Mortgage Bank Startup Costs For A $50M First-Year Loan Plan

Mortgage Bank Bundle

This mortgage bank startup budget covers pre-opening setup, CAPEX, and operating runway for a launch model that targets $500 million in first-year loan volume It separates office and technology setup from the larger funding stack: $300 million in warehouse line credit, $50 million in subordinated debt, and $50 million in Federal Home Loan Bank advances The outcome is a planning view of cash needed before revenue stabilizes, not a legal capital quote

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets for a mortgage bank, not day-to-day funding needs.

!

Non-CAPEX Exclusions Excludes working capital, payroll runway, deposits, debt service, warehouse line collateral, loan funding, inventory, marketing runway, regulatory reserves, and other operating expenses.

What do mortgage bank licensing and compliance costs include?

Mortgage Bank licensing and compliance costs usually cover NMLS setup, state mortgage lender applications, entity formation, legal review, compliance manuals, policies, background checks, audits, surety bonds, and regulatory prep. Using the cost anchors provided, recurring spend is about $5,500/month from $2,500 compliance and legal fees, $1,000 insurance, and $2,000 professional services, before filing and bond costs. State rules vary on net worth, qualified individual requirements, and surety bond amounts, so validate state-specific requirements before you commit spend.

Core startup costs

NMLS registration and filings

State lender applications

Entity formation and setup

Legal review and document prep

Ongoing compliance spend

$2,500 monthly compliance and legal fees

$1,000 monthly insurance

$2,000 monthly professional services

Background checks, audits, surety bonds

How much money do you need to start a mortgage bank?

To start a Mortgage Bank, separate launch cash from funding capacity: listed operating readiness includes $565,000 in base payroll plus $19,200/month in fixed overhead, while the broader funding stack includes $400 million from credit, debt, and advances. For the KPI behind that capital plan, see What Is The Main Success Indicator For Your Mortgage Bank?; the base model targets $500 million in Year 1 loan volume.

Opening cost

$565,000 listed base payroll

$19,200 monthly fixed overhead

Costs move with staff count

State footprint affects reserves

Capital base

$300 million warehouse line credit

$50 million subordinated debt

$50 million Federal Home Loan Bank advances

$500 million Year 1 loan volume target

What hidden costs of starting a mortgage bank should founders budget for?

If you're budgeting a Mortgage Bank, the real cash drain is not office furniture; it's payroll runway, compliance, delayed loan-sale cash, and borrower acquisition. For a quick anchor, see How Much Does The Owner Of Mortgage Bank Typically Make? and then budget around $19,200 monthly fixed overhead, $565,000 listed launch payroll, plus 13% Year 1 loan origination commissions and 50% Year 1 marketing and customer acquisition. Those hidden operating needs can move total funding far more than signage or desks.

Cash you must fund

$19,200 monthly fixed overhead

$565,000 listed launch payroll

13% Year 1 origination commissions

50% Year 1 marketing and acquisition

Hidden cost buckets

Payroll runway before loan revenue lands

Compliance monitoring and renewals

Loan-sale timing and warehouse deposits

Repurchase, due diligence, and tech overruns

Calculate Fuding Needs

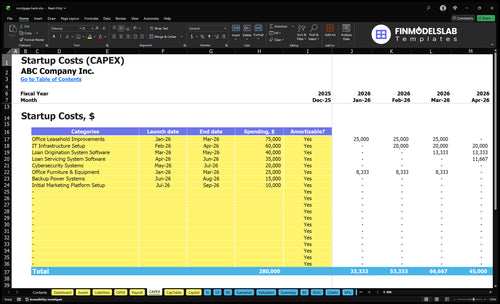

Startup Cost Summary

This table summarizes startup CAPEX and the separate cash reserve needed before launch for a mortgage bank.

Buildout for lending operations and compliance space

Yes

IT Infrastructure Setup

$60,000

Core network, hardware, and secure systems setup

Yes

Loan Origination System Software

$40,000

Loan origination platform implementation

Yes

Loan Servicing System Software

$35,000

Servicing system setup and integration

Yes

Cybersecurity Systems

$20,000

Security controls for borrower data and funds flow

Yes

Liquidity Reserve

$18,719,000

Warehouse funding, payroll, and regulatory capital runway

No

Mortgage Bank Core Five Startup Costs

Licensing And Compliance Startup Expense

License Scope

For a mortgage lender, licensing is not one fixed fee. Budget $4,500/month for compliance and legal work based on $2,500 plus $2,000, then add state filing costs, background checks, and approval work by jurisdiction. Ask which states launch first, whether commercial lending is in scope, and whether servicing stays in-house.

