check state hiring rules.

Track Month 1 payroll.

Trim The Premium

Keep insurance quotes separate from buildout costs, and don’t hide premiums inside office furniture or rent deposits. Ask for quotes only on required coverages first, then add cyber or bond coverage if the license, carrier, or compliance setup needs it. One clean one-liner: insurance costs are recurring operating costs, not one-time assets.

Separate required from optional cover.

Delay hiring until needed.

Don’t mix with CAPEX.

Keep It Out Of CAPEX

Put premiums in pre-opening expense or monthly operating cost. That keeps the launch budget clean and avoids inflating fixed assets with coverage you need before day one.

Agency Technology Stack Startup Expense

Stack spend

Agency tech spend starts with the agency management system, customer relationship management (CRM), comparative rater, e-signature, secure email, phone or VoIP (internet calling), website, hosting, and data security. Budget recurring licenses separately from one-time onboarding, migration, and implementation. Source lines include $1,500 monthly general software licenses, $1,000 monthly marketing platform subscriptions, 20% Year 1 hosting and infrastructure, and 15% Year 1 payment gateway fees.

Build it

Use vendor quotes, user counts, and months of coverage to price the stack. Here’s the quick math: seats × license price, plus setup quotes for migration and onboarding, plus transaction volume tied to gateway fees. One line: recurring software burn is not the same as launch cash.

Price users, not feature lists.

Separate setup from subscriptions.

Track gateway fees by volume.

Keep it lean

Ask vendors to split implementation from subscriptions so you can see opening cash needs clearly. Don’t bury website work, data security setup, or migration inside monthly SaaS fees. The biggest savings usually come from trimming overlapping tools, not from cutting the core rater or CRM.

CAPEX line

Capitalized software setup belongs in CAPEX only if your accounting policy treats it that way. If not, book onboarding, migration, and implementation as operating expense. Keep subscriptions, hosting, and gateway fees out of CAPEX so startup cash, P&L, and asset values stay clean.

Office And Equipment Startup Expense

Office shape

A home-based setup keeps cash in equipment, not rent. A shared office splits fixed cost, while a small retail office adds $3,000 rent, $400 utilities, and $250 supplies, or $3,650 a month before extra overhead. With $5,000 monthly non-office overhead, total recurring burn is $8,650 if you add the office.

Equipment buys

Office equipment is mostly CAPEX, not monthly burn: computers, monitors, phones, printer/scanner, desks, chairs, filing, signage, and basic security. Estimate it from unit counts times vendor quotes, then add leasehold improvements only for a leased space. Keep utility hookups, deposits, and office supplies separate.

Use units times quote

Separate deposits from assets

Track buildout apart

Cut fixed burn

The fastest savings come from avoiding a retail lease until client traffic justifies it. Home-based or shared office space cuts deposits, signage, and buildout, but it does not change revenue by itself. The decision mainly changes recurring burn, so compare the monthly run rate before you commit.

Delay retail space

Buy only needed gear

Watch monthly run rate

Pre-open cash

Treat rent deposits, utilities setup, and early office supplies as pre-opening cash outlays or operating expenses, not CAPEX. If you strip out $3,000 rent, $400 utilities, and $250 supplies, the office line drops by $3,650 a month while the base $5,000 overhead stays in place.

Launch Marketing And Market Access Startup Expense

Market access

This bucket covers carrier appointments, cluster membership, aggregator access, branding, referral materials, local search, paid leads, community marketing, and prospecting campaigns. Plan it as a split budget: $150,000 for producer-side marketing and $200,000 for customer-side marketing, or $350,000 total in Year 1. The mix drives how fast agents and buyers show up.

Producer CAC

Use $500 Year 1 producer CAC to size acquisition. Here’s the quick math: $150,000 / $500 = 300 producer-side acquisitions if spend hits plan exactly. This covers outreach, appointment work, and channel tests, but not guaranteed approvals or funded policies. Track cost per accepted agent, not just clicks.

