Payment Processing Startup Costs With $350K Year 1 Marketing Plan

Payment Processing

Key Takeaways

Legal and compliance need $3,500 monthly before growth.

Platform build adds $3,000 monthly cloud plus fees.

Fraud controls cost 15% of Year 1 revenue.

Fixed overhead starts at $13,500 monthly in Month 1.

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets needed before launch; it excludes operating costs and other funding needs.

!

Excluded costs This calculator covers capitalized launch assets only. It excludes payroll runway, recurring marketing, working capital, deposits, debt service, inventory, chargebacks, transaction fees, cloud hosting at $3,000 per month, and other post-launch operating costs.

How much money do you need to start a payment processing company?

You need at least $842,000 for the first-year visible operating floor of a Payment Processing company, before quoted platform build, sponsor bank, acquirer, PCI DSS, fraud, legal, compliance, reserves, and working capital costs. Treat this as the opening-cost budget, not the full funding need; payment volume matters early, so track How Is The Growth Of Payment Processing Volume Impacting The Success Of Your Business? alongside CAC and onboarding cost.

Opening Budget

Use $842,000 as the Year 1 floor

Budget $350,000 for acquisition marketing

Include $162,000 fixed overhead

Set $330,000 for leadership payroll

CAC Math

Spend $250,000 on seller marketing

At $500 CAC, onboard 500 sellers

Spend $100,000 on buyer marketing

At $10 CAC, acquire 10,000 buyers

Why is starting a payment processing company expensive?

Payment Processing is expensive because every dollar moves through a regulated flow that needs PCI DSS compliance, legal setup, underwriting controls, fraud checks, and banking access. Here’s the quick math: just the known readiness costs are $1,500/month for security and compliance software, $2,000/month for legal and accounting, and $3,000/month for cloud infrastructure, before you layer in 70% gateway fees and 15% fraud software licenses in Year 1. So the founder is not really buying software; they’re funding risk control, partner due diligence, and technical integrations from day one.

Big cost drivers

PCI DSS compliance is required

Underwriting blocks bad merchants

Fraud monitoring runs nonstop

Banking access needs due diligence

Known readiness costs

$1,500/month security software

$2,000/month legal and accounting

$3,000/month cloud infrastructure

70% gateway fees, 15% fraud licenses

What hidden costs of starting a payment processing business matter most?

The biggest hidden costs in Payment Processing are working capital tied up in reserves, chargeback exposure, compliance audits, and legal review cycles. If you want the owner-side cash picture, read How Much Does The Owner Of Payment Processing Business Typically Make? because reserves are a funding need, not CAPEX, and they can drain cash fast. Year 1 can also carry $500/month for insurance, $2,000 for legal and accounting, $1,500 for security and compliance software, plus 85% combined COGS from gateway and fraud tools against $13,500 in monthly fixed overhead.

Cash traps

Rolling reserves trap cash.

Chargebacks and fraud hit fast.

Residual income can arrive late.

Partner onboarding can delay payouts.

Fixed monthly drag

$500 for business insurance.

$2,000 for legal and accounting.

$1,500 for compliance software.

Reserve needs are model-dependent.

Calculate Fuding Needs

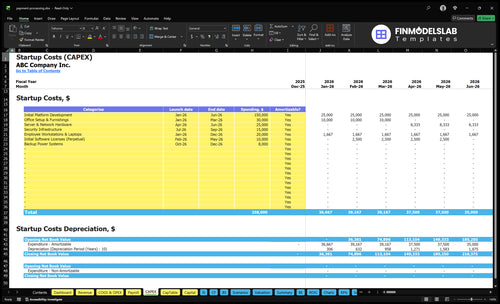

Startup cost summary

This table covers startup assets plus the non-CAPEX cash needed to open a payment processing business.

Highlighted CAPEX$240,000Base planning example

Excluded cash needs$1,103,000Outside CAPEX total

Funding need$1,343,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Initial Platform Development

$150,000

Development scope and build time

Yes

Office Setup & Furnishings

$30,000

Fit-out scope and furniture count

Yes

Server & Network Hardware

$25,000

Hardware capacity and redundancy

Yes

Security Infrastructure

$15,000

Security controls and fraud testing

Yes

Employee Workstations & Laptops

$20,000

Launch team device count

Yes

Operating Reserve

$1,103,000

Month 30 cash trough and fixed overhead

No

Payment Processing Core Five Startup Costs

Compliance and Legal Setup Startup Expense

Legal setup

This cost covers entity formation, legal counsel, merchant agreements, privacy and security documents, risk policies, underwriting procedures, contract review, PCI DSS readiness, regulatory review, and partner compliance packs. The budget depends on how many states you touch, your payment flow, and whether you use a sponsor or acquirer structure. One filing does not cover every model.

