Microfinance Institution Startup Costs: $625M First-Year Lending Plan

Microfinance Institution

Key Takeaways

Technology alone runs $40,000 monthly before implementation.

Facility costs add $10,500 monthly, even in lean setups.

Three core roles cost $395,000 yearly before benefits.

Capacity must match the $625 million first-year loan plan.

Microfinance CAPEX Calculator Objective

Startup CAPEX Calculator

This estimates capitalized startup assets only, so you can size the opening investment before launch.

!

What this excludes Shows opening asset investment only. Excludes Month 1 fixed operating cost of 98000, annual fixed overhead of 1176000, excluded first-year loan capital of 625000000, inventory, payroll runway, deposits, debt service, working capital, marketing spend, monthly software, monthly hosting, loan loss reserves, and legal fees expensed before opening.

How should a microfinance startup funding plan support financial projections?

The funding plan for a Microfinance Institution has to match loan disbursement timing, because cash goes out before interest income comes in. With the researched first-year loan yield assumptions of 115% on microenterprise loans, 95% on credit builder loans, 160% on personal installment loans, 88% on secured auto loans, and 125% on working capital lines, first-year loan interest is about $700,500 before credit losses and operating costs. It should also show the funding base: $3 million in checking deposits, $2 million in savings deposits, $1 million in certificates of deposit, $1 million in Federal Home Loan Bank advances, and $25 million in grants and subordinated debt.

Cash timing

Show loan disbursement dates first

Track $700,500 interest before costs

Reserve for credit losses early

Plan for cash out before income

Funding mix

Use $3M checking deposits

Add $2M savings deposits

Include $1M CDs and advances

Backstop with $25M grants and subordinated debt

How much money do you need to start a microfinance institution?

You need to separate opening cost from total funding: a Microfinance Institution has at least $1.176 million in first-year fixed operating costs before loan capital, because fixed overhead is $98,000/month. For the full funding plan, add loan capital, reserves, and runway; the listed first-year loan mix totals $42.25 million, so don’t collapse lending capital into startup CAPEX; for setup steps, see How Do I Start A Microfinance Institution?.

Opening cost

Cover licensing and compliance setup

Fund technology, office, and insurance

Staff readiness includes CEO at $175,000

Fixed costs run $98,000/month

Total funding

Add loan capital separately

Microenterprise loans: $25.0M

Credit-builder loans: $15.0M

Other listed loans: $2.25M

What hidden microfinance working capital and pre-opening expenses should founders expect?

Founders should budget beyond build-out: a Microfinance Institution can carry $18,000 a month for loan loss provision and $12,000 for marketing and community outreach from Month 1, plus payroll runway, compliance monitoring, borrower outreach, legal work, audit readiness, cybersecurity controls, staff training, and delayed interest income during ramp-up. The first-year loan capital is $625 million, and other interest-earning assets add $2 million ($1 million cash and equivalents, $500,000 government securities, $250,000 CDFI bonds, and $250,000 interbank deposits), so these are working capital needs, not simple CAPEX; for KPI context, see What Are The 5 KPIs For Microfinance Institution?

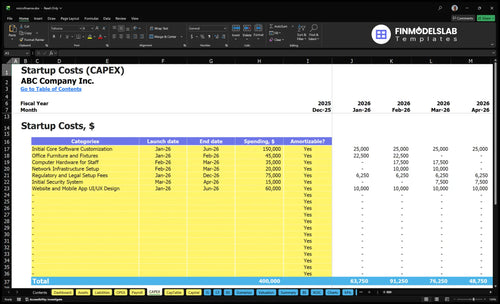

Customer-facing digital onboarding and interface design

Yes

Office Furniture and Fixtures

$45,000

Branch and office setup

Yes

Computer Hardware for Staff

$35,000

Staff workstation and device rollout

Yes

Excluded Loan Fund Capital

$625,000,000

First-year lending capital held outside CAPEX

No

Microfinance Institution Core Five Startup Costs

Regulatory, Licensing, Legal, and Compliance Setup Startup Expense

Compliance Scope

Start with entity formation, state lending licenses, consumer finance rules, borrower disclosures, fair-lending controls, policy manuals, board governance, legal review, audit readiness, and monitoring. Requirements change by state, products, rates, nonprofit status, deposit plans, and whether banking is direct or through partners. If deposits are accepted, Federal Deposit Insurance Corporation and bank-level rules can move the budget fast.

Monthly Legal Run-rate

Use the provided $10,000 per month for ongoing legal and audit planning support, not as a one-time license quote. Add $7,500 per month for insurance where regulatory or board coverage applies. That is $17,500 per month, or $210,000 per year, before state filing fees, outside counsel, or any bank-level deposit work.

