Mixed-Use Development Startup Costs: $160M+ Planning Budget

For this mixed-use development, known land purchases and construction budgets total $1600 million, before the listed $405,000 in startup capital expenditures (CAPEX), site-control rent, overhead, reserves, and working capital The 60-month model reaches breakeven in Month 26, but the cash low point is -$1406 million in Month 36, so funding must cover the build period and early ramp-up

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a mixed-use development project.

!

Exclusions Excludes inventory, payroll runway, deposits, debt service, working capital, the $40k monthly rented site-control cost once both rented components are active, and other operating costs.

What hidden costs should a mixed-use development budget include?

If you’re asking what a How Much Does The Owner Of A Mixed-Use Development Typically Make? budget should really include, the hidden costs are the soft costs and cash gaps, not just bricks and steel. In Mixed-Use Development, that means entitlement delays, environmental remediation, utility upgrades, traffic studies, legal fees, insurance during construction, property taxes, lender reserves, marketing, brokerage commissions, model units, and operating cash before stabilization. The model already assumes $60k for feasibility and market research, $150k for architecture and engineering, $30k for legal formation and initial permits, and $50k for initial marketing, so the real risk is the cash burn before income starts.

Soft Costs

Entitlement delays can push schedules.

Environmental remediation can add big cleanup costs.

Utility upgrades often land off budget.

Traffic studies and permits add more spend.

Cash Drag

Property taxes hit before stabilization.

Lender reserves protect the downside.

Marketing, brokerage commissions, and model units cost cash.

The model flags -$1406M minimum cash in Month 36.

What belongs in a mixed-use development funding plan?

A Mixed-Use Development funding plan should show the full capital stack: sources and uses, land equity, construction debt, sponsor equity, preferred equity if used, plus draw schedule, lease-up assumptions, debt sizing, interest reserves, operating reserves, and exit timing. In this model, the six phased assets start construction from Month 8 through Month 27, hit breakeven in Month 26, and target sale and payback in Month 60. After the cost estimate is built, test IRR, ROE, the funding gap, and downside lease-up cases so the capital plan can hold if absorption slips.

Core funding stack

Sources and uses set the base.

Show land equity clearly.

Include construction debt and equity.

Add reserves for cash gaps.

Model checks

Test IRR after cost build.

Test ROE on each phase.

Stress lease-up timing by month.

Check sale at Month 60.

How much money do you need for a mixed-use development?

For a Mixed-Use Development, fund the cash curve, not a universal headline number: this base case needs about $1,406M at peak in Month 36. The quick math behind What Is The Current Growth Trajectory Of Your Mixed-Use Development Project? includes $450M land, $1,150M construction, $405k startup CAPEX, $303k monthly fixed overhead, and $4.375M Year 1 payroll, with breakeven in Month 26 and payback in Month 60.

Funding base case

Land purchases: $450M

Construction budget: $1,150M

Startup CAPEX: $405k

Year 1 payroll: $4.375M

Cash gap drivers

Site-control rent before closing

Financing reserves and working capital

Debt sizing and equity contribution

Leasing pace and operating deficits

Calculate Fuding Needs

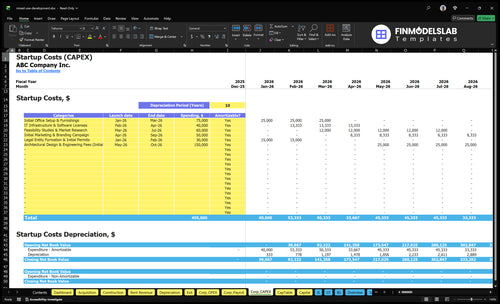

Startup cost summary

This table breaks the mixed-use project into acquisition, construction, launch, and non-CAPEX reserve needs before stabilization.

Highlighted CAPEX$160,405,000Base planning example

Excluded cash needs$140,567,000Outside CAPEX total

Operating deficits and debt service gap before breakeven

No

Mixed-Use Development Core Five Startup Costs

Land Acquisition and Site Due Diligence Startup Expense

Land First

Treat land as its own bucket, because location and zoning can swing the deal. The base case has $450M in owned-site purchases across four components, bought from Month 3 through Month 18. Model earnest money, title, survey, appraisal, Phase I, geotechnical, zoning, legal, and closing costs separately.

