Savings Bank Startup Costs: Plan For $665K Monthly Overhead

Based on the model, the documented operating launch base for a savings bank starts with $66,500 per month in fixed costs, or $798,000 across the first operating year Known first-year executive payroll from the provided roles adds at least $430,000 before any missing or role-specific staffing detail is layered in That means the visible first-year operating-cost floor is at least $1228 million, before branch CAPEX, charter work, additional payroll, marketing, and working-capital cushion Regulatory capital and liquidity reserves are separate from ordinary startup expenses and can exceed the operating launch budget, especially with Year 1 deposits of $45 million and Year 1 loans of $30 million

Estimate Startup Costs with Calculator

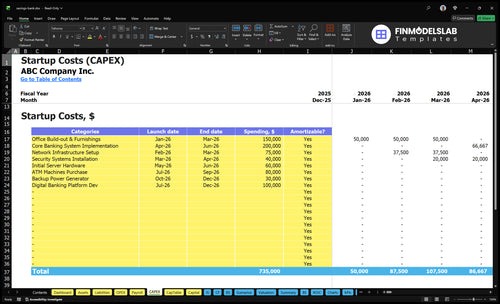

Startup CAPEX Calculator

Estimates capitalized startup assets only for a savings bank, including branch buildout, equipment, security, and implementation costs.

!

Excluded Costs This calculator covers capitalized launch assets only. It excludes deposits, regulatory capital, liquidity reserves, working capital, payroll runway, rent runway, debt service, inventory, operating losses, and non-capitalized software subscriptions.

Calculate Fuding Needs

Startup cost summary

This table sums startup CAPEX and excluded cash needs for a savings bank launch.

A limited-branch launch keeps cash needs lower; a fuller launch adds tech, staff, compliance, and marketing, so startup cost rises fast with scope.

Lean, base, and full launch cost comparison for a savings bank.

Scenario

Lean LaunchLimited branch

Base LaunchSource match

Full LaunchBroader launch

Launch model

Launch one branch with a narrow product set and tighter hiring.

Run the source-model community bank with the planned deposit and loan mix.

Launch with heavier technology, a larger staff, deeper compliance testing, and a broader loan mix.

Typical setup

Use lower branch build-out, lean tech, and basic support functions.

Use the model's $66,500 monthly fixed costs, $798,000 first-year fixed overhead, $45 million Year 1 deposits, and $30 million Year 1 loans.

Use more launch marketing, more staff, stronger systems, and wider lending support.

Cost drivers

Lower branch build-out

core banking software

smaller team

basic compliance

launch marketing

Office rent

core banking software

compliance fees

customer service staff

FDIC premiums

Technology rollout

larger staff

compliance testing

marketing spend

broader loan mix

Planning rangeCAPEX only

Below base launch spendLowest cash need

$1.53M startup spendModel baseline

Above base launch spendHighest spend

Best fit

Best for a local community launch with one branch and a tight opening budget.

Best for a community savings bank that wants the source-model operating plan.

Best for a fuller multi-service launch that can fund more systems and staff.

!

Planning note: These scenario ranges are planning assumptions from the model, not exact vendor quotes or guaranteed costs.

What hidden costs of starting a savings bank should founders budget for?

For a Savings Bank, the hidden bill starts before deposits or loan income ramp, so founders should split operating spend from capital spending (CAPEX) and regulatory capital; if you want the owner-side math, see How Much Does Owner Make From Savings Bank Business?. Plan on a $66,500 monthly fixed cost base, plus pre-opening payroll, rent before opening, cybersecurity reviews, vendor due diligence, compliance testing, insurance, audits, website, launch marketing, and customer education, with 8% Year 1 marketing and customer acquisition.

Launch costs

Pre-opening payroll starts first.

Rent can hit before launch.

Vendor due diligence needs cash.

Compliance testing delays revenue.

Fixed monthly base

$10,000 rent each month.

$25,000 core banking software.

$12,000 hosting and $6,000 cybersecurity.

$3,000 Federal Deposit Insurance Corporation premiums.

What do savings bank charter costs and bank regulatory application costs include?