What It Covers

This expense covers entity setup, NMLS registration (Nationwide Multistate Licensing System), state applications, lender approvals, compliance manuals, written policies, legal review, background checks, qualified individual setup, audits, recordkeeping, and regulator-ready procedures. The quick math is simple: monthly operating cost plus outside filing and counsel work, which varies by state and license type.

Set up entity and registrations first

Map each state separately

Document policies before launch

How To Control Cost

Keep the launch state list tight, reuse one policy set where allowed, and avoid paying for commercial scope unless you truly need it. Since licensing is jurisdiction-specific, fee amounts are not universal. The main mistake is undercounting legal review and recordkeeping setup, which can trigger rework and delay approvals.

Start with fewer states

Keep servicing scope clear

Use one document system

Regulator-Ready Setup

Build for exams from day one: written procedures, audit trails, file retention, complaint logs, and approval records should be ready before first funding. If onboarding or background checks slow down, fix that early, because weak process control can block lender approvals and delay the first closed loan.

Capital And Liquidity Readiness Startup Expense

Capital Stack

This is not a normal startup expense. It is the money you must hold for net worth, liquidity reserves, warehouse deposits, and funding needs before loans are sold, so it sits beside launch costs, not inside them.

Liquidity Need

The funding stack shown is $300 million warehouse line credit, $50 million subordinated debt, and $50 million Federal Home Loan Bank advances in Year 1. With $500 million of Year 1 loan volume, warehouse capacity is the core operating constraint, and reserve needs depend on approvals, investor terms, and state rules.

Due Diligence

Budget for credit facility due diligence, collateral setup, and the cash needed before loans are sold. The key inputs are lender minimums, warehouse haircuts, sale timing, and required deposits. If loan sale timing slips, cash gets trapped longer, so this reserve is a balance sheet buffer, not an operating expense.

Approval Limits

Do not set this number alone. Investor agreements, lender approvals, and state requirements decide how much capital, collateral, and liquidity you must keep on hand, and those rules can change the real startup cash need fast.

Technology Systems Startup Expense

Core systems

This budget covers the loan origination system, borrower portal, CRM, pricing engine, document management, e-signature, cybersecurity, compliance tracking, reporting, and integrations. Use $3,000 per month as the recurring anchor for software licenses and IT support, then add one-time implementation separately. The key is setup, security, and audit-ready workflow, not feature shopping.

Estimate inputs

Start with three inputs: Month 1 users, whether commercial mortgages are in scope, and whether servicing needs extra systems. One-time setup is separate from monthly spend, so price both. If you launch with a small team, the monthly run rate can stay near the $3,000 anchor before added modules or user seats push it up.

Keep it lean

Trim cost by launching only the workflows you need on day one, then adding reporting, integrations, or servicing tools later if volume justifies it. Don’t underbuy security or compliance tracking, because loan files and borrower data need clean records from the start. One clean rule: build for the first closing, not the full-year wish list.

Scope check

Before you lock the budget, confirm whether the launch includes commercial mortgages and whether servicing runs on the same stack. Those two choices can change user counts, controls, and implementation work fast. If the team expects month-one volume growth, plan for tighter permissions, stronger audit trails, and extra integration testing from day one.

Staffing Readiness Startup Expense

Base Payroll

Launch staffing is a monthly burn item, not a one-time fee. The base team is CEO or Head of Lending at $180,000, CFO at $150,000, Senior Loan Underwriter at $100,000, Loan Advisor at $75,000, and Loan Processor or Servicing Specialist at $60,000. That is $565,000 in Year 1 base payroll, or about $47.1k a month before benefits, taxes, bonuses, commissions, and contractors.

What It Covers

Use this line item for recruiting, screening, offers, onboarding, and training. The key inputs are headcount, base pay, hiring timing, and ramp speed. Year 1 commissions are modeled at 13% of loan origination volume if tied to production, so payroll planning has to match underwriting, processing, compliance, and loan sale capacity.

Recruiting and background checks

Training and onboarding time

Monthly payroll runway

Production-linked commissions

How To Control It

Keep fixed payroll lean until loan flow is proven. Start with the roles you need to approve, process, and sell loans, and do not add headcount faster than the pipeline. The main mistake is mixing one-time hiring costs with ongoing runway, which hides the real cash need.

Hire in stages

Let commissions flex first

Match staff to volume

Capacity Check

If underwriting, processing, compliance, and loan sale capacity do not scale together, the team becomes the bottleneck. That pushes service times up and makes the $565,000 base payroll harder to support, especially before commissions and contractor spend are added.