Diligence Stack

This bucket covers deposits and third-party checks before closing. Use quote-based inputs for earnest money, title, survey, appraisal, Phase I environmental assessment, geotechnical review, zoning review, legal review, and closing costs. Keep each parcel separate, because one clean report does not carry to the next.

Release deposits by milestone.

Order Phase I early.

Verify zoning before funding.

Site Control Rent

For leased control, budget $25k per month for one component and $15k per month for the two rented components where applicable. Multiply monthly rent by the control period from signing to closing or conversion, and keep it outside hard cost so the land line stays clean.

Track rent by parcel.

Stop paying when control ends.

Link rent to closing timing.

Timing Risk

Month 3 to 18 is the danger zone: delay can stack rent, carry costs, and extra diligence before any revenue starts. Phase the buys, tie deposits to milestones, and do not overfund site control on parcels that may fail zoning or environmental review.

Entitlements, Permits, Design, and Professional Fees Startup Expense

Soft Costs First

Entitlements, permits, design, and professional fees are soft costs, not construction. For this mixed-use project, plan for $240k in source startup CAPEX: $60k feasibility and market research, $30k legal entity formation and initial permits, and $150k initial architecture and engineering before hard costs start.

What It Covers

This bucket covers rezoning, site plan approval, legal counsel, civil engineering, architecture, structural design, mechanical-electrical-plumbing design, traffic studies, code review, permit fees, and consultants. Here’s the quick math: budget by scope, quote count, and month of coverage, with work timing aligned to Month 3 through Month 10 before construction.

Use scoped consultant bids.

Track permit and review counts.

Budget for Month 3-10 work.

Keep Scope Tight

Control this cost by locking the design brief early, bundling consultant work, and getting city feedback before drawings get too far. The main mistake is starting too late or changing the plan after reviews begin, which forces rework and more fees. That can raise cash needs without adding any revenue.

Freeze scope before full design.

Ask cities early on zoning.

Avoid redesign after submittal.

Watch the Timing

Delays here matter because these are pre-construction dollars. If approvals slip past Month 10, funding needs can move earlier than expected, before any rental or sale revenue starts. Keep the entitlement path, permit path, and design path synced so the project doesn’t stall between land control and vertical build.

Sitework, Utilities, Infrastructure, and Parking Startup Expense

Scope

Sitework covers demolition, grading, stormwater, sewer, water, power, sidewalks, landscaping, street work, surface parking, structured parking, accessibility upgrades, and utility tie-ins. Cost moves with site condition, municipal rules, density, parking ratios, and whether structured parking is needed. For this mixed-use deal, the source data does not isolate sitework from the $1,150M construction budget.

Budget setup

Put this line item inside hard construction until bids arrive, or break it out from contractor estimates. That keeps the model honest when site risk is still unclear. The key input is not a fixed dollar amount yet; it’s the scope split across demolition, utilities, paving, and parking, then priced once the site plan and bid set are real.

Cost drivers

Parking is the swing factor. A low-density site with surface parking costs far less than one that needs structured parking. Municipal street and sidewalk upgrades can also add scope fast. If the site needs major utility upgrades, off-site work, or cleanup, the cash need rises before vertical construction starts.

Refine before bid

Get these answers early so the estimate is usable: utility capacity, environmental cleanup, off-site improvements, and the exact parking count. Those four items can change the sitework budget more than small design tweaks. If any of them are unresolved, keep the cost in hard construction and avoid pretending the number is fixed.

Confirm utility capacity first

Check cleanup scope early

Lock parking count before pricing

Vertical Construction and Building Shell Startup Expense

Shell Build Budget

This is the largest hard-cost line. Base case construction budgets total $1,150M across six components, with packages from $50M to $350M and build times of 8 to 18 months. It covers foundations, structure, envelope, roof, MEP, elevators, life safety, common areas, residential units, and commercial and retail shell delivery.

