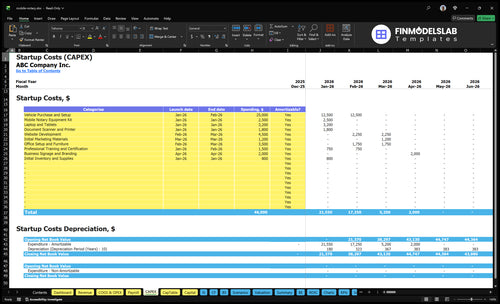

Mobile Notary Startup Costs: $46K Setup Before Working Cash

You’re planning a traveling notary service, so the budget has to cover state authorization, supplies, insurance, vehicle readiness, technology, marketing, pre-opening work, and operating cash The researched model carries $46,000 of startup setup costs across the startup period, plus $1,049 in monthly fixed overhead before payroll and $8,000 of Year 1 marketing These are planning assumptions, not quotes or guarantees, and the model reaches breakeven in Month 34

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a mobile notary launch.

!

What this leaves out This calculator covers CAPEX only. It excludes training, licensing, bond, insurance, marketing, supplies, inventory, payroll runway, owner draw, debt service, deposits, working capital, fuel, software subscriptions, and other non-CAPEX startup cash needs.

How much money do I need to start a mobile notary business?

You need about $46,000 to start a Mobile Notary in this model before working capital; fund it as CAPEX plus pre-opening costs plus early operating cash, not one fixed universal number. If you already have a suitable vehicle, setup cash drops by $25,000 to about $21,000, but the ramp still matters because the model shows negative EBITDA of $34,000 in Year 1 and breakeven in Month 34; track the right driver with What Is The Most Critical Measure For The Success Of Mobile Notary Services?.

Setup cash

$25,000 vehicle purchase

$4,500 website development

$3,200 laptops and tablets

$2,500 mobile notary equipment kit

Ramp cash

$1,049/month fixed overhead before payroll

$8,000 Year 1 marketing budget

$45 Year 1 customer acquisition cost

Fund payroll timing and state-rule delays

What are the biggest costs to start a mobile notary business?

The biggest startup costs for a Mobile Notary are the vehicle, state commissioning steps, bond and insurance, and the gear needed to print, scan, and book work. Using your figures, upfront spend is about $39,700 before monthly fixed costs of about $1,049 start. Year 1 cash burn is then hit by 120% vehicle and travel costs, 80% notary commission fees, 80% marketing, and 25% transaction fees, so this is a travel-first business, not a rent-heavy one.

Upfront setup costs

$25,000 vehicle purchase and setup

$4,500 website development

$3,200 laptops and tablets

$2,500 mobile notary equipment kit

Monthly cost pressure

$1,800 document scanner and printer

$1,500 training and certification

$1,200 initial marketing materials

$150 E&O insurance, plus $200 commercial auto insurance

Recurring monthly items

$75 business license and bonding

$85 phone service

$49 scheduling software

$65 website hosting

Year 1 variable pressure

120% vehicle and travel expenses

80% notary commission fees

80% marketing and advertising

25% transaction processing fees

How much funding do I need for a mobile notary business?

If you’re starting a Mobile Notary business, plan on more than equipment: the modeled need starts at $46,000 for setup, then adds runway for $1,049 in monthly fixed overhead before payroll, a $45,000 owner salary, contract notary cost starting in Month 7, $8,000 in Year 1 marketing, and variable costs tied to revenue. The model stays under pressure early, with EBITDA at negative $34,000 in Year 1, negative $25,000 in Year 2, and negative $6,000 in Year 3, then turns positive at $47,000 in Year 4 and $184,000 in Year 5. Breakeven lands in Month 34, so the next step is to validate state fees, service-area mileage, close rate, pricing, customer acquisition cost, and booking ramp in a mobile notary financial model before you commit cash.

Startup cash

$46,000 modeled setup budget

$1,049 monthly fixed overhead

$45,000 owner salary

Contract notary cost starts Month 7

Timing and risk

Year 1 EBITDA: negative $34,000

Year 2 EBITDA: negative $25,000

Year 3 EBITDA: negative $6,000

Breakeven and payback: Month 34

Calculate Fuding Needs

Startup cost summary

This table shows the main startup cost buckets for a mobile notary, plus the separate working capital reserve before payroll.