Savings Bank charter and application costs cover more than a filing fee: they include legal counsel, regulatory consultants, FDIC filing work, charter prep, board formation, governance documents, policies, audits, and compliance readiness. Budget for ongoing readiness too, including about $5,000 per month in regulatory compliance fees and $4,000 per month in professional services for legal and audit. The key point is simple: application fees are only part of the cost, and approval is not guaranteed.

Startup costs

Legal counsel for structure and filings

Regulatory consultants for application prep

FDIC filing work and state or federal charter prep

Board formation, governance docs, and policies

Ongoing readiness

$5,000 per month for compliance fees

$4,000 per month for legal and audit services

Compliance testing and review cycles

Ask about charter path, board experience, and organizing group

How much money is needed to start a savings bank?

A Savings Bank needs more than startup cash: the model shows $66,500 in fixed monthly costs, or $798,000 in first-year fixed overhead, before branch CAPEX, technology, charter work, working capital, regulatory capital, and liquidity funding. Tie the raise to the operating plan and customer trust signals like What Is The Most Important Indicator Of Customer Satisfaction For Savings Bank?, because Year 1 assumes $45 million in deposits, $30 million in loans, and $40 million in interest-bearing assets.

Core funding need

$66,500 fixed costs per month

$798,000 first-year fixed overhead

$430,000+ visible executive payroll

CEO, lending, and operations roles

Balance sheet plan

$45 million planned Year 1 deposits

$30 million planned Year 1 loans

$40 million interest-bearing assets

Add charter, liquidity, and capital funding

Key Takeaways

Compliance and legal cost $9,000 monthly before launch.

Core tech adds $43,000 monthly plus processing fees.

Year one payroll tops $430,000 before revenue.

Rent, insurance, and marketing keep burn high.

Savings Bank Core Five Startup Costs

Charter, Regulatory Application, And Compliance Formation Startup Expense

Charter Setup

Savings bank charter work starts with the licensing file: organizing group expenses, governance setup, compliance and risk policies, board materials, regulator readiness, and a plan for a Federal Deposit Insurance Corporation (FDIC) deposit insurance application. Estimate it from counsel hours, filing fees, policy count, and review cycles. Treat this as pre-opening professional expense, not regulatory capital or an approval event.

Cost Run-Rate

The model uses $5,000 per month for regulatory compliance fees and $4,000 per month for legal and audit services from Month 1 through Month 60. That is $9,000 monthly, or $540,000 over five years. Budget it as startup operating expense, separate from capital and from one-time filing costs.

Keep It Lean

Cut waste by locking scope early: one lead law firm, one policy set, one board pack calendar, and one owner for regulator follow-up. Don’t save money by skipping controls, because weak drafts create rework and delay. The cleanest savings come from fixed monthly retainers and tight issue logs, not from trimming compliance work.

Budget Check

Quick math:$9,000 a month for 60 months equals $540,000, before other startup work. Keep this bucket in pre-opening expense so the board sees a clear runway for charter, licensing, and readiness work instead of mixing it with regulatory capital.

Hiring, Training, And Pre-Opening Payroll Startup Expense

Pre-Opening Payroll

Before the first deposit lands, this cost covers recruiting, onboarding, training, and paying the team that gets the bank ready to open. The visible base is at least $430,000 in Year 1 from the CEO at $200,000, Head of Lending at $160,000 on 0.5 FTE, and Head of Operations at $150,000. Treat it as working capital, not CAPEX.

Budget Inputs

Estimate this with headcount × salary × pre-revenue months, then add onboarding and training time. Include executive hires, the compliance officer, operations staff, lending staff, deposit staff, and branch staff. FTE, or full-time equivalent, matters because the lending role is only 0.5 FTE in Year 1. The base three roles alone run about $35.8k per month.

Count months before opening

Use loaded salary timing

Add training and onboarding

Control Burn

Stage hires to the launch date so payroll starts when work starts, not months early. Use 0.5 FTE where the job can stay part-time, but don’t squeeze compliance or operations too hard. If onboarding slips, idle payroll rises fast and launch timing gets messy. The clean win is hiring only for the opening plan.

Hire in launch order

Delay noncritical roles

Protect compliance coverage

Runway Need

This spend belongs in the funding plan as runway, not equipment. On the named roles alone, the bank needs $430,000 in Year 1 before adding the compliance officer, operations staff, lending staff, deposit staff, branch staff, onboarding, and training.

