You’re budgeting a peer-to-peer (P2P) lending launch, so the first year needs to cover platform build, compliance, licensing, underwriting, payments, staff readiness, launch marketing, pre-opening expenses, working capital, and any separate liquidity plan The provided model shows $350,000 in first-year acquisition spend, $16,000 in monthly fixed overhead, and $120,000 in founder salary before unpriced CAPEX, legal setup, licensing, or loan-funding reserves These are researched planning assumptions, not vendor quotes, legal advice, or guaranteed launch costs

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a peer-to-peer lending platform.

!

CAPEX scope note This calculator includes only capitalized software and implementation spend. It excludes payroll runway, inventory, deposits, debt service, working capital, customer acquisition, legal retainers, licensing fees, and loan funding unless your accounting policy clearly allows capitalization.

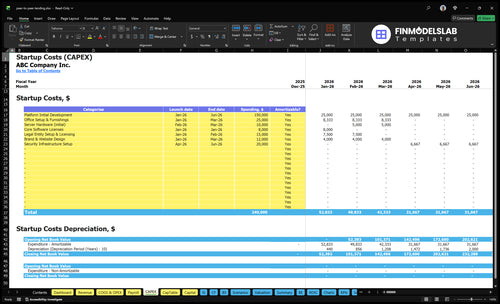

What does the CAPEX tab show?

The screenshot shows the Peer-to-Peer Lending Financial Model TemplateCAPEX tab. It shows startup costs, launch timing, and depreciation or amortization; open it and review $350,000 acquisition spend, $16,000 overhead, and fee assumptions.

Financial model screenshot highlights

CAPEX and startup spend

Pre-opening and working capital

1-year and 5-year periods

$350k acquisition spend

$16k monthly overhead

$120k founder salary

30% variable commission

Fixed $50 commission

40% fees, 30% data

Peer-to-Peer Lending Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

How much money do you need to start a peer-to-peer lending platform?

You need at least $662,000 in first-year operating funding to start Peer-to-Peer Lending before unpriced platform build, licensing, and legal setup; use What Strategies Are You Using To Grow Peer-To-Peer Lending Platform? once acquisition spend starts. Here’s the quick math: $350,000 launch acquisition + $192,000 fixed overhead + $120,000 founder salary.

Base Funding

Fund lenders: $150,000

Fund borrowers: $200,000

Cover overhead: $192,000

Pay founder: $120,000

Main Drivers

Revenue: 30% variable commission

Add $50 fixed commission per loan

Costs vary by licensing, states, team

Not vendor quotes or legal advice

What are the biggest cost drivers for a peer-to-peer lending startup?

Peer-to-Peer Lending is cost-heavy because it needs fintech-grade controls, not a simple website. The biggest drivers are 40% loan servicing and transaction fees, 30% data verification and credit scoring, plus fixed run-rate costs like $5,000 a month for cloud and SaaS, $3,000 for maintenance and security, and $2,500 for legal and compliance. Every new state, loan type, or investor segment adds review work for lending rules, securities checks, bank partnership review, KYC/AML, fraud controls, and audit readiness.

Core cost drivers

40% loan servicing and transaction fees

30% data verification and credit scoring

$5,000 monthly cloud and SaaS

$3,000 monthly maintenance and security

Compliance load

$2,500 legal and compliance retainer

State-by-state lending and broker review

Consumer credit, securities, and bank checks

KYC/AML, fraud, cybersecurity, audit work

What hidden costs of peer-to-peer lending startups should founders plan for?

Hidden costs in Peer-to-Peer Lending sit in operations and working capital, not CAPEX, so founders should budget for compliance, support, and loan servicing from day one. For owner-pay context, see How Much Does The Owner Of Peer-To-Peer Lending Platform Typically Make?. With $16,000 monthly fixed overhead, plus $1,000 insurance, $1,000 accounting and audit fees, and $1,500 general admin, cash burn can start before revenue scales if onboarding or compliance reviews run long.

Operating costs

30% customer support load

50% marketing and affiliates

$1,000 insurance monthly

$1,000 accounting and audit fees

Working capital risks

Legal revisions and compliance checks

State license renewals and audits

Dispute handling and repayment exceptions

Cloud spikes, fraud tools, payroll runway

Calculate Fuding Needs

Startup cost summary table

This table shows startup CAPEX and the excluded operating reserve needed to launch and support early platform operations.

Highlighted CAPEX$218,000Base planning example

Excluded cash needs$299,000Outside CAPEX total

Funding need$517,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Platform Initial Development

$150,000

Build the loan marketplace and admin tools

Yes

Security Infrastructure Setup

$20,000

Cybersecurity and secure platform setup

Yes

Legal Entity Setup & Licensing

$15,000

Formation, licensing, and compliance setup

Yes

Office Setup & Furnishings

$25,000

Launch workspace and furnishing needs

Yes

Core Software Licenses

$8,000

Initial software tools and subscriptions

Yes

Operating Reserve

$299,000

Cash runway for fixed overhead and launch period

No

Peer-to-Peer Lending Core Five Startup Costs

Platform Technology And Software Build Startup Expense

Core Build Scope

Treat the platform build as the largest CAPEX line. It should cover borrower applications, lender dashboards, loan matching, underwriting workflows, document upload, e-signature, admin panels, reporting, permissions, security, and cloud architecture. That scope is product work, not a simple website, because repayment tracking and compliance evidence are core functions.