Highlighted CAPEX$46,000Base planning example

Excluded cash needs$696,000Outside CAPEX total

Funding need$742,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Vehicle purchase and readiness

$25,000

Existing vehicle versus purchased vehicle and travel prep

Yes

Mobile office equipment and document handling

$7,500

Kit, tablet, laptop, and scanner/printer readiness

Yes

Website and launch marketing

$7,700

Site build, branding, and heavier launch marketing

Yes

Training and signing-agent setup

$1,500

Training, certification, and loan-signing readiness

Yes

Office setup and supplies

$4,300

Furniture, supplies, and workspace setup

Yes

Working capital reserve

$696,000

Fixed overhead before payroll, travel, ads, and owner draw runway

No

Mobile Notary Core Five Startup Costs

Commission, Training, and Authorization Startup Expense

Commission cost

Budget the state fee stack first: application fee, required education, exam fee, background check, fingerprinting where required, oath, county recording, and the notary certificate. Add the model $1,500 for professional training and certification in Month 1 to Month 2. Rules vary by state, so confirm the secretary of state or commissioning office before you set the budget.

Budget inputs

Here’s the quick math: state commission fees + $1,500 training = launch authorization cost. For planning, treat notary commission fees as an operating cost at 80% of revenue in Year 1, stepping down to 60% by Year 5. That works only if your state rules, renewal cycle, and required screening match the model.

Check state-specific fee rules

Confirm renewal timing

Separate one-time from recurring costs

Cost control

Keep the cost lean by buying only what your state requires, then add extra training only if you plan loan signing work, after-hours services, or remote online notarization. Those services can trigger more screening, training, or tech rules. Don’t guess here; a missed state step can delay commissioning and push launch back.

Pay for required items first

Avoid optional extras too early

Verify service-specific requirements

State check

Before you book training, ask your state office which items apply: education, exam, background check, fingerprinting, oath, and any county recording or certificate fee. Some states add extra steps, and those fees can change the startup total fast. One clean rule: verify first, then budget.

Bond, Errors and Omissions, and Insurance Startup Expense

Bond Rules

Bond rules vary by state. A surety bond protects the public, not the notary, if a filing or witnessing error causes loss. For professional mistake coverage, budget $150/month for errors and omissions insurance and $75/month for business license and bonding.

Monthly Cost

Here’s the quick math: $150/month E&O, $75/month business license and bonding, and $200/month commercial auto insurance total $425/month. Add $300/month for accounting and legal services and you’re at $725/month before taxes and payment fees.

Legal Help

Use the $300/month legal and accounting line for contracts, entity paperwork, bookkeeping, and compliance. It keeps the setup clean when you work with lenders, law firms, or healthcare clients. If you skip it, tracking receipts and filings gets messy fast.

Rate Drivers

Refine the quote by state bond amount, E&O coverage limit, claim history, vehicle use, loan-signing exposure, and whether you use contract notaries. More driving, more paperwork, and more outside work usually raise the bill; a local-only setup can stay leaner.

Supplies and Mobile Office Equipment Startup Expense

Core supplies

The notary seal, stamp, journal, certificates, pens, folders, secure bag, and document tools are small supplies, so treat them as operating inventory. Use $800 for initial supplies and keep them separate from durable gear. Here’s the quick check: count units, replacement cycles, and any state-required forms before you buy.

Equipment kit

The durable mobile office set includes the $2,500 notary kit, $3,200 laptops and tablets, and $1,800 for the scanner and printer. That is capital expense, or CAPEX, because these items last more than one job. Loan signings can need higher print volume, scan backs, and dual-tray printing; basic general-notary work usually runs lighter.

Keep it lean

Spend on the setup that matches your work mix, not the nicest version on the shelf. If you do fewer prints and no scan backs, you may not need heavy-duty gear on day one. One-liner: buy for the appointment type you will actually serve, then upgrade after volume proves out.

Right-size the setup

Ask how many appointments per day, whether you print documents, whether scan backs are expected, and whether the work is mostly local mobile service or loan signings. Those answers drive paper use, printer duty, battery needs, and storage. If loan signings are core, size for higher volume and faster turnaround.

Vehicle and Travel Readiness Startup Expense

Vehicle Readiness

If you already have a car, don’t model it like a free asset. Budget for fuel, mileage, parking, tolls, a maintenance buffer, roadside kit, and mobile storage. If you need a buy or upgrade, use the $25,000 source figure across Month 1 to Month 2.

Cost Load

Here’s the quick math: vehicle and travel expenses are modeled at 120% of revenue in Year 1, then 90% by Year 5. Add $200 per month for commercial auto insurance. The mix matters because Year 1 assumes 300% mobile services, 150% loan signings, and 100% after-hours services.

Route Pricing

Price travel by real route cost, not guesswork. Radius, traffic, parking, tolls, cancellation rules, appointment density, and whether travel fees are already in the quote all change the number. One clean rule: sparse routes burn cash faster. Dense service areas and tighter scheduling spread the same car cost over more billable stops.

Own Car vs Buy

Separate an existing personal vehicle from a purchase or upgrade. If the car is already dependable, carry only operating travel costs; if not, the $25,000 setup belongs in startup cash. That split keeps the budget honest and stops founders from hiding one-time vehicle spend inside monthly overhead.