Core Banking, Digital Banking, And Cybersecurity Startup Expense

Core Stack

A savings bank needs one-time setup for the core system, online and mobile banking, vendor links, data security, and BSA/AML (Bank Secrecy Act and anti-money laundering) controls. The recurring base is about $25,000 per month for core licenses, $12,000 for cloud hosting, $6,000 for cybersecurity, plus 30% Year 1 payment processing fees.

Charter Costs

Treat implementation support as one-time work and software, hosting, and payment processing as recurring. Charter work covers regulatory filing, governance, policies, board materials, and readiness for deposit insurance planning. Use the model $5,000 monthly compliance fee and $4,000 monthly legal and audit support from Month 1 through Month 60; the inputs are scope, counsel hours, and regulator questions.

Branch Buildout

Branch costs are separate from tech. Budget for leasehold improvements, teller counters, lobby, offices, signage, access control, cameras, alarms, vault or cash-handling gear, and IT hardware. Keep the physical CAPEX distinct from $10,000 monthly rent, $1,500 for utilities and maintenance, plus deposits and runway. Cost swings with branch size, security level, and local construction prices.

People, Risk, Launch

Pre-opening staff, onboarding, and risk spend hit cash hard before deposits scale. Use salary inputs for the CEO at $200,000, Head of Lending at $160,000 at 0.5 FTE, and Head of Operations at $150,000; Year 1 payroll is at least $430,000. Add $3,000 monthly FDIC insurance planning, $4,000 legal and audit, and keep marketing at 80% of Year 1 spend.

Insurance, Audit, Risk Management, And Launch Marketing Startup Expense

Compliance Cost

This line covers Federal Deposit Insurance Corporation (FDIC) insurance premiums, directors and officers insurance, the financial institution bond, accounting, independent audits, risk assessments, and regulator-ready policies. At $3,000/month for FDIC premiums and $4,000/month for legal and audit services, the base is $84,000 a year before any launch marketing.

Estimate It

Estimate it with months of coverage plus fixed quotes from counsel, auditors, and insurers. Include board materials, compliance policies, and opening risk reviews. If legal and audit support stays at $4,000/month, a 12-month plan is $48,000; add $36,000 for FDIC premiums and then layer bond and D&O quotes.

Marketing Order

Keep brand launch spend secondary: website, community outreach, and customer materials should support trust, not replace readiness. The model puts 80% of Year 1 marketing and acquisition effort behind compliance, systems, staffing, and controls, so don’t buy broad ads before policies, monitoring, and onboarding work.

Avoid Rework

Reuse the same website copy, outreach deck, and trust materials across channels, and hold paid ads until onboarding and controls are stable. That avoids paying twice for fixes. If compliance drags, the better savings move is to delay spend, not cheapen the controls.

Branch Buildout, Facilities, And Physical Security Startup Expense

Buildout Scope

This cost covers the branch fit-out: leasehold improvements, teller counters, offices, customer lobby, signage, access control, cameras, alarm systems, vault or cash-handling equipment, and IT hardware. Keep it separate from occupancy costs like $10,000 monthly rent, $1,500 monthly utilities and maintenance, plus rent deposits and runway.

Budget Inputs

Here’s the quick math: estimate by branch size, local construction quotes, and security level. Add separate line items for cash-handling gear and IT hardware. A one-site launch needs a different budget than a fuller network, so build each location on its own cost sheet and include occupancy runway before opening.

Use square feet and quotes

Separate CAPEX from rent

Model each site alone

Save Safely

Save money by shrinking the footprint, standardizing finishes, and matching security to actual cash volume. Don’t overbuild a network-style branch for a single location. The best savings come from simpler layouts and right-sized equipment, not from cutting cameras, access control, or other controls that protect cash and customers.

Smaller space cuts buildout

Right-size vault equipment

Keep core controls intact

Cost Drivers

The bill moves with branch size, security level, cash volume, customer-facing design, local construction cost, and whether you open one location or a broader network. More cash and more traffic usually mean more controls, more hardware, and a higher physical CAPEX total.