Owner income$180k

Owner income$180kHow Much 5G Internet Provider Owners Can Make By Year 5: $176M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k  Net margin7.2%

Net margin7.2% Revenue for target pay$1.16M

Revenue for target pay$1.16M Business difficultyHard

Business difficultyHard

A 5G ISP owner’s income depends on salary, profit, financing, and how much cash stays in the network In this researched case, the owner-operator CEO role is budgeted at $180,000 per year, but Year 1 EBITDA is -$606,000, so distributions would not be prudent early The model reaches breakeven around Month 17, with EBITDA rising to $669,000 in Year 2 and $176 million in Year 5 Those figures are planning assumptions, not salary promises or tax advice

Owner income$180kNet margin7.2%Revenue for target pay$1.16MBusiness difficultyHardWant to test your own 5G ISP owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full 5G Internet Service Provider financial model?

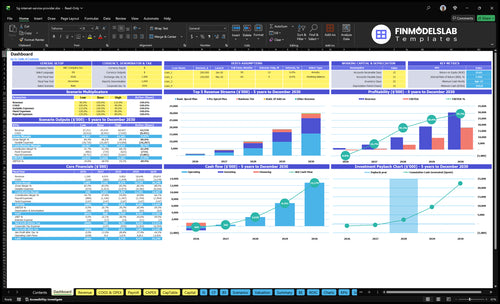

This dashboard shows subscriber assumptions, ARPU, churn, costs, and owner take-home; open the 5G Internet Service Provider Financial Model Template.

Owner-income model highlights

- EBITDA: -$606k to $176M

- Cash floor: -$426k Month16

- Payback: 31 months

Is a 5G internet service provider profitable?

Yes, a 5G Internet Service Provider can be profitable, but only after scale. One source case still shows -$606,000 EBITDA in Year 1, breakeven in Month 17, a -$426,000 cash low in Month 16, and 31-month payback, so early cash burn is the real issue. Profit improves as ARPU rises from $62.01 to $84.95 and variable cost load falls from 250% to 155%.

Profit drivers

- Raise ARPU to $84.95

- Cut variable cost load to 155%

- Reach breakeven in Month 17

- Target 31-month payback

Key risks

- -$606,000 Year 1 EBITDA

- -$426,000 minimum cash

- Churn can slow payback

- Weak density caps pricing

What 5G ISP operating costs reduce owner take-home?

Owner take-home gets squeezed first by wholesale network access fees, which are 120% of revenue in Year 1 and still 80% in Year 5, before overhead and growth spend hit. For launch cost context, see How Much Does It Cost To Open, Start, Launch Your 5G Internet Service Provider Business?. CPE (customer premises equipment) falls from 70% to 40%, while payment processing, software licenses, and referral bonuses drop from 60% to 35% of revenue.

Variable drag

- 120% wholesale fees in Year 1

- 80% wholesale fees in Year 5

- 70% to 40% CPE cost

- 60% to 35% processing, software, referrals

Fixed drag

- $12,250 monthly fixed overhead

- Payroll starts at $770,000 yearly

- Payroll reaches $1465 million

- Marketing rises from $500,000 to $55 million

How much can a 5G ISP owner make?

A 5G Internet Service Provider owner can model a $180,000 annual CEO salary, but profit is not the same as cash take-home; see What Is The Current Growth Rate For 5G Internet Service Provider's Customer Base? for customer-base growth context. Case EBITDA moves from -$606,000 in Year 1 to $669,000 in Year 2, then $3.858 million, $9.490 million, and $17.645 million in Years 3–5, but distributions are tight with -$426,000 minimum cash and a 31-month payback.

Owner Take-Home

- Start with $180,000 CEO salary

- Separate salary from business profit

- Delay distributions during cash strain

- Protect working capital first

Profit Ramp

- Year 1 EBITDA: -$606,000

- Year 2 EBITDA: $669,000

- Year 5 EBITDA: $17.645 million

- Payback target: 31 months

What drives 5G ISP owner income most?

1

HighSubscriber Base

More active subscribers spread the fixed payroll and office costs, which is the fastest way to lift take-home once the network is live.

2

$62-$85ARPU Mix

Mixing in more Pro, Business, and add-on lines lifts monthly revenue per user from about $62 in Year 1 to $85 in Year 5.

3

25%-15.5%Network Cost

Wholesale access, CPE, and software fees fall from about 25% to 15.5% of sales, and every point saved flows straight to profit.

4

$150-$100CAC Control

Cutting CAC from $150 to $100 makes the $500K first-year marketing budget go farther and shortens payback.

5

7%-4%Install Costs

Lower CPE cost eases the cash hit on each new line, which matters before the model reaches breakeven in Month 17.

6

$770K-$1.47MOverhead Discipline

Payroll and marketing rise fast, so reserve control matters when minimum cash dips to -$426K before payback.

5G Internet Service Provider Core Six Income Drivers

Subscriber Scale And Penetration

Subscriber Scale

More paying subscribers spread network, support, marketing, billing, and admin costs across recurring revenue. The model implies average subscribers rise from about 1,450 in Year 1 to about 28,700 in Year 5, so owner income improves only if each added account stays profitable after service and retention costs.

This driver includes active accounts, coverage density, capacity, support quality, and churn. More accounts lift take-home pay only when service holds up and replacement sales do not eat the margin.