Buyer CAC

$20 Year 1 customer CAC means $200,000 can buy 10,000 customer-side acquisitions on paper. That budget supports paid search, local search, referral materials, and community marketing. What this estimate hides: conversion rates, quote quality, and close time still control revenue timing, so watch booked apps and bound policies, not lead counts alone.

Timing risk

The real risk is timing, not spend. Carrier appointments and aggregator access can slow launch, so marketing may outpace revenue if approvals lag. Keep producer and customer campaigns separate, and review CAC by channel monthly so you can cut weak paid leads fast and shift money to the best local search or referral sources.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Lean fits a solo producer with no office, Base covers a small local office, and Full assumes a staffed ramp with paid marketing. Costs rise fast once payroll and acquisition spend kick in.

Lean, Base, and Full launch cost comparison

Scenario

Lean LaunchSolo producer

Base LaunchLocal office

Full LaunchGrowth funded

Launch model

Home-based launch with no dedicated office and about $5,650 in monthly non-office overhead.

Small office launch with $3,000 rent and about $8,650 in monthly fixed overhead.

Staffed launch with about $340,000 in Year 1 payroll and $350,000 in Year 1 marketing, plus the core office setup.

Typical setup

Use the core platform build, legal setup, and online sales flow, but skip rent and furniture.

Add a modest office, basic software, and the full core operating stack.

Add hired support, a bigger sales team, and heavier spend on customer acquisition.

Cost drivers

Platform development

Legal setup

Hosting and compliance

Non-office overhead

Office rent

Software licenses

Legal and accounting

Insurance

Marketing platform subscriptions

Payroll ramp

Paid marketing

Office rent

Support staff

Platform build

Planning rangeCAPEX only

$275,000 - $300,000Lower cash need

$300,000 - $350,000Mid-range budget

$950,000 - $1,100,000Largest funding need

Best fit

Best for a solo producer who wants to start lean and sell from home.

Best for a local office that needs a simple, steady launch.

Best for a growth-funded agency that needs scale from day one.

!

Planning note: These scenario ranges are researched planning assumptions built from the model inputs, not exact vendor quotes or live market pricing.

Yes, a home-based launch can work if your state licensing, carrier access, client meetings, and data-security setup allow it In this plan, removing office rent, utilities, and supplies cuts modeled fixed overhead from $8,650 to about $5,000 per month You still need software, legal and accounting, business insurance, marketing tools, licensing, and working capital

Yes, working capital is a separate cash reserve, not equipment spend The model starts $8,650 of monthly fixed overhead in Month 1, before adding $350,000 of Year 1 marketing and $340,000 of Year 1 payroll Since commissions are modeled at 90% of order value, cash can go out well before enough policies close

Revenue timing depends on licensing, carrier access, lead quality, sales cycle, and commission payment timing The model assumes expenses begin in Month 1, with customer support added in Month 13 and Year 1 marketing at $350,000 Use a runway plan that covers early ramp-up, because paid leads at $20 CAC still need conversion

You need a legal way to place business before selling policies, but the route can vary Options may include direct carrier appointments, cluster membership, aggregator access, or brokerage relationships Budget separately for appointment paperwork, compliance, and access fees The Year 1 revenue mix assumes 500% property and casualty, 400% life and health, and 100% specialty lines

For the researched small-office plan, start with $8,650 per month of fixed overhead before payroll, variable costs, and paid acquisition That includes $3,000 rent, $1,500 software, $2,000 legal and accounting, $500 business insurance, $400 utilities, $250 supplies, and $1,000 marketing platform subscriptions Then layer in CAPEX, licensing, deposits, and working capital

About the author

Martin Fletcher

Founder Support Writer

Martin Fletcher is a founder support writer at Financial Models Lab, focused on practical profit planning for founders writing a business plan. He helps small business owners understand how profit works, with clear guidance on startup cost estimates and the numbers to check before money is invested. His writing keeps the focus on useful figures and realistic expectations.

Choosing a selection results in a full page refresh.