What to budget

Plan for $2,000 per month for legal and accounting, plus $1,500 per month for security and compliance software. Here’s the quick math: multiply monthly spend by runway months, then add outside counsel and filing work based on your state footprint and processor setup. That gives a cleaner startup reserve.

$2,000 legal and accounting

$1,500 security software

Months of coverage

How to keep it tight

Use standard templates for merchant terms, privacy, and risk policies, and review them before launch. Don’t assume one license or one filing covers every payment model. If the state footprint is small and the payment flow is simple, counsel time can stay lower; if not, expect more review and more compliance work.

Partner readiness

Budget this work early because sponsor and acquirer reviews can slow revenue. The real cost is not just setup fees; it is the months of legal, accounting, software, and partner diligence needed before processing starts. Requirements change with processor role, state footprint, payment flow, and sponsor or acquirer structure.

Technology Platform and Payment Infrastructure Startup Expense

Build Scope

The platform build covers the payment gateway, APIs, merchant portal, transaction routing, reconciliation, reporting, tokenization, uptime monitoring, and integrations. Keep capitalized build separate from $3,000 per month cloud hosting and 70% Year 1 third-party gateway fees, or the startup budget will hide the real cost of getting live.

Cost Inputs

Here’s the quick math: estimate developer hours, API licenses, certification scope, and testing time, then add hosting months and processor fees. The biggest inputs are build versus outsource, required uptime, reporting depth, and merchant onboarding workflow. What this estimate hides: partner testing and compliance review can stretch the timeline.

Control Spend

Cut cost by building only the first release you need, not every feature at once. Start with core payment flow, reconciliation, and basic reporting, then phase richer analytics later. Ask what uptime is truly required, which integrations are mandatory, and which certifications are needed now. One clean rule: don’t pay for scale before you have volume.

Budget Check

The budget needs a clean split between one-time platform build and recurring run cost. If Year 1 gateway fees stay at 70% of revenue, then payment infrastructure economics depend more on transaction volume and fee structure than on the hosting line. That makes merchant onboarding speed and routing quality central to cash planning.

Security, Fraud Prevention, and Risk Management Startup Expense

Readiness Controls

If you process payments, fraud controls are not optional overhead. Budget for fraud scoring, Know Your Customer (KYC), Know Your Business (KYB), merchant underwriting, chargeback workflows, transaction monitoring, access controls, alerting, penetration testing, and PCI DSS readiness. In Year 1, plan 15% of revenue for fraud prevention software licenses plus $1,500 per month for security and compliance software.

Budget Inputs

Estimate this line with three inputs: months of coverage, vendor quotes, and expected payment volume. The core spend is $1,500 per month for security and compliance software, plus 15% of Year 1 revenue for fraud prevention licenses. Add tools for merchant underwriting, transaction alerts, and chargeback handling so the budget covers live operations, not just launch paperwork.

Lean Setup

Cut waste by staging tools in order: start with KYC, KYB, scoring, and alerts, then add deeper analytics after volume rises. Avoid duplicate monitors or custom rules too early. Keep access controls tight and review alert thresholds often. Real savings come from fewer false positives and less manual review, not from skipping controls.

Why It Comes First

Treat this spend as a readiness gate, not a nice-to-have. If fraud losses start before revenue catches up, the launch budget needs room for security software, testing, and monitoring from day one. A lean team still has to fund compliance-grade controls, because payment risk hits fast and recovery is slower.

Sponsor Bank, Acquirer, and Certification Startup Expense

Bank Partner Setup

This cost covers sponsor bank diligence, acquirer integration, processor connectivity, network testing, technical certification, compliance reviews, implementation fees, and partner onboarding. There is no single fee or approval path; the spend depends on merchant categories, payment flow, and how many systems need to be certified before live processing starts.

Cost Build

Estimate this line from quotes, integration scope, test cycles, and onboarding months. Here’s the quick math: fixed overhead starts in Month 1 at $13,500 per month, and partner onboarding may delay processing revenue, so the budget needs enough working capital to cover the gap before the first settlement lands.

Reduce Rework

Cut waste by locking the payment flow early, giving clean merchant data up front, and limiting late changes that force retesting. Don’t chase the cheapest partner if it weakens controls. Faster onboarding usually comes from tighter due diligence packets and fewer technical edits, not from skipping certification.

Cash Timing Risk

The main risk is timing, not just price. If onboarding slips, you still carry $13,500 per month of fixed overhead before payment revenue starts. That makes working capital part of the startup budget, so founders should fund the integration bill and the delay between setup and live processing.

