How Much Does It Cost To Start A Record Label? A $569K Year 1 Plan

Based on the provided model, the cost to start a record label should be planned at at least $569,200 for the first operating year before release-specific costs and unquoted CAPEX That figure includes $150,000 in first-year acquisition marketing, $340,000 in payroll, and $6,600 per month in fixed operating costs One-time CAPEX should be kept separate because the data does not price computers, audio gear, cameras, office assets, or capitalized software Artist advances, recording budgets, videos, PR, royalty reserves, and working capital can push the total funding need much higher, especially if the label funds multiple artists before revenue is predictable

Calculate Fuding Needs

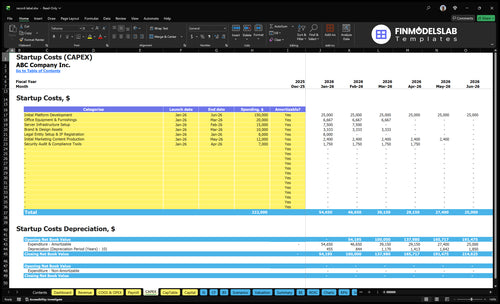

Startup cost summary

This table summarizes the main startup CAPEX items and the non-CAPEX cash reserve needed to launch a record label.

Highlighted CAPEX$203,000Base planning example

Excluded cash needs$166,000Outside CAPEX total

Funding need$369,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Initial Platform Development

$150,000

Build scope and launch complexity

Yes

Office Equipment & Furnishings

$20,000

Workstations and office setup

Yes

Server Infrastructure Setup

$15,000

Hosting and setup capacity

Yes

Brand & Design Assets

$10,000

Creative production and identity work

Yes

Legal Entity Setup & IP Registration

$8,000

Formation, filings, and rights protection

Yes

Working Capital Buffer

$166,000

Negative minimum cash and first-year operating spend

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a record label, not working capital or ongoing operating spend.

!

CAPEX only This calculator covers capitalized startup assets only. It excludes artist advances, recording sessions, legal fees, payroll, marketing, royalties, subscriptions, deposits, inventory, debt service, working capital, and other non-CAPEX funding needs. The provided data does not include exact CAPEX quotes, and operating costs start in Month 1.

Startup cost swings fast when you move from a founder-led digital label to a staffed full-service model. The gap comes from payroll, marketing, equipment, and artist support, plus release-level cash needs.

Lean, Base, and Full launch cost comparison for a record label

Scenario

Lean LaunchDigital-first

Base LaunchSmall independent

Full LaunchFull-service

Launch model

A founder-led digital label keeps the team thin and pushes most work to the owner.

The base model uses the provided first-year operating base of $569,200 before unpriced CAPEX and release-specific advances or recording.

A full-service label adds more artists, more releases, and more cash tied up in promotion and reserves.

Typical setup

Use a light setup with basic tools, limited rent, and low paid acquisition.

Use the core team, standard marketing, and normal legal and admin overhead.

Use a larger staff, more contractors, bigger content spend, and higher royalty reserves.

Cost drivers

Founder labor

lower payroll

basic software

light marketing

minimal equipment

Core payroll

marketing spend

platform build

legal and compliance

artist support

Multiple artists

higher release volume

videos and publicists

contractor spend

royalty reserves

Planning rangeCAPEX only

$250,000 - $400,000Founder-led band

$569,200 - $700,000Base budget

$900,000 - $1,400,000Scaled build

Best fit

Best for owners who want to test releases with low fixed costs and heavy founder time.

Best for a small independent label that wants a structured launch without a large studio footprint.

Best for teams that want a broader roster and can fund higher upfront spend and working capital.

!

Planning note: These scenario ranges are researched planning assumptions, not exact quotes, and they should be used as launch bands until you price advances, recording, video, and CAPEX.

How do you fund a record label after estimating startup costs?

Fund a Record Label around cash timing, not just the $569,200 first-year base. That spend comes before release-specific production and unpriced CAPEX, while streaming and licensing cash usually land later and royalty payouts hit early. Build runway for the gap, then tie it to the monthly fee stack: $29 solo artist, $49 band, $79 producer, $7 engaged fan, and $15 super fan. The next step is a financial model that links artist pipeline, fan growth, release budgets, royalties, and break-even timing.

