Online Bank Startup Costs: $163M First-Year Operating Base

Online Bank

This online bank cost breakdown separates launch CAPEX, pre-opening expenses, working capital, and funding items that are not startup costs The researched model shows $57,000 in monthly fixed costs and $950,000 in first-year payroll, or $1634 million before variable costs, one-time CAPEX, regulatory capital, customer deposits, and lending capital

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates the capitalized startup assets needed to launch an online bank, before recurring operating costs and other funding needs.

!

Exclusions This covers capitalized launch assets only. Excludes salaries, legal retainers, regulatory filing fees, marketing, working capital, regulatory capital, customer deposits, loan funding, debt service, inventory, payroll runway, and other operating costs. Ongoing monthly items like $15,000 cloud hosting, $10,000 software licenses and APIs, $8,000 cybersecurity, and $4,000 data analytics should be budgeted separately.

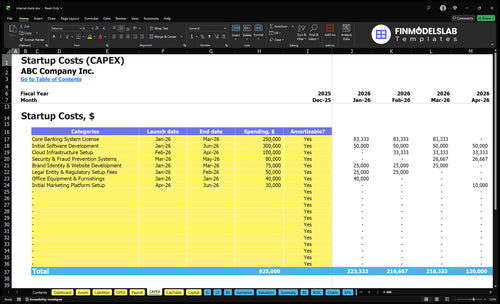

What does the CAPEX tab show?

Open Online Bank Financial Model TemplateCAPEX tab. Review startup-expenses, Month 1-60 timing, depreciation, amortization, working-capital, funding assumptions before fundraising.

Model screenshot highlights

Startup costs by category

Month 1-60 runway

Depreciation and amortization

Working capital funding

Online Bank Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

How does a bank charter change online bank startup costs?

Online Bank gets more expensive fast if it goes for its own charter, because that path adds regulatory application work, compliance buildout, governance, capital planning, examination readiness, and internal controls. A sponsor-bank or banking-as-a-service path can reduce that charter burden, but it adds partner due diligence, processor fees, contract limits, compliance oversight, and revenue-share economics. At the operating level, the visible costs here are a $12,000 monthly regulatory compliance and legal retainer, a $180,000 Head of Compliance salary, and regulatory capital that sits in a separate bucket from startup spend.

Charter path costs

More application work up front

More governance and controls

More exam-readiness preparation

More capital planning discipline

Sponsor-bank tradeoffs

Less charter work, more partner checks

Processor fees and revenue share

Contract limits on products

Ongoing compliance oversight still required

How much money do you need to start an online bank in the US?

For an Online Bank, a practical first-year startup expense base is $1.634 million before variable costs and one-time CAPEX: $57,000/month fixed overhead equals $684,000/year, plus $950,000 payroll. That is not the same as total funding need; What Is The Main Indicator That Shows The Growth Of Your Online Bank? matters because deposits, loans, and earning assets sit on the balance sheet, not just the launch budget. A regulated banking business may need capital beyond startup costs, and the final number changes with charter route, product scope, technology build, and compliance depth.

Startup Expense Base

Use $57,000 monthly fixed overhead

Annual fixed overhead: $684,000

Add first-year payroll: $950,000

Subtotal before extras: $1.634 million

Balance Sheet Funding

$20 million first-year deposits

$125 million first-year loans

$105 million other interest-earning assets

Not basic opening expenses

What hidden costs of starting an online bank should founders plan for?

Hidden costs for an Online Bank are mostly the control layers around the product, not the app itself. If you’re sizing the business, start with the revenue side too: How Much Does The Owner Of An Online Bank Usually Make? shows why these costs can eat runway fast, even when interest income looks strong.

Here’s the quick math: plan for $12,000/month compliance and legal, $8,000 cybersecurity services, $3,000 insurance-related FDIC fee assumption, and $4,000 for data analytics, all as operating costs. Separate working capital from excluded funding needs like customer deposits, loan portfolio capital, and regulatory capital; Year 1 interest income of $1,775 million and interest expense of $290,000 leave $1,485 million before overhead, so the hidden costs matter.

Core hidden costs

BSA/AML and KYC controls

Fraud monitoring and alerts

Cybersecurity audits and testing

Vendor due diligence and reviews

Budget buckets

$12,000 monthly compliance retainer

$8,000 cybersecurity services

$3,000 insurance-related FDIC fee

$4,000 data analytics platform

Calculate Fuding Needs

Startup cost summary

This table summarizes startup CAPEX and excluded cash needs for an online bank using researched planning assumptions.

Regulatory capital, deposits, and operating runway

No

Online Bank Core Five Startup Costs

Regulatory Setup And Compliance Readiness Startup Expense

Launch Path

A digital bank starts with the charter or sponsor-bank path, plus policies, governance, BSA/AML, KYC, reporting controls, vendor oversight, and application support. Keep these setup costs separate from regulatory capital and ongoing exams. The base run rate is $12,000 a month for legal and compliance, plus $3,000 monthly insurance fees.

