Tea Business Startup Costs: Plan For 50 Hectares In Year 1

You’re budgeting a tea business before the first harvest, so the cost model has to cover more than equipment This outline uses researched planning assumptions for a 50-hectare first operating year, including $200,000 of owned-land CAPEX and $72,000 of annual leased-land cash cost, but these are not binding vendor quotes

Calculate Fuding Needs

Startup cost summary

This table shows the main tea startup CAPEX and the non-CAPEX cash needed to cover launch runway.

Highlighted CAPEX$760,000Base planning example

Excluded cash needs$71,000Outside CAPEX total

Funding need$831,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

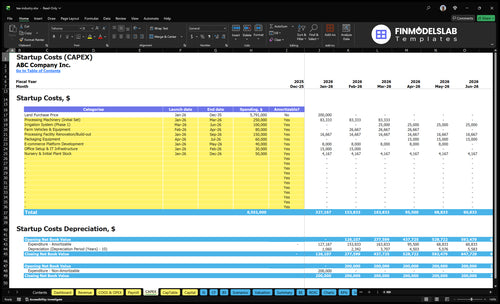

Processing Machinery (Initial Set)

$250,000

Line capacity and equipment spec

Yes

Owned Land Acquisition

$200,000

Owned hectares and land price

Yes

Processing Facility Renovation/Build-out

$150,000

Facility scope and finish level

Yes

Irrigation System (Phase 1)

$100,000

Coverage across cultivated area

Yes

Packaging Equipment

$60,000

Packaging line throughput

Yes

Working Capital Reserve

$71,000

Minimum cash deficit and launch runway

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a tea business.

!

Scope note This calculator covers only capitalized startup assets. It excludes tea inventory, botanicals, packaging consumables, payroll runway, rent deposits, permits, marketing, e-commerce fees, lease payments, debt service, working capital, and other pre-opening expenses; use separate startup inventory, pre-opening expense, and total funding need outputs for those items.

Tea startup costs jump as you move from online resale and packaging into blended production and then a full farm-and-processing build. More land, gear, and lease cash lift both upfront spend and cash risk.

Lean, Base, and Full tea launch cost comparison

Scenario

Lean LaunchFastest launch

Base LaunchOperational balance

Full LaunchHighest asset risk

Launch model

Sell packaged tea online or through private label, with no owned farm land.

Blend, package, and sell tea with a small processing room and wholesale readiness.

Run an owned-and-leased farm plus processing setup with full harvest and packaging operations.

Typical setup

Use inventory, packaging, ecommerce, compliance, and samples.

Add a blending room, equipment, storage, and packaging machinery for bulk and packaged tea.

Use 50 hectares with 20% owned land and 40 leased hectares, which implies about $72,000 a year in lease cash at Year 1 rates.

Cost drivers

Inventory

packaging

ecommerce

compliance

samples

Processing build-out

machinery

packaging equipment

storage

wholesale prep

Land purchase

land lease cash

irrigation

processing machinery

farm labor

Planning rangeCAPEX only

$70,000 - $150,000Lowest CAPEX

$250,000 - $500,000Balanced spend

$900,000 - $1,000,000Most working capital

Best fit

Best if you want to test demand fast and keep fixed assets light.

Best if you want a real operating base without full farm ownership.

Best if you want to control land, processing, and supply at scale.

!

Planning note: Scenario ranges are researched planning assumptions, not exact quotes or bids.

What hidden costs should a tea business budget for?

If you’re budgeting Tea Industry, the hidden cash hit is usually working capital, not equipment: deposits, pre-opening payroll, lease payments before revenue, testing, samples, freight, spoilage, and packaging waste all leave cash early. See the owner math in How Much Does The Owner Of Tea Industry Make?—the hard part is that harvest lands in just 6 months of the model year, but cash can leave long before sales return. Build cash for 60% yield loss, inventory lag, packaging buys, and customer payment terms.

Cash leaves first

Pay rent and utility deposits upfront.

Cover pre-opening payroll before sales.

Budget lab tests and label reviews.

Pay freight, spoilage, and packaging waste.

Cash timing risk

Cycle 1 fits bulk black and green tea.

Cycle 2 slows packaged premium black tea.