Fund the gap first

Cover $569,200 before releases.

Reserve cash for royalty payouts.

Plan for delayed streaming revenue.

Add buffer for unpriced CAPEX.

Model the runway

Track artist pipeline by month.

Model fan growth and acquisition.

Use 150% variable commission.

Test break-even every month.

What hidden costs of starting a record label are easy to miss?

The hidden costs of a Record Label are usually not gear; they’re the cash drain from royalty accounting, contract edits, takedowns, disputes, metadata cleanup, distributor fees, marketing overruns, contractor retainers, insurance, and tax compliance. For a quick read on the owner side, see How Much Does The Owner Of A Record Label Typically Make?—because the business can look light on equipment and still burn cash fast. Here’s the quick math: the fixed base here is $4,800/month.

Fixed monthly burn

$2,500 legal and compliance

$1,000 accounting

$500 insurance

$800 software

Year 1 variable drag

50% technology infrastructure

25% payment gateway fees

30% content support

40% marketing and sales support

How much should a record label budget for artists and recording?

A Record Label should budget artist advances and recording spend as deal cost, not as capital spend (CAPEX), because the real risk is cash timing and future royalty payouts. Your Year 1 mix is 60% solo artists, 30% bands, and 10% producers, but there are no advance or studio quotes here, so the budget has to start with release count and rights terms. Ask how many releases hit before the first royalty statement, and whether the label owns masters or only licenses finished recordings.

Budget the release cost

Advances to artists

Demo acquisition and buyouts

Studio time and engineers

Mixing, mastering, QC

Separate the legal risk

Keep payroll off signing budget

Track long-term royalty liabilities

Price session musicians and beat licenses

Budget artwork and videos

Key Takeaways

Legal setup is pre-opening and operating expense, not CAPEX.

Year 1 marketing totals $150,000, split $50k artist-side and $100k fan-side.

Buyer CAC is $15; seller CAC is $750.

Recording and admin costs scale with release volume.

Record Label Core Five Startup Costs

Legal, Rights, And Business Formation Startup Expense

Formation and rights

This cost is pre-opening and operating expense, not CAPEX. It covers entity formation, the operating agreement, artist and producer agreements, split sheets, licensing terms, trademark review, copyright registration workflow, and music attorney review. The source model sets legal and compliance at $2,500 per month, or $30,000 in year one.

Budget drivers

The quick math starts with $2,500 monthly, then scales by deal count and rights complexity. Ask how many artist agreements you need, whether masters are owned or licensed, how producer points are documented, and whether publishing administration must be coordinated. Those inputs decide review time, filing volume, and how much attorney work sits inside the $30,000 year-one budget.

Count artist contracts first.

Separate owned from licensed masters.

Track producer points in writing.

How to keep it tight

Use one standard contract stack, then customize only the deal terms that change money or rights. Batch trademark and copyright work, and keep split sheets and license terms tied to each release. The main mistake is mixing legal spend with equipment buys; that hides the real run rate and can understate first-year cash needs by $30,000.

Standardize your templates early.

Batch filings to save time.

Keep legal off CAPEX.

Workflow control

Build the workflow around release timing: form the entity first, then clear ownership, then sign artist and producer papers before distribution. If publishing administration is in scope, coordinate it before launch so royalty splits, registrations, and statements match the contract terms from day one.

Recording And Master Production Startup Expense

Cost scope

This cost covers studio sessions, producers, engineers, mixing, mastering, session musicians, beat licenses, artwork, and first-release video assets. Treat it as release startup expense, not CAPEX, unless you buy long-lived gear. The right estimate depends on release count, roster size, and whether artists deliver finished masters or need full production support.

Estimate inputs

Build the budget from three inputs: number of releases, who supplies the master, and which outside vendors you use. Ask for quotes on studio time, mixing, mastering, and video work, then add recoupable artist spend separately. The source data gives no per-song, per-EP, or per-album quotes, so one blanket number will miss the real need.

Spend control

Keep costs down by using finished masters where possible, reusing trusted engineers, and limiting video spend to the first slate that actually supports launch. Avoid buying gear too early; that moves spend into CAPEX only if the equipment is long-lived and owned. One clean rule: pay for release assets once, not twice.

