Personal Finance App Startup Costs: $87k CAPEX Plus $208k Cash

This personal finance app cost breakdown covers $87,000 in launch CAPEX, pre-opening setup, security, compliance, launch marketing, working capital, and the cash needed through the early ramp-up period The model shows $208,000 minimum cash, breakeven in Month 29, and first-year EBITDA of -$338,000 These are researched planning assumptions, not vendor quotes, revenue guarantees, or fixed launch costs

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a personal finance app.

!

What's excluded For capitalized startup assets only. Excludes working capital, payroll runway, deposits, debt service, inventory, recurring cloud usage, subscriptions, customer support, performance marketing, app store fees, and revenue-based aggregator fees.

Calculate Fuding Needs

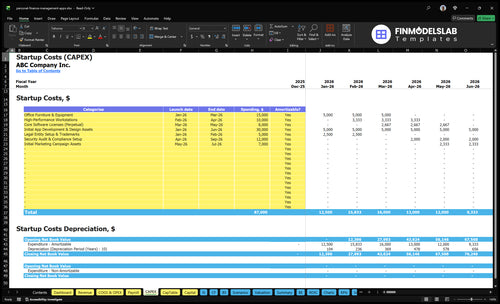

Startup cost summary

This table summarizes the main app build costs and the cash reserve kept outside CAPEX for launch.

Highlighted CAPEX$75,000Base planning example

Excluded cash needs$208,000Outside CAPEX total

Funding need$283,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Initial app development and design assets

$30,000

Scope of MVP build, design polish, and revisions.

Yes

Office furniture and equipment

$15,000

Number of desks, chairs, and setup quality.

Yes

Security audit and compliance setup

$12,000

Audit depth and compliance prep scope.

Yes

High-performance workstations

$10,000

Workstation specs and number of engineers.

Yes

Core software licenses, perpetual

$8,000

License count and vendor tier.

Yes

Minimum cash reserve

$208,000

Payroll, rent, marketing, and recurring app costs through breakeven.

Lean keeps the app simple and tests demand with manual budgeting and limited integrations. Base matches the modeled plan, while Full adds deeper analytics, broader coverage, and Year 2 specialist hires.

Lean, Base, and Full launch cost bands for a personal finance app

Scenario

Lean LaunchManual MVP

Base LaunchModeled plan

Full LaunchScale-ready

Launch model

Launch a manual-entry budgeting MVP with limited integrations and tight QA.

Launch the researched plan with full core features, standard QA, and normal marketing spend.

Launch with deeper analytics, broader account coverage, and support readiness built in from the start.

Typical setup

Use a small build, simple onboarding, and only the core spending and budget flows.

Cover the modeled $87,000 CAPEX, $150,000 Year 1 marketing, and the cash runway needed to reach Month 29 breakeven.

Add the data scientist and support specialist in Year 2 and keep room for heavier product and analytics work.

Cost drivers

Light app build

limited integrations

lower QA

smaller support load

basic launch marketing

CAPEX buildout

Year 1 marketing

security setup

fixed payroll

app store and cloud costs

Data scientist $95k

support specialist $50k

deeper analytics

broader coverage

higher cash burn

Planning rangeCAPEX only

$50,000 - $120,000Lowest setup

$87,000 - $208,000Model-based

$250,000 - $400,000Highest burn

Best fit

Best for founders testing demand before funding a full feature set.

Best for teams using the forecast as their first operating budget.

Best for teams aiming for faster feature depth and heavier support from day one.

!

Planning note: Scenario ranges are researched planning assumptions, not exact quotes or vendor bids.

How much money do I need to launch a personal finance app?

You don’t need one fixed number to launch a Personal Finance App; you need a budget by scope: $87,000 researched CAPEX for the build and at least $208,000 minimum cash need when working capital and operating runway are included, as explained in What Is The Primary Goal Of Personal Finance App To Enhance User Financial Well-Being?. The pressure point is cash burn: Year 1 EBITDA is -$338,000, Year 1 marketing is $150,000, breakeven lands in Month 29, and payback takes 44 months.