Estimate Inputs

Build the budget from hours × rate or a vendor quote, then add implementation fees, data connections, payment connections, testing, and contingency. Keep one-time build cost separate from monthly run rate. That gives you a cleaner startup model and stops software spend from hiding inside general launch costs.

Build hours or vendor quote

Implementation and testing fees

Data and payment connections

Month 1 Run Rate

Operating tech costs start in Month 1 at $5,000 for technology infrastructure and $3,000 for platform maintenance and security. Budget both from day one, because loan matching, repayment tracking, and compliance evidence are live system needs, not post-launch extras.

Avoid Website Framing

Don’t frame this like a marketing site. The hard costs are underwriting workflow, security, and audit-ready records, so scope control matters more than design polish. If the build misses permissions, cloud controls, or evidence capture, you’ll pay for rework later.

Regulatory, Legal, And Licensing Startup Expense

Core legal scope

Start with entity formation, lending law review, state lending or broker rules, securities checks, bank-partnership review, consumer credit disclosures, privacy and servicing policies, complaint handling, and compliance training. A qualified US fintech counsel should map the path before launch. One line to remember: the legal cost follows the regulatory path, not just one license.

Budget inputs

Plan for $2,500 per month for legal and compliance from Month 1, plus $1,000 per month for accounting and audit. Build the estimate with separate fields for upfront legal work, state filings, policy drafting, compliance monitoring, and renewals. The spend depends on counsel quote, state count, and filing volume.

Upfront legal work

State filings

Policy drafting

Compliance monitoring

Renewals

Control the spend

Do not chase the cheapest route. Keep the state footprint tight at launch, then add states only after counsel signs off on filings, disclosures, and complaint rules. Reuse core policies where you can, but update them where local law changes. The cleanest savings usually come from fewer states, not thinner compliance.

What drives cost

The cost driver is the regulatory pathway, not one license. A lender model, broker model, or bank-partner model changes legal work, filings, and monitoring. Add one new state and you usually add another filing, more policy review, and renewal tracking. Decide the footprint before product launch, because that choice sets the legal budget.

Data, Underwriting, Fraud, And Verification Startup Expense

Core checks

This stack covers identity verification, AML checks, bank account verification, credit bureau access, income verification, fraud scoring, and risk rules. It is a trust and compliance cost, not a back-office add-on. The source model pegs data verification and credit scoring at 30% of first-year revenue, easing to 20% by year five.

Price it

Build the estimate from applications × per-check fees × loan types, plus monthly data usage fees, setup work, and any adverse-action workflow where applicable. Use separate inputs for vendor quotes, months of coverage, and pull volumes. With first-year loan values of $5,000, $15,000, and $20,000, deeper checks should scale with loan size.

Control it

Cut waste by tiering checks: keep full verification for larger loans and use lighter rules only where risk supports it. Reuse verification data, block duplicate pulls, and tune fraud rules so they do not flood the team with false positives. One clean rule set beats a messy pile of vendor tools when lender confidence matters.

Budget fit

The borrower mix starts at 600% personal, 250% debt consolidation, and 150% home improvement, so underwriting rules should reflect different loan behavior and file depth. That mix shapes data spend, because each category can justify a different verification path, review step, and evidence trail. Keep the spend linked to loan performance, not just application volume.

Payments, Servicing, Custody, And Transaction Infrastructure Startup Expense

Payment flow

This cost covers ACH rails, payment processor onboarding, borrower disbursements, repayment collection, lender distributions, reconciliation, servicing workflows, escrow or custodial handling, and exception handling. It is transaction infrastructure, not loan capital, so keep it outside funding inventory. Estimate it from expected payment events, provider quotes, implementation fees, and months of coverage.

Cost drivers

For planning, use fee per transfer times expected volume, plus setup work for vendor onboarding and compliance review. The model assumes 40% of revenue in year 1 from servicing and transaction fees, easing to 30% by year 5. Seller extra payment processing fees start at $5 and rise to $10.

Count monthly disbursements.

Count repayment collections.

Count lender payouts.

Keep it lean

Keep costs down by using one provider for ACH, payouts, and reconciliation where compliance allows. Don’t bury regulated fund-flow checks inside the build; treat onboarding and review as separate setup lines. The fastest savings come from fewer manual exceptions, cleaner repayment data, and tighter servicing rules.

Standardize exception rules early.

Reduce manual payment fixes.

Separate compliance work from coding.

Regulated rails

If fund flows are regulated, special providers can be required for custody or escrow. Budget their onboarding, legal review, and account setup before launch, because those items move on a different timeline than software. The cost driver is not just payment volume; it is also how many rails, accounts, and control steps each loan needs.