Budget Base

The biggest staffing anchor is the Head of Compliance at $180,000 a year, or about $15,000 a month before benefits. Add the $12,000 monthly legal retainer and $3,000 FDIC insurance fee, and the steady compliance base is about $30,000 a month, or $360,000 a year, before filings and systems.

Phase It

Launch in phases if you can. Deposits, lending, credit cards, and payments all at once raise the number of controls, tests, and approvals you need; one product at a time keeps the setup smaller. The main mistake is hiring for full volume too early. Tie vendor reviews and reporting to the first product set only.

Scope Drives Spend

If deposits, lending, cards, and payments launch together, compliance staffing, monitoring, and application work rise fast; if you phase them, the setup bill stays lower. One clean rule: scope first, spend second. That choice sets the size of your control stack, your vendor oversight, and how much pre-launch legal support you need.

Core Banking Platform And Digital Infrastructure Startup Expense

Platform Build

The core banking stack is a split budget: one-time implementation work on one side, and recurring tech run rate on the other. The operating base is $29,000 per month, or $348,000 a year, before payroll.

Cost Drivers

This bucket covers core ledger, account opening, mobile and web banking, application programming interfaces (APIs), cloud hosting, data architecture, integration work, and implementation. Price it with vendor quotes, months of coverage, and system count, then separate capitalized build work from recurring subscriptions and maintenance.

Manage Spend

Keep the first release tight: core ledger, account opening, mobile and web access, and the needed APIs. Push nonessential analytics and custom integrations to phase two so you do not pay for full-stack complexity before traffic proves it. What this estimate hides is integration drag: every extra system raises testing, support, and vendor oversight.

Phase the launch by module.

Cap custom integrations early.

Track CAPEX and OPEX separately.

CAPEX Split

Classify software build work that creates a long-lived asset as CAPEX; treat subscriptions, hosting, maintenance, and payroll as operating spend. With $520,000 of first-year payroll for the CTO and two senior engineers, the tech team is a major burn item, so the launch plan should say what ships now and what waits.

Cybersecurity, Fraud, Identity, And Risk Control Startup Expense

Security at launch

An online bank needs security on day one, not after launch. A workable base assumption is $8,000 per month for penetration testing, security operations monitoring, encryption, vendor risk management, identity verification, transaction monitoring, fraud tools, and security audits.

Cost inputs

Estimate this from months of coverage, vendor quotes, and Year 1 volume. With $15 million in credit card loans, $5 million in personal loans, and $20 million in deposits, KYC and fraud review load rises fast. That drives the spend you need for tools, alerts, and audit support.

Use monthly vendor quotes

Count loan and deposit volume

Price for audit-ready controls

Keep it tight

Use one core stack where it works, but keep testing and monitoring independent. Start with the $8,000 monthly base, then add only what card, loan, and deposit activity needs. Heavy card use means more disputes, alerts, and loss-control work, so underbuying here usually gets expensive later.

Phase noncore tools

Reuse vendor reports

Review alerts weekly

Volume pressure

If loan and card volume grows before controls do, fraud losses and dispute work can outrun revenue. Tie spend to transaction count, not headcount alone, and refresh vendor risk reviews as new processors, KYC tools, or data feeds come online.

Payment Rails, Card Program, And Network Integration Startup Expense

What it covers

Payment-rail setup covers ACH, wires, debit card issuing, card processing, optional ATM access, settlement ops, sponsor-bank integrations, reconciliation, and processor onboarding. The setup bill depends on sponsor-bank, processor, transaction volume, and product scope. Keep it separate from per-transaction fees so launch cost and run cost do not blur.

How to size it

Use units × unit price: one-time integration work, then monthly vendor and staff run-rate. Anchor the scope to $8 million checking deposits, $10 million savings deposits, and $2 million CDs in Year 1. Ask for quotes on onboarding, reconciliation, and settlement before you lock the budget.

Sponsor-bank setup quote

Processor onboarding fee

Monthly reconciliation cost

How to control it

The cheapest safe path is to phase scope. Start with the rails needed for the first deposit products, then add ATM access only if customers will use it. In Year 1, model 60% card interchange fee expense and 80% customer acquisition costs as variable drag, so launch volume matters as much as setup cost.

Phase by product need

Skip unused rails

Separate fixed from variable

Year 1 mix

With $8 million checking, $10 million savings, and $2 million CDs, payment rails must support deposits, settlement, and reconciliation from day one. If the product mix leans hard on cards, Year 1 gets expensive fast because 60% interchange expense and 80% acquisition cost hit the same launch window.