Marketing, Booking, and Customer Acquisition Startup Expense

Launch setup

For a mobile notary, launch spend is the one-time setup that gets calls, bookings, and payments working. Model $4,500 for website development, $1,200 for initial marketing materials, and $2,000 for signage and branding. That sits apart from monthly tools, so you can see what it takes to open vs. what it costs to keep leads coming.

Monthly tools

Run-rate costs cover the website, booking, and phone stack: $65 for hosting and maintenance, $49 for scheduling software, and $85 for phone service. Add local search setup, directory profiles, business cards, and payment processing setup. One clean rule: build these as fixed monthly costs, then compare them to booked jobs and after-hours coverage.

Lead cost

Use the Year 1 marketing budget of $8,000 to cover launch ads, referral outreach to attorneys and real estate professionals, and reputation-building. The model also uses $45 customer acquisition cost, so here’s the quick math: budget ÷ expected new customers should land near that number. If booking conversion is weak, CAC rises fast.

Fee pressure

Keep the model honest with 80% marketing and advertising as a share of revenue and 25% transaction processing fees in Year 1. Those are heavy drags, so the mix matters: more attorney and real estate referrals, more after-hours jobs, and better local search can lower paid ad dependence. If local competition is strong, expect higher spend per booked appointment.

Compare 3 Startup Cost Scenarios

Scenario Table

Startup cost changes fast based on vehicle ownership and how much mobile, loan-signing, and remote work you add. These scenarios show the gap from a lean side launch to a growth-ready setup.

Lean, Base, and Full launch cost comparison for a mobile notary business

Scenario

Lean LaunchSide-launch fit

Base LaunchLocal operator

Full LaunchGrowth-ready

Launch model

Uses an existing vehicle, light gear, a basic website, and local listings to start as a side launch.

Uses the researched $46,000 startup plan with the core vehicle, tools, site, and launch buildout.

Adds loan-signing gear, higher insurance, broader marketing, contract notary capacity from Month 7, and remote online notarization tools where allowed.

Typical setup

Existing vehicle, light equipment, a basic website, local listings, and low-cost marketing materials.

Vehicle purchase, notary kit, laptop and tablets, scanner and printer, website build, training, marketing materials, and supplies.

Base setup plus stronger loan-signing gear, higher insurance, broader marketing, contractor capacity, and remote online notarization costs where allowed.

Cost drivers

Existing vehicle

basic website

light equipment

local listings

low launch materials

Vehicle purchase

notary kit

laptop and scanner

website build

training and launch materials

Loan-signing gear

higher insurance

broader marketing

contractor capacity

remote online notarization tools

Planning rangeCAPEX only

$21,000 - $25,000Lowest cash need

$46,000Model-backed base

$60,000+Higher capital build

Best fit

Best for a side launch or owner-operator who already has a reliable vehicle.

Best for a full-time local operator who wants the model-backed launch plan.

Best for a growth-ready signing service planning more volume and more service lines.

!

Planning note: These ranges are researched planning assumptions, not vendor quotes; actual funding need shifts with state rules, vehicle ownership, equipment choices, and early marketing intensity.

The modeled mobile notary launch costs $46,000 before working capital and payroll runway The largest item is a $25,000 vehicle purchase and setup Other key setup costs include $4,500 for website development, $3,200 for laptops and tablets, $2,500 for a mobile equipment kit, and $1,800 for document scanning and printing

In this researched model, the mobile notary reaches breakeven in Month 34, with a 34-month payback period EBITDA is negative $34,000 in Year 1, negative $25,000 in Year 2, and negative $6,000 in Year 3 That means working capital matters as much as the opening budget

Yes, plan for insurance and bonding because this business handles legal documents and client travel The model includes $150 per month for errors and omissions insurance, $75 per month for business license and bonding, and $200 per month for commercial auto insurance State bond rules vary, so verify your local requirement

Start with the required notary seal and journal, then add a phone, secure document bag, laptop or tablet, printer, scanner, and basic supplies The model budgets $2,500 for a mobile notary equipment kit, $3,200 for laptops and tablets, $1,800 for a scanner and printer, and $800 for initial supplies

Use an existing reliable vehicle if it fits the service area, because the modeled vehicle purchase and setup is $25,000 Keep the first launch tight with essential supplies, booking tools, and local referral outreach Still budget for $8,000 in Year 1 marketing, a $45 customer acquisition cost, and $1,049 monthly fixed overhead before payroll

About the author

Simon Reed

Small Business Educator

Simon Reed is a small business educator at Financial Models Lab who helps service business founders understand the numbers behind everyday business ideas. He focuses on pricing and margin basics, common business costs, and the first months after launch, giving readers a clearer view of what it takes to build a healthy business. Simon brings a simple, confident approach that balances optimism with cost-aware planning.

Choosing a selection results in a full page refresh.