Budget lines

Split the budget into owned gear CAPEX, outsourced production costs, and recoupable artist spend. That keeps approvals clear and stops recording costs from leaking into marketing or legal lines. If an artist delivers a finished master, the production line should shrink fast; if not, it should expand only with the release slate.

Launch Marketing And Promotion Startup Expense

Launch Spend

Marketing here is working capital, not equipment. Budget for branding, press, playlist pitching, content, music videos, social ads, influencer work, radio promo where used, release events, and publicist retainers. The source model sets $150,000 for Year 1 acquisition marketing, split into $50,000 for artists and $100,000 for fans.

Size The Budget

Here’s the quick math: $15 buyer CAC means about 6,667 buyer acquisitions from the $100,000 fan budget. A $750 seller CAC means about 67 artist-side acquisitions or prospects from the $50,000 artist budget. To estimate the real need, add campaign counts, months of coverage, and quote-based unit costs.

$15 buyer CAC

6,667 buyer acquisitions

$750 seller CAC

Control The Burn

The trap is treating launch promo like one clean lump sum. In practice, add 40% for marketing and sales support, so the $150,000 base becomes $210,000. Keep the spend tied to release dates and roster targets, and avoid locking in long retainers before you know which channels convert.

Use short, testable campaigns

Track CAC by channel

Review spend monthly

Working Capital

Put this cost in the startup cash plan, not the asset schedule. If artist-side conversion is slow, the $50,000 pool can disappear before roster depth builds, so the key control is pacing spend against signed artists, release timing, and buyer growth.

Distribution, Metadata, And Royalty Administration Startup Expense

Admin Stack

This cost covers distributor setup, ISRC and UPC workflows, royalty statements, accounting, publishing admin coordination, website, email tools, and catalog management. Use $800/month in software licenses and $1,000/month in accounting and audit fees, or $21,600 in Year 1 before variable fees and cleanup labor.

Cost Inputs

Estimate this by counting releases, statements, and catalog lines. Add fields for metadata cleanup, takedowns, royalty reserve policy, statement timing, and catalog reconciliation. The clean split is subscriptions, admin labor, and capitalized tech assets, because only long-lived development belongs on the balance sheet.

Count releases per month

Price cleanup hours separately

Set reserve timing rules

Keep It Lean

Keep this lean by using one system for ingestion, statements, and reconciliations, then automate takedown and metadata checks before each release. The model also carries 50% technology infrastructure costs and 25% payment gateway fees in Year 1, so fixed admin spend is only part of the bill. Avoid overcapitalizing software or staff time.

Automate metadata checks

Reconcile before statements

Review gateway fees monthly

Close Calendar

Track statement timing, reserve releases, and catalog reconciliation on day one. If takedowns or metadata fixes land late, payable balances drift and audit work grows fast. A simple close calendar — ingest, match, reserve, issue, reconcile — keeps the back office from becoming emergency labor.

Artist Acquisition And Initial Roster Startup Expense

Signing Cash

$50,000 in Year 1 artist-side acquisition marketing at $750 CAC buys about 67 artist-side acquisitions or prospects. Keep that money separate from payroll, recording, and long-term royalty liabilities. Because no advance amounts are provided, the real signing budget still needs deal-level inputs: advances, demos, travel, creative retainers, and recoupment terms.

What It Covers

This cost covers the cash you spend to win talent, not to run the team. Include advances, demo buys, development support, travel, and creative retainers. One clean split sheet and one clear recoupment rule can save you from messy disputes later. Budget by deal, not by vibe.

Set per-deal advance caps.

Track recoupable spend separately.

Price travel by project.

Budget Inputs

Start with the roster mix: 60% solo artists, 30% bands, and 10% producers. Then add the number of deals, advance size, months of support, and expected travel. If you sign 67 prospects at the model CAC, even small per-artist spend changes the budget fast.

Control Cash

The safest way to control cash is to stage signings in steps. Use short-term deals, milestone-based advances, and clear recoupment from day one. Don’t hide acquisition spend inside payroll or production. If the contract needs publisher or producer terms, get legal review before money moves.