Professional Services, Launch Team, And Readiness Startup Expense

Pre-open fees

For an online bank, most banking attorneys, compliance consultants, finance advisors, auditors, and risk consultants are pre-opening expenses, not CAPEX. Budget them as quote-based fees plus months of work, then separate one-time launch support from ongoing controls. This is the spend that gets the charter, policies, and launch files ready before deposits and loans go live.

Launch payroll

The first-year salary base is $950,000: CEO $250,000, CTO $220,000, Head of Compliance $180,000, and two senior software engineers totaling $300,000. Add $57,000 per month in operating readiness costs for launch management, product work, engineering readiness, and customer support setup. This is working capital, so map it by headcount and months before traction.

Count pre-launch months.

Separate fixed pay from setup fees.

Delay hires tied to traction.

Hire timing

Hire the roles that protect launch first: compliance, legal, risk, and core product readiness. Push some customer support, finance support, and extra engineering capacity until deposits and loan volume justify them. The key question is simple: which roles must exist on day one, and which can wait until account growth covers the $57,000 monthly readiness burn?

Front-load control roles.

Delay noncritical support.

Review headcount monthly.

Budget split

Classify most of this spend as pre-opening expense or working capital, not CAPEX. That keeps the model honest: setup fees hit launch cost, while payroll and readiness burn bridge you to deposits and loan traction. One clean rule helps: if the item builds the bank’s operating muscle, it belongs in startup cash, not fixed assets.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Lean, base, and full launches change cost fast because product count, compliance depth, integrations, and staff move together. The base case matches the model; the other two show lighter or heavier builds.

Lean, base, and full online bank launch cost comparison

Scenario

Lean LaunchSponsor-bank path

Base LaunchModel match

Full LaunchCharter-heavy

Launch model

Use a sponsor-bank path, launch core accounts and a narrow loan set, and keep compliance and integrations light.

Use the researched operating base with deposits and lending scaled to core products and standard compliance.

Pursue broader charter work, more products, deeper compliance, and more integrations from day one.

Typical setup

Run a small team, basic integrations, and focused marketing to test deposits and loan demand.

Build for checking, savings, deposits, and the core loan mix with a fuller launch team and standard integrations.

Staff up across compliance, tech, risk, and marketing while supporting a wider product and funding plan.

Cost drivers

Sponsor-bank fees

fewer products

lighter integrations

smaller launch team

narrow marketing

Core products

standard compliance

deposits and loans

full launch team

regular marketing

Charter work

deeper compliance

more integrations

larger staffing

higher marketing

Planning rangeCAPEX only

$850,000 - $1,200,000Lower setup cost

$1,550,000 - $1,700,000Research base

$2,250,000 - $3,500,000Higher capital need

Best fit

Best for founders who want a narrower, faster start and can live with limited products and a lighter regulatory build.

Best for teams using the model's main assumptions, including $57,000 monthly fixed costs, $950,000 payroll, $20 million deposits, and $125 million loans.

Best for teams that want a broader launch and can fund a slower, more complex regulatory build.

!

Planning note: These ranges are researched planning assumptions, not vendor quotes or guaranteed budgets.

Using the researched assumptions, plan for at least $1634 million in first-year fixed overhead and core payroll before variable costs and one-time CAPEX That includes $57,000 per month in fixed costs and $950,000 in first-year salaries It excludes $20 million of first-year deposits and $125 million of first-year loans because those are balance sheet funding needs

Not always, but the choice drives cost and control A chartered online bank carries heavier regulatory setup, capital planning, governance, and examination readiness A sponsor-bank or banking-as-a-service model may reduce charter work but adds partner oversight and integration costs In this model, compliance already includes a $12,000 monthly legal retainer and a $180,000 Head of Compliance

Pre-launch costs usually include compliance setup, technology implementation, cybersecurity, professional services, staffing, and payment integrations The model starts Month 1 with $15,000 cloud hosting, $10,000 software licenses and APIs, $8,000 cybersecurity services, and $12,000 regulatory compliance and legal retainer Payroll adds about $79,000 per month from a $950,000 first-year team

Usually it is both The model includes recurring bought technology, such as $10,000 per month for software licenses and APIs, $15,000 for cloud hosting, and $4,000 for data analytics It also includes build capacity through a $220,000 CTO and two senior software engineers at $150,000 each in Year 1

Start with monthly cash burn, then add a cushion for launch delays and compliance timing In this model, fixed costs are $57,000 per month and first-year payroll averages about $79,000 per month, so baseline monthly overhead is roughly $136,000 before variable costs Six months of that base is about $817,000, excluding CAPEX, regulatory capital, deposits, and loan funding

About the author

Timothy Dawson

Small Business Educator

Timothy Dawson is a small business educator at Financial Models Lab who helps readers understand the numbers behind everyday business ideas, with a focus on pricing, margin basics, and the common business costs that shape early decisions. He writes about the practical choices founders need to make before launch, especially when planning the first months after a business opens and evaluating whether an idea makes sense.

Choosing a selection results in a full page refresh.