What to Include

Build the estimate from scope, not from a fake per-square-foot shortcut. Use trade bids, design stage, and package timing to size each line: foundations, structure, envelope, roof, MEP, and tenant-shell work. The budget should also reflect start timing from Month 8 through Month 27, since phasing changes cash need.

Six package budget lines

$50M to $350M per package

8 to 18 months per package

What Drives Cost

Cost moves with building height, materials, labor market, code rules, phasing, and start timing. Taller buildings and tighter codes push structural, fire, and elevator spend up fast. If the project starts during a busy labor window, quotes can move before work begins, so cash planning needs to match the bid schedule, not just the design schedule.

Cost Control

Hold back fake precision until gross square footage is known. The cleanest way to protect the budget is to lock scope by package, stage bids early, and watch phasing gaps that add remobilization cost. If code changes or start timing slips, the shell budget can rise before revenue starts, so contingency needs to sit inside the hard-cost plan.

Tenant Improvements, Leasing Launch, and Pre-Opening Startup Expense

Lease-Up Budget

Keep tenant fit-out and opening costs separate from the shell. This bucket covers tenant improvement allowances, retail demising, signage, residential amenities, model units, brokerage commissions, marketing, insurance, property management setup, and operating readiness. The startup plan includes $50k for initial marketing and branding, so this is a real launch line, not core construction.

How to Price It

Price each item from scope, quotes, and timing. Use unit counts for model units, broker proposals for commissions, and months of coverage for launch spend. Operating assumptions show leasing and marketing commissions at 30% of revenue in Year 1, stepping to 10% by Year 5. Property management fees start at 40% in Year 1.

Count units needing upgrades

Quote brokers before launch

Budget months, not guesses

Control the Spend

Push reusable work into construction and keep opening costs lean. One signage package, phased model-unit buildout, and shared amenity standards can cut waste without hurting leasing. Watch for double counting: if launch costs sit inside hard construction and again in ops, the budget gets bloated fast. Common-area utilities and maintenance run at 20% in Year 1.

Phase model-unit buildout

Reuse shared amenity items

Lock broker terms early

Pre-Opening Readiness

Budget launch work by month, not by instinct. Lease-up staffing, insurance, marketing, property management setup, and operating systems must be funded before occupancy starts. In a mixed-use project, the lender should see this as a separate readiness pool, since it does not build the asset itself but it does decide when rent can start.

Compare 3 Startup Cost Scenarios

Scenario table

Scale changes this project fast: bigger land, harder entitlements, parking, and tenant build-outs push cash needs up. Lean is easiest to fund; Full carries the widest gap.

Lean, Base, and Full show how site scope drives funding needs.

Scenario

Lean LaunchBest fit: infill

Base LaunchCore case

Full LaunchBest fit: large site

Launch model

Use a smaller infill redevelopment with simpler entitlements and reused infrastructure.

Run the researched base case with owned land, phased construction, and Month 26 breakeven.

Expand the site with structured parking, heavier amenities, and broader tenant build-outs.

Typical setup

Keep parking limited and trim tenant improvements to the essentials.

Model $450M land purchases, $1.15B construction, $405k startup CAPEX, and Month 36 peak cash gap.

Add longer entitlement work, higher reserves, and more upfront tenant improvements.

Cost drivers

Simpler entitlements

reused infrastructure

limited parking

fewer tenant improvements

Land purchases

construction budget

startup CAPEX

peak cash gap

Structured parking

heavier amenities

tenant improvements

longer entitlements

higher reserves

Planning rangeCAPEX only

Below $1.60BLower funding risk

$1.60B baseMonth 36 cash gap

Above $1.60BHighest funding risk

Best fit

Use this when the site is compact, approvals are simpler, and you want the lightest cash load.

Use this when you want the model in the brief and need a grounded funding plan for the full mixed-use stack.

Use this when the site is more complex, tenants need more finish work, and you need extra reserve capacity.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes, and they should be used as budgeting bands until site scope is locked.