What Drives Cost

Scope it by the number of states, the loan products offered, and whether you take deposits or partner for banking. One line: more products, more controls. Ask for quotes tied to filings, policy work, disclosures, and board support, then map them to launch months so you can separate pre-opening cash from steady-state compliance spend.

Count states and product lines.

Separate filings from ongoing support.

Model deposit-taking as a step-up.

Budget Guardrails

Keep a live compliance calendar for renewals, board approvals, exams, and disclosure updates. The cheapest mistake here is over-documenting early and under-documenting later. If you plan to accept deposits, budget for a materially higher legal, insurance, and audit load because FDIC-type requirements can add review layers, evidence trails, and stronger controls.

Lending Technology and Secure Systems Startup Expense

Core systems

This cost covers loan origination, underwriting, borrower records, payment tracking, servicing, collections, reporting, customer relationship management, cybersecurity, data storage, cloud hosting, and integrations. Keep one-time implementation separate from monthly subscriptions and IT support, or launch cash needs will look too low. Software is not the same as setup work.

Price check

Here’s the quick math: $25,000 a month for core banking software plus $15,000 for data security and cloud hosting equals $40,000 monthly, or $480,000 a year. That excludes unprovided implementation CAPEX, so get vendor quotes for setup, migration, and IT support before you lock the budget.

Keep it lean

Start with only the modules you need at launch. Delay deposit accounts, real-time payments, multi-state reporting, automated underwriting, and stronger cybersecurity controls until the product is live and the control stack is ready. One common mistake is paying for full-function software before the team can use it.

Budget load

The $480,000 annual technology overhead is the baseline, not the ceiling. Costs rise as you add deposit accounts, real-time payments, multi-state reporting, automated underwriting, and tighter cybersecurity controls. Build the budget around the features you truly need on day one, then phase the rest as usage and compliance demands grow.

Office, Branch, Equipment, and Physical Setup Startup Expense

Facility Cost

A microfinance office does not need a full bank branch, but it still needs private borrower space, secure records, and reliable connectivity. The modeled facility cost is $8,500 rent plus $2,000 for utilities and telecom, or $10,500 a month. That annualizes to $126,000 before buildout, furniture, computers, and security systems.

Estimate Inputs

Here’s the quick math: base rent, lease deposit, and monthly utilities are only the start. Add quotes for basic buildout, furniture, computers, secure networking, signage, accessibility, meeting rooms, borrower intake space, safety controls, and hybrid service tools. The missing CAPEX can move the startup budget a lot.

Lease term and deposit size

Square feet and buildout quote

Count computers and network gear

Lean Layout

Lean community models can shrink the footprint, but they cannot skip privacy, accessibility, or secure connectivity. Keep one intake room, a small meeting area, and locked records storage, then use hybrid service tools for simple service work. What this estimate hides is the one-time cost for buildout, furniture, computers, and the security system.

No-Branch Trap

Don’t overbuild for a bank-style branch unless the service model truly needs it. Spend on the controls that protect borrowers and files: private meetings, safe access, reliable internet, and secure storage. That keeps the site usable for daily lending work without tying up cash in unnecessary space.

Staffing Readiness and Pre-Opening Payroll Startup Expense

Pre-Launch Payroll

Pre-opening payroll is a launch cost, not steady-state overhead. One CEO at $175,000, one CFO at $150,000, and one loan officer at $70,000 total $395,000 before payroll taxes, benefits, recruiting, training, or contractors. If underwriting, servicing, collections, and compliance must support a $625 million first-year loan plan, this team has to be ready before launch.

What It Covers

This cost covers management, finance, loan origination, underwriting, servicing, collections readiness, compliance oversight, bookkeeping, and staff training before opening. Size it from headcount × salary, then add pre-launch months for hiring and training. One clean rule: if a role must approve loans or controls on day one, it belongs in startup payroll, not later operating spend.

Use months of runway, not guesses.

Add taxes, benefits, recruiting.

Stress-test for loan volume.

Keep It Lean

Keep pre-opening payroll separate from ongoing payroll after launch. The big mistake is booking only salaries and missing payroll load, contractor help, and training time, which can push cash need well above $395,000. If onboarding slips, collections and compliance coverage start late, and that raises risk before the first loan book is live.

Capacity Match

Headcount has to match the $625 million first-year plan, not just the org chart. If underwriting or compliance are thin, growth slows and control risk rises at the same time. A lean start can save cash, but it should not cut the staff needed to review files, monitor loans, and keep records clean from day one.