Cycle 3 slows packaged herbal blends most.

Reorders and payment terms trap cash.

What are the biggest costs to start a tea business?

The biggest startup costs in Tea Industry are land, a food-safe facility, equipment, and inventory cash. Here’s the quick math: land is the clearest driver at about $20,000 per owned hectare or $150 per leased hectare per month in Year 1, and costs rise fast if you need a blending room, processing facility, warehouse, tasting room, or retail shop. What this hides is the operating drag: 60% yield loss, 70% processing and packaging materials, 50% direct farm labor, plus 40% ecommerce transaction and shipping fees and 30% wholesale commissions where they apply.

Big startup cost drivers

Land: owned or leased

Facility: blending or processing space

Warehouse: storage and handling

Retail: tasting room or shop

Equipment and cash needs

Dryers, rollers, roasters

Blenders, sealers, fillers, labelers

Inventory cash: leaves, herbs, botanicals

MOQs: minimum order quantities

How much money do you need to start a tea business?

For a Tea Industry startup, the cash need depends more on the model than the label: a 50-hectare growing setup shows $200,000 owned-land CAPEX or $72,000 first-year lease cash, before vendor equipment quotes and working capital. For tracking whether that spend is paying off, use What Is The Primary Measure Of Success For Your Tea Industry Business? and tie it to yield, product mix, and sales by channel.

Cost drivers

50 hectares sets the growing baseline

$200,000 owned-land CAPEX shown

$72,000 first-year lease cash shown

Vendor equipment quotes are still required

Model choices

Ecommerce avoids farm-land CAPEX

Private-label still needs inventory and packaging

Blending needs compliance and equipment quotes

Retail needs separate location cost quotes

Key Takeaways

Land CAPEX starts at $200,000 for 10 owned hectares.

Leased land burns $6,000 monthly, $72,000 yearly.

Year 1 processing and packaging run near 70% revenue.

Sales channels add 30% to 40% in fees.

Tea Industry Core Five Startup Costs

Facility, Site, And Buildout Startup Expense

Land Base

Start with the land math: 50 cultivated hectares in Year 1, with 10 owned hectares at $20,000 each, equals $200,000 in land CAPEX. The other 40 leased hectares at $150 per hectare per month run $6,000 monthly and $72,000 annually in cash before equipment.

Site Buildout

Classify permanent site work as CAPEX: farm improvements, food-safe processing space, blending room, storage, humidity control, shelving, utilities, tasting room fixtures, retail fixtures, and warehouse layout. Quote each item by square feet, fixture count, or install scope, then keep pre-opening deposits and rent in separate startup cash lines.

Lease Cash

Lease cash is not a building asset. Budget the $6,000 monthly lease as operating cash, and set aside any opening deposit or rent paid before launch as a separate startup expense. That split keeps the site budget clean and stops land access from getting mixed into fixed asset cost.

Buildout Control

Keep the buildout lean until harvest and sales paths are proven. The expensive mistakes are oversizing storage, adding too many retail fixtures, or locking in long rent before the processing line is ready. Tie every quote to output volume, then stage the tasting room and warehouse fit-out after the core food-safe rooms are set.

Initial Tea, Botanicals, And Inputs Startup Expense

Inventory First

Tea leaves, herbs, botanicals, flavorings, sample batches, planting material, freight, and spoilage are startup inventory or working capital, not capital spending (CAPEX). Plan Year 1 around 400% bulk black tea, 300% bulk green tea, 150% packaged premium black tea, 100% packaged specialty green tea, and 50% packaged herbal blends, then assume 60% yield loss, so only 40% stays usable.

How To Estimate

Price this with units × unit price for each input, plus minimum order quantities, freight, and storage loss. Separate sellable stock from sample batches and planting material if you grow tea. One clean rule: buy for the next sales window, not the full year.

Keep It Lean

Spoilage is the real cost leak. Tight humidity control, smaller replenishment orders, and fast receiving usually save more than chasing the cheapest quote. Packaged teas and herbal blends need the most cash because they carry extra handling and shelf risk, so keep those buys lean and timed to demand.