Launch Team, Insurance, And Go-To-Market Startup Expense

Budget First

This bucket is mostly pre-opening expense and working capital, not CAPEX. For a peer-to-peer lending launch, it covers founder pay, contractors, compliance ops, customer support, risk management, product management, launch campaigns, and insurance. Here’s the quick math: $120,000 CEO pay is $10,000/month, insurance is $1,000/month, and first-year acquisition spend is $350,000.

Build The Estimate

Use headcount × months, contractor quotes, $220 lender CAC, $180 borrower CAC, and campaign count to size the launch budget. Add errors and omissions, cyber liability, and directors and officers coverage as monthly premiums, then keep compliance work separate from software build. The model also shows 30% customer support cost in year one, so don’t leave service out.

Count people by launch month

Use quotes, not guesses

Price support from day one

Keep It Lean

Hire to milestones, not comfort. Use contractors for short bursts, stage the launch budget by channel, and hold paid acquisition until lender and borrower conversion is proven. The main mistake is overstaffing before the first funded loan. If compliance or support is thin, though, cost cuts just create rework and slower approvals.

Start with one launch channel

Delay full-time hires

Protect compliance coverage

Split The Message

With $220 lender CAC and $180 borrower CAC, one message will not fit both sides. Lenders want return, risk, and reporting; borrowers want speed, rate, and approval clarity. A single go-to-market script burns the $350,000 acquisition budget fast, especially when support and compliance must handle two very different workflows.

Compare 3 Startup Cost Scenarios

Launch cost scenarios

Lean MVP keeps states, integrations, and paid acquisition tight. Base launch matches the model's Year 1 spend and Month 14 cash trough, while Full adds more states, security, support, lender segments, and runway.

Lean, Base, and Full launch cost comparison

Scenario

Lean LaunchMVP test

Base LaunchCompliant launch

Full LaunchScale launch

Launch model

Single-state MVP with basic loan matching, limited integrations, and a short runway.

Compliant launch across the first target states using the model's Year 1 marketing and overhead inputs.

Multi-state launch with deeper security, broader integrations, and a larger runway.

Typical setup

Use core loan servicing, simple credit checks, and a small team while delaying broad state work and paid scale.

Build the core platform, use the model's $220 lender CAC and $180 borrower CAC, and fund enough liquidity for the Month 14 trough.

Add more compliance work, more support coverage, more lender segments, and more operational depth.

Cost drivers

Single-state compliance

basic build

limited integrations

low paid acquisition

lean support

Year 1 marketing $350k

$16k monthly overhead

founder salary $120k

servicing fees

credit scoring

Multi-state licensing

deeper security

larger support

more lender segments

longer runway

Planning rangeCAPEX only

$250,000 - $500,000Lower cash need

$1.1M - $1.3MModel cash need

$1.5M - $2.5MHigh runway need

Best fit

Founders testing demand before they fund broad compliance, integrations, or heavy marketing.

Teams ready to fund the full Year 1 model and carry cash to the $299k minimum point.

Teams that want to scale beyond the first states and serve more lender segments from day one.

!

Planning note: These scenario ranges are researched planning assumptions, not vendor quotes. Use them to compare launch scope, cash need, and operating depth.

Plan runway beyond the software build because fixed costs start before loan volume is stable The provided model shows $16,000 in monthly fixed overhead, $120,000 in annual founder salary, and $350,000 in first-year borrower and lender acquisition spend That is $662,000 before unpriced CAPEX, licensing, legal setup, and any liquidity reserve

Usually, yes, but the exact path depends on structure, states, loan product, and whether the platform acts as a lender, broker, servicer, or marketplace Budget for qualified US fintech counsel The model includes a $2,500 monthly legal and compliance retainer, plus $1,000 monthly accounting and audit fees, but upfront licensing costs are not separately priced

You may be able to if the platform only connects borrowers and lenders and does not lend from its own balance sheet, but the structure must be validated Loan capital should be shown separately from startup expenses The model’s revenue assumes platform fees, including a $50 fixed commission and 30% of loan value in the first year

The provided data does not include a launch timeline, so don’t force one into the budget Build the model by phase: startup period, launch month, early ramp-up period, and first operating year Monthly costs matter because overhead begins at $16,000 per month, while cloud, security, legal, insurance, rent, admin, and audit fees all start in Month 1

Narrow the first launch before adding states, loan types, and integrations A lean plan should limit the regulatory footprint, focus borrower acquisition, and avoid custom features that don’t affect underwriting or repayment The model already carries $200,000 for borrower acquisition, $150,000 for lender acquisition, and $8,000 per month for cloud, SaaS, maintenance, and security

About the author

Dennis Coleman

Small Business Consultant

Dennis Coleman is a small business consultant who writes for Financial Models Lab about everyday business finance and business plan basics. He helps readers compare business ideas by showing how small businesses really operate day to day, from realistic expenses to practical cash flow assumptions. Dennis focuses on building a basic plan before investing money, giving entrepreneurs clear, credible guidance they can use to make smarter decisions.

Choosing a selection results in a full page refresh.