Professional Services, Insurance, Marketing, and Launch Readiness Startup Expense

Launch Burn

This cost is real pre-opening cash burn. The model puts marketing and community outreach at $12,000 per month, professional fees at $10,000, and insurance at $7,500, or $29,500 per month and $354,000 per year. Treat most of it as early launch spend unless accounting rules support capitalization.

What It Covers

Use this bucket for accounting, audit readiness, legal review, website setup, borrower education, referral partnerships, grant materials, and launch marketing. Price it with vendor quotes and months of coverage. The clean estimate is scope × monthly fee × launch months, then split one-time build items from recurring spend.

Control The Burn

Cut spend without cutting compliance. Bundle legal and accounting work, cap agency retainers, and use channels that already reach borrowers. The common mistake is buying broad branding before the loan pipeline is ready. Watch the $29,500 monthly run rate; every extra month adds $29,500.

Fit To Portfolio

Borrower acquisition has to match the first-year mix, especially $25 million in microenterprise loans and $15 million in credit-builder loans. If outreach skews too wide, you pay for leads that do not fit the product. One line: the channel mix should feed the loan mix.

Lean, Base, and Full-Service Microfinance Startup Cost Scenarios

Scenario table

Scenario scale changes cash need fast here. Lean keeps the footprint tight; Base matches the model; Full adds more coverage, staff, systems, and funding.

Lean, Base, and Full launch cost comparison

Scenario

Lean LaunchSmall footprint

Base LaunchCore model

Full LaunchHigh complexity

Launch model

Launch with one region, fewer products, and partner-based banking services.

Launch with the model's core product mix, standard staff, and deposit-taking operations.

Expand into broader state coverage with more products, deeper systems, and a larger compliance team.

Typical setup

Use a small office, limited geography, and quote-needed capex.

Use the researched model: $98,000 monthly fixed costs, $1.176 million year-one fixed overhead, $6.25 million loans, $2.0 million other earning assets, and $9.5 million liabilities and funding sources.

Add more staff, stronger software, and more deposit-taking capacity for a wider launch.

Cost drivers

Small office

partner banking

fewer loan products

light tech stack

lean compliance

98k monthly fixed costs

6.25M first-year loans

2.0M other earning assets

9.5M liabilities and funding

standard staffing

Broader coverage

deeper software stack

larger compliance team

more deposit products

higher loan capital

Planning rangeCAPEX only

Quote-needed setup bandLower funding

Model anchor funding bandBase funding

Higher-capital expansion bandHeavy funding

Best fit

Best for founders testing demand with low regulatory load and tight cash.

Best for operators who want the core footprint and a manageable compliance build.

Best for teams with strong funding, larger regulatory capacity, and a faster scale plan.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes.

The researched model shows $98,000 in fixed monthly costs from Month 1 before full payroll detail, loan disbursements, and one-time CAPEX The largest listed monthly items are $25,000 for core banking software, $18,000 for loan loss provision, and $15,000 for data security and cloud hosting This is operating overhead, not loan capital

Yes, loan fund capital should be separate from startup CAPEX and opening expenses The first-year lending plan totals $625 million across five products, including $25 million in microenterprise loans and $15 million in credit builder loans You also need reserves and runway because interest income arrives over time, not on day one

Build the launch budget around at least the first operating year, then test it across the full 60-month model The researched assumptions start fixed costs in Month 1 and carry them through Month 60 First-year fixed overhead alone is $1176 million, before complete payroll burden, one-time CAPEX, or borrower-default volatility

The best mix depends on whether the institution accepts deposits, uses debt, wins grants, or lends through partners The researched first-year funding side includes $3 million in checking deposits, $2 million in savings deposits, $1 million in certificates of deposit, $1 million in Federal Home Loan Bank advances, and $25 million in grants and subordinated debt

Yes, structure changes legal setup, tax treatment, grant eligibility, investor return expectations, governance, and compliance work The operating cost base may still look similar if both models need licensed lending, secure software, staff, and loan servicing Use the same core cost buckets, then adjust funding assumptions such as the $25 million grants and subordinated debt line

About the author

Grace Hall

Startup Planning Writer

Grace Hall is a startup planning writer at Financial Models Lab, where she creates simple financial projections that help founders make business ideas easier to evaluate. She focuses on the numbers behind everyday businesses, especially for people planning to open a physical location. Grace writes about cost and income assumptions in a clear, practical way, helping readers understand what it really takes to open a business and build a realistic plan.

Choosing a selection results in a full page refresh.