Staffing, Professional Services, and Launch Marketing Startup Expense

Setup

This bucket is mostly one-time setup before go-live: compliance consultants, merchant agreements, PCI DSS readiness, developers, risk staff, support playbooks, sales materials, website, CRM, merchant onboarding assets, and launch campaigns. Estimate it from headcount quotes, months of coverage, and vendor bids. The core recurring anchors are $180,000 CEO pay, $150,000 Head of Product & Tech pay, and $700 per month for CRM and project tools.

Control

Cut spend by using short-burst consultants for legal, security, and compliance, then lock one owner on risk policy and underwriting procedures. Don't overbuild the website or merchant portal before you have a tested onboarding flow. Year 1 seller marketing of $250,000 and buyer marketing of $100,000 should be staged by channel, not spent all on day one.

Payroll

Recurring staff cost matters more than the launch checklist. At $180,000 plus $150,000, base leadership payroll is $330,000 a year, or about $27,500 per month before benefits and other hires. Add customer support, sales commissions, and risk coverage as volume grows, because payment failures and disputes usually hit right after onboarding.

Launch

Year 1 acquisition spend totals $350,000 across sellers and buyers, so this line needs clear targets: merchant sign-ups, funded accounts, and first transactions. Use the CRM to track source, conversion, and payback by channel. If onboarding is slow, protect seller spend first, since weak supply makes buyer marketing less useful.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Lean, Base, and Full launch paths change how much of the stack you own, and that shifts compliance load, staffing, reserve needs, and first-year cash burn.

Lean vs Base vs Full payment processing launch costs

Scenario

Lean LaunchLowest ownership

Base LaunchModerate integration ownership

Full LaunchHighest compliance and risk ownership

Launch model

Use a referral or ISO-style model and route processing through a sponsor or acquirer.

Run a technology-enabled merchant services model with your own onboarding and support, but keep core processing tied to partners.

Run a full PayFac-style model with more platform ownership, settlement control, and direct compliance responsibility.

Typical setup

Keep the platform light, with minimal custom build and narrow compliance scope.

Build standard integrations, use partner rails, and carry moderate compliance and ops work.

Build deeper payment infrastructure, expand controls, and keep higher reserves for risk and chargebacks.

Cost drivers

Sponsor dependence

lighter tech build

lower compliance work

smaller reserves

lean staffing

Acquisition marketing

fixed overhead

leadership payroll

compliance software

support hiring

Platform build

compliance burden

reserve funding

security controls

senior staffing

Planning rangeCAPEX only

$400,000 - $900,000Lower band

$900,000 - $1,600,000Mid band

$1,800,000 - $3,500,000Highest band

Best fit

Fits founders who want the lightest setup and can trade control for speed.

Fits teams that want control of the customer flow without taking full regulatory and settlement risk.

Fits capitalized teams that need direct control, large volume, and can absorb slower payback.

!

Planning note: These scenario ranges are researched planning assumptions, not exact vendor quotes.

The researched first-year funding floor is about $842,000 before platform CAPEX, compliance buildout, reserves, and incomplete staffing costs That floor includes $350,000 in acquisition marketing, $162,000 in fixed overhead, and $330,000 for the CEO and Head of Product & Tech Treat this as a planning base, not a vendor quote

Usually, some bank or acquiring relationship is needed if the business touches merchant acquiring, settlement, or card processing flow The cost is not just the fee it includes due diligence, compliance review, technical integration, and risk controls The model already carries $2,000 per month for legal and accounting and $1,500 per month for security and compliance software

Plan for an early ramp-up period where costs start before revenue is stable Fixed overhead begins in Month 1 at $13,500 per month, while Year 1 marketing totals $350,000 and visible leadership payroll totals $330,000 If partner onboarding, PCI DSS readiness, or certification takes longer than expected, working capital needs rise fast

Compliance work, legal setup, platform build, security tools, partner onboarding, website, CRM, sales materials, and launch marketing often come first In this plan, seller acquisition uses $250,000 in Year 1 at $500 CAC, while buyer acquisition uses $100,000 at $10 CAC Cloud hosting adds $3,000 per month from Month 1

Reduce funding risk by separating must-have launch costs from scale costs Start with quoted CAPEX, then add $13,500 monthly fixed overhead, $350,000 Year 1 marketing, visible payroll of $330,000, and reserve assumptions Also test CAC sensitivity because the plan depends on $500 seller CAC and $10 buyer CAC in Year 1

About the author

Jonathan Bell

First-Time Founder Guide Writer

Jonathan Bell is a Financial Models Lab writer focused on launch budget planning, helping aspiring small business owners estimate startup needs before opening. As a first-time founder guide writer, he explains business costs in simple language and offers simple launch planning insights that help readers compare business opportunities realistically and make grounded real-world decisions.

Choosing a selection results in a full page refresh.