Cycle The Buys

Match each SKU to its 1, 2, or 3 sales cycle and buy only what you need before the next replenishment date. That keeps bulk leaf, packaged tea, and herbal blends from turning into dead stock, and it lowers age-related loss while protecting cash.

Sales Channel And Launch Readiness Startup Expense

Launch Math

For a tea startup, most sales-channel launch costs are cash expenses at first. Budget the website, product photography, sampling, launch marketing, and launch labor as expenses; only durable POS hardware or fixtures get capitalized. The big swing factor is channel mix: direct sales carry 40% Year 1 ecommerce transaction and shipping fees, while wholesale often carries 30% commissions.

Direct Setup

Build the direct channel budget from quotes for the site, photos, POS hardware, and customer acquisition. Add sampling units, farmers market setup, trade show setup, wholesale line sheets, and display materials. Use one-time setup quotes plus launch-month labor hours. This matters because Year 1 selling prices range from $800 for bulk black tea to $4,000 for packaged specialty green tea.

Lean Launch

Keep fixed spend light until repeat orders show up. Start with one sales lane, reuse photo assets across web and line sheets, and treat sampling as a measured test, not open-ended spend. The quick check is simple: if the channel can’t absorb 40% ecommerce fees or 30% wholesale commissions, the price mix is too thin.

Channel Fit

Channel choice should follow product value. Bulk tea can support simpler wholesale tools, while packaged specialty tea needs more launch cash for content, displays, and customer acquisition. Higher-priced packs can carry heavier launch spend, but lower-priced bulk tea needs tighter acquisition cost control. Don’t buy durable gear unless it cuts repeat setup cost.

Tea Processing And Packaging Equipment Startup Expense

Processing line quotes

The core spend is the tea processing line. For 50 hectares, six harvest months, and five product lines, build quote fields for dryers, withering racks, rollers, roasters, grinders, blenders, scales, filling equipment, sealers, labelers, storage bins, and quality assurance tools. Treat durable gear as CAPEX; consumables belong in startup inventory or operating expense. Add separate installation and freight lines.

Packaging needs

Packaged teas need more filling, sealing, labeling, and storage control than bulk tea, so the packaging side usually drives the most moving parts. Use one quote field per asset, then size the line for harvest peaks, not average days. One line can bottleneck all five products if packaging capacity is too small during the six-month crop window.

Split bulk and packaged flows.

Match capacity to peak harvests.

Quote QA tools separately.

Cost control

Keep the first buy tight: fund only the machines that move leaf from drying to finished pack, then add extras as sales prove out. Don’t bury labels, seals, pouches, and other consumables in equipment cost; they sit in inventory or operating expense. Ask for freight and install quotes up front so the cash need is clear before you order.

Buy for throughput, not looks.

Separate consumables from CAPEX.

Request freight and install quotes.

Budget fit

The right budget ties each asset to a quote, then adds installation and freight as its own line. That makes it easy to see whether the line can handle five product lines without slowing the six harvest months. If one machine can’t cover both bulk and packaged tea, it belongs on the deferred list.

Packaging, Labeling, And Compliance Startup Expense

Pack Costs

Packaging spend starts with pouches, tins, tea bags, cartons, labels, and setup for UPCs and ingredient panels. Treat these as startup inventory or operating expense, not CAPEX. In Year 1, the operating benchmark for processing and packaging materials is 70% of revenue, so the package mix should track product mix, not just unit count.

What It Covers

This cost covers packaging inputs and the print work behind them: pouches, tins, tea bags, cartons, labels, UPCs, ingredient statements, and allergen calls. Add separate quote lines for units × unit price, label setup, and first-run minimums. Packaged premium black tea, specialty green tea, and herbal blends need more cash than bulk tea.

Compliance Split

Protect cash by splitting required compliance from brand extras. You need state rule checks, US Food and Drug Administration food facility registration where applicable, and trademark work before launch. Organic or fair trade certification is optional and should sit outside core compliance. Use product count, filing fees, and attorney quotes to size this line.

Run Lean

The biggest waste is overbuying packaging before demand is clear. Start with the smallest safe run, then reorder against sell-through. Bulk black and bulk green tea need less packaging cash than retail-packed teas, so keep their inventory lean. One missed rule can force relabeling, so build in a review step before print.