Office Insurance And Launch Infrastructure Startup Expense

Office Setup

Secure office space covers the lease deposit, furniture, signage, utilities, maintenance, business insurance, errors and omissions coverage, surety bonds, website setup, brand setup, and borrower launch spend. Price it with the lease quote, deposit terms, and setup invoices so you can see what is fixed and what is a one-time launch cost.

Fixed Run Rate

Here’s the quick math: $8,000 rent + $1,500 utilities and maintenance + $1,000 insurance + $1,200 general admin = $11,700 per month before launch spend. If Year 1 marketing and customer acquisition are modeled at 50%, keep that spend separate so overhead does not blur the real cost of getting borrowers.

Keep It Lean

Use a digital-first office plan, but do not underfund records, audits, or borrower data protection. Save money with smaller space, shared meeting rooms, and phased furniture buys; skip the impulse to cut security or storage. The best savings come from trimming square footage, not from weakening compliance-ready operations.

Launch Controls

Before you sign, price the deposit, first month’s rent, and any fit-out work. Then confirm that business insurance, errors and omissions, and surety bonds match lender and state rules. One clean test: if the office cannot protect files and audit trails, it is too cheap.

Compare 3 Startup Cost Scenarios

Scenario Table

Mortgage banking costs move fast as payroll, compliance, and warehouse credit scale with volume. Lean fits a tighter pilot, while Full assumes multi-state growth and much higher funding needs.

Lean, Base, and Full launch cost comparison.

Scenario

Lean LaunchSingle-state pilot

Base LaunchYear 1 model fit

Full LaunchMulti-state scale

Launch model

Start in one state with a smaller team, fewer loan products, and a lighter office setup.

Run the Year 1 plan with residential, commercial, refinance, and home equity lending.

Build for multi-state lending and product breadth, with Year 5 loan volume near $9.0 billion and warehouse credit near $4.8 billion.

Typical setup

Use core lending and servicing, then delay product expansion until volume proves out.

Keep one main office, the standard staff mix, $19,200 in monthly fixed overhead, and $565,000 listed payroll.

Add more underwriting, processing, compliance, and funding capacity early.

Cost drivers

Payroll

compliance

office footprint

software

Payroll

warehouse credit

compliance

marketing

servicing tech

Payroll

warehouse credit

compliance

multi-state ops

IT

Planning rangeCAPEX only

Low six figuresCapital-light

Mid six figuresModel case

High seven figuresScale risk

Best fit

Best for founders testing demand before they add more products or branch into new states.

Best for teams that want the researched operating plan and a clear path to breakeven.

Best for backed teams that can fund slower payback, heavier oversight, and rapid loan growth.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes, bids, or lender offers.

The model does not give one fixed opening quote It shows a $500 million Year 1 loan plan with $19,200 in monthly fixed overhead and $565,000 in listed first-year payroll The larger funding stack includes $300 million in warehouse credit, plus $50 million subordinated debt and $50 million Federal Home Loan Bank advances

The provided model does not state a licensing timeline, so don’t build a calendar promise from it Plan the launch period around Month 1 expense readiness, a 60-month operating model, and recurring compliance costs of $2,500 per month State approvals, background checks, surety bonds, and regulator review can change the opening schedule

In this researched mortgage bank model, yes Year 1 includes $300 million of warehouse line credit to support $500 million of loan volume before loans are sold or otherwise financed That is separate from office setup, software, licensing, and payroll If you start as a broker instead, the funding structure can look very different

A mortgage banker usually carries heavier capital and liquidity needs because it funds or closes loans using warehouse capacity This model includes $300 million in Year 1 warehouse credit and $400 million in residential mortgage volume alone A broker model may avoid that balance sheet load, but still needs licensing, compliance, staff, software, and marketing

Start by mapping loan volume to cash timing Use the model’s $500 million Year 1 loan volume, $19,200 monthly fixed overhead, $565,000 listed payroll, 13% loan origination commissions, and 50% marketing and customer acquisition assumption Then test whether warehouse capacity, payroll runway, and compliance spend hold up during the early ramp-up period

About the author

Jason Burke

Business Operations Writer

Jason Burke is a business operations writer at Financial Models Lab who researches how small businesses launch, operate, and earn money, with a focus on first-year business costs and the shift from side project to real business. He writes simple business projections and practical guidance that helps non-finance readers make business planning feel clearer, more useful, and easier to act on.

Choosing a selection results in a full page refresh.