Budget by scope

Lean MVP: manual entry first

Bank sync raises build cost

Categorization adds data cleanup work

Analytics need tested user flows

Cash to protect

Separate build from working capital

Plan recurring support costs

Fund security before launch

Expect runway through Month 29

What hidden costs of starting a personal finance app should I budget for?

If you’re budgeting a Personal Finance App, split one-time launch costs from monthly working capital. For a quick reality check on earnings, see How Much Does The Owner Of Personal Finance App Make? Start with about $24,000 before launch, then plan for about $4,000/month plus 15% of Year 1 revenue for cloud hosting and data security; these are operating costs, not CAPEX, unless you capitalize them.

Launch Costs

$5,000 for legal setup

$12,000 for security and compliance

$7,000 for launch assets and QA

$24,000 total pre-opening cash

Monthly Burn

$2,000/month legal and accounting retainer

$800/month internal software

$700/month base security platform

$500/month support software

How do I calculate funding needed for a personal finance app?

For the Personal Finance App, start with $87,000 of CAPEX, $208,000 of minimum cash, and $150,000 of Year 1 marketing, then add pre-opening spend, operating runway, and contingency, and subtract any committed founder cash or outside financing. The model also assumes launch setup from Month 1 through Month 9, plus $6,000 a month in fixed costs and a -$338,000 Year 1 EBITDA gap.

Funding formula

CAPEX: $87,000

Minimum cash: $208,000

Marketing budget: $150,000

EBITDA gap: -$338,000

Downside checks

CAC above $25

Visitor-to-trial below 30%

Trial-to-paid below 250%

$6,000 monthly fixed cost load

Key Takeaways

Core app build is the biggest upfront cost.

Bank data fees fall from 25% to 15%.

Security and legal setup starts at $12,000.

Launch marketing is separate from recurring spend.

Personal Finance App Core Five Startup Costs

App Development and Product Build Startup Expense

Build Cost

The biggest scope-sensitive startup cost is the app build. Initial app development and design assets are budgeted at $30,000 over the startup period, before payroll and launch spend.

Feature Scope

A manual-entry MVP can stop at user accounts, budgets, expense entry, and basic reporting. A bank-connected product adds sync, categorization, refresh rules, and error handling. A full platform layers in admin tools, notifications, and deeper analytics.

Keep It Lean

To hold the bill down, ship the manual-entry MVP first and protect scope. Freeze new features until users prove they need bank sync and automation. Rework is the hidden cost here, so clean flows and tight specs save more than bargain coding.

Payroll Split

Here’s the quick math: a lead software engineer at $110,000 a year is about $9.2k a month, and a CEO/founder at $120,000 is $10k a month. Keep those salaries in operating expense; only build work that creates the app asset belongs in capitalized development cost.

UX, UI, and Product Design Startup Expense

Design Scope

For a finance app, UX/UI is not decoration. It covers onboarding, budget setup, dashboard views, spending insights, account-linking screens, accessibility, prototype testing, error states, and app store screenshots. The core design and build assets are budgeted at $30,000, while launch creatives sit in the $7,000 marketing asset line.

Cost Inputs

Estimate this with screen count, revision rounds, and asset types. Use the number of flows, wireframes, high-fidelity screens, and screenshot sets to price quotes. The key job is to make balances, categories, and permissions easy to read. Here’s the quick math: more screens and more testing push cost up fast.

Keep It Tight

Cut waste by reusing components across onboarding, charts, and alerts, and by testing low-fidelity prototypes before polish. Don’t pay for visual extras until flows work. One clean rule: fix confusion first, style second. If the product needs deeper UX later, plan for a $85,000 UI/UX designer starting in Year 3 instead of hiring too early.

Activation Link

Design should drive activation, not just look polished. In Year 1, the plan assumes 30% visitor-to-free-trial conversion and 250% trial-to-paid conversion, so every screen must reduce drop-off at signup and account link. What this estimate hides: poor balance labels, category errors, and permission friction can break trust fast.

Bank Integration and Financial Data API Startup Expense

What this cost covers

A bank-linked personal finance app needs bank sync, transaction feeds, account linking, authentication, refresh schedules, categorization rules, reconciliation, and error handling. The biggest variable is the financial data aggregator fee, which is modeled at 25% of revenue in Year 1, then 22%, 19%, 17%, and 15% by Year 5.

How to estimate it

Price it from revenue × fee rate, then add pre-launch integration testing and post-launch support load. Cost moves with provider choice, account volume, data depth, and refresh frequency. Here’s the quick math: if revenue changes, the fee changes with it, so this is a live operating cost, not a one-time build expense.

Year 1: 25% of revenue

Year 2: 22% of revenue

Year 3: 19% of revenue

Year 4: 17% of revenue

Year 5: 15% of revenue

How to keep it under control

Keep the first release tight: connect only the accounts and refresh schedules you truly need, then expand after launch. Clean error handling and good categorization rules cut support churn, which matters because bad syncs create manual work fast. Do not overbuild deep data pulls on day one; every extra feed and refresh can push fees and support time up.

What to budget first

Budget for a full integration test cycle before launch and a steady support process after users start linking accounts. The cost is driven less by the app shell and more by how often data refreshes, how many transactions flow in, and how much cleanup is needed when feeds break or categories misfire.

Security, Privacy, and Compliance Startup Expense

Security Base

The app needs encryption, secure authentication, user consent, a privacy policy, terms of service, access controls, and data retention planning. Budget $12,000 for security audit and compliance setup, plus $700 per month for the base data security platform. That is the minimum line item for protecting user data and keeping launch risk in check.

Cost Inputs

Here’s the quick math: use one-time setup at $12,000, then add $700 per month for tooling and $2,000 per month for legal and accounting retainer support. Add penetration testing and audit readiness to the scope. If the product only tracks budgets, costs stay lower; extra licenses may apply only for payments, lending, investing, stored funds, or regulated advice.

Keep It Lean

Use one compliant data stack, standard policies, and a tight permission model before adding fancy controls. Reuse templates for privacy policy and terms, then review them with counsel instead of custom drafting from scratch. Avoid buying regulated-product licenses too early. If onboarding feels unsafe or unclear, trust drops fast and churn rises, even if the budgeting features work well.

Trust Matters

Security spend is not optional overhead; it is part of product quality. A finance app that handles sensitive account data needs clear consent, audit trails, and steady monitoring so users feel safe linking accounts. If the experience feels risky, people stop connecting data, and that hits activation, retention, and subscription conversion.

Launch Readiness and Go-to-Market Startup Expense

Launch Spend Split

Launch readiness is a one-time setup cost, while marketing is recurring operating spend. For a personal finance app, that means beta testing, QA, app store setup, analytics, support tools, launch content, onboarding materials, and early acquisition tests sit apart from the $150,000 Year 1 marketing budget.

One-Time Assets

The $7,000 initial marketing campaign assets are launch assets, not monthly spend. Use it for screenshots, ads, landing pages, and onboarding creatives. Estimate it with vendor quotes and asset counts, then keep it on the launch budget so you do not bury startup setup inside the Year 1 media plan.

Early Funnel Math

Here’s the quick math: with $25 CAC, 30% visitor-to-trial conversion, and 250% trial-to-paid conversion as given, your launch model lives or dies on traffic quality. Pair that with $500 per month for customer support software and you can see how fast fixed tools add up before paid growth starts working.

Year 1 Pressure

Performance marketing at 80% of revenue in Year 1 is a heavy load, so watch payback from day one. If launch content, onboarding, and analytics are weak, CAC rises fast and trial conversion slips. What this estimate hides is support time, failed acquisition tests, and the cost of fixing confused users after install.