Grow Net Active Subs

Track net active subscribers, not just new sign-ups. Use churn, support tickets, and capacity by coverage area to see whether growth is real or just replacement sales. If installs or service issues rise, the margin on each new account can disappear fast.

Push growth where density is strongest and support can keep up. One clean rule: add accounts only where the network still has room and the service team can protect retention.

- Measure active subs by area.

- Watch churn and ticket volume.

- Test capacity before scaling spend.

1

ARPU And Plan Mix

Higher-Tier ARPU

ARPU means average revenue per user. In this model, weighted ARPU rises from $6,201 in Year 1 to $8,495 in Year 5 as the plan mix shifts toward higher tiers. That lifts monthly revenue and can improve owner pay, but only if churn, install burden, and service promises stay under control.

Here’s the quick math: ARPU rises by $2,294, or about 37%. That helps cash flow and gross profit only when the added price is not swallowed by support, truck rolls, network costs, or retention spend. Higher tiers are good for income, but they need clean delivery.

Measure Mix, Not Just Sales

Track revenue by plan, not just total subscribers. Watch how many customers sit in each tier, how much each account actually pays after credits, and whether higher-tier users stay longer. If business-plan growth comes with more setup time or more tickets, the ARPU gain may not reach take-home income.

- Track tier mix every month.

- Test price before full rollout.

- Monitor churn by plan.

- Cap install and support costs.

Use churn, competition, install burden, and service obligations as guardrails. A cleaner mix works when the customer still gets fast, reliable service without extra handholding. If the richer plans need more support or faster fixes, price for that cost or the margin lift will leak out.

2

Network Cost Efficiency

Network Cost Efficiency

This driver is the gap between network spend and real demand. If wholesale network access, backhaul, site access, and capacity are sized to live traffic, the ISP keeps more of each subscription dollar. In the model, wholesale network access fees fall from 120% of revenue in Year 1 to 80% in Year 5, so the owner moves from cash burn toward usable gross margin.

The key inputs are subscribers, usage per customer, committed bandwidth, site count, and fixed network contracts. Here’s the quick math: underused capacity burns cash, but overloaded capacity raises support tickets and churn, which cuts take-home income. The best fit is dense areas with predictable demand, where fixed commitments can be spread over more recurring revenue.

Fit Network Spend to Demand

Separate fixed network costs from subscriber-driven costs. Track monthly revenue, committed capacity, peak utilization, and support tickets by site or zip. If utilization is low, delay new capacity adds; if it is too high, customers feel slow service and churn rises. The goal is simple: tie each network commit to real subscribers, not hoped-for growth.

- Watch revenue per committed link

- Test dense zip codes first

- Flag ticket spikes fast

- Cut idle commitments early

Price and expand where density is high enough to cover fixed access fees. In low-density areas, the same contract sits idle and drags cash flow. In dense areas, the fee base spreads faster, and owner pay improves sooner because recurring revenue covers a larger share of network commitments.

3

Churn And Customer Acquisition Cost

Churn And Customer Acquisition Cost

Churn is the share of subscribers you lose, and CAC is the cost to win one new customer. In a recurring-revenue ISP, lower churn protects monthly revenue and cuts replacement sales spend. Here, CAC improves from $150 in Year 1 to $100 in Year 5, while marketing budget rises from $500,000 to $55 million; spend alone does not fix weak retention.

Churn is not provided, so the model should keep it editable. If churn stays high, cash gets trapped in re-acquisition, breakeven moves out, and owner distributions get delayed. Judge local marketing by subscriber lifetime value, the total dollars one subscriber brings in over time, not just new installs.

Track churn against payback

Use one simple test: if acquisition costs $150 in Year 1 or $100 in Year 5, does that subscriber stay long enough to earn it back? The main inputs are new subscribers, churn rate, CAC, marketing spend, and subscriber lifetime value. If churn rises, replacement sales eat more cash and delay profit.

- Track churn monthly, not yearly.

- Compare CAC to lifetime value.

- Test local ads by payback period.

- Keep churn editable in forecasts.

At $500,000 of early marketing spend, small churn changes matter fast; by $55 million, waste gets expensive. Use service checks, cancel reviews, and retention offers to keep acquired subscribers from leaving before the business earns back the sales cost.

4

Equipment And Installation Economics

CPE And Install Cash Payback

CPE (customer premises equipment) and install spend hit cash payback fast. In Year 1, modeled CPE cost is 70% of revenue, then drops to 40% in Year 5. That gap matters more than headline growth, because a subscription business only pays the owner when installation cash outflows stop eating monthly margin.

The capex stack includes $250,000 for core network infrastructure, $80,000 for two vans, $50,000 for monitoring tools, and $35,000 for warehouse setup, or $415,000 total. Self-install, equipment financing, and fewer truck rolls shorten payback; heavy subsidies do the opposite and delay distributions.

Cut Install Cost Per Subscriber

Track install cost per new subscriber, truck rolls per install, and the share of customers who self-install. Here’s the quick math: if CPE stays near 70% of first-year revenue, there’s little cash left for owner pay; moving toward 40% in Year 5 creates room for distributions. The owner should price hardware support, not hide it.

Use financing terms and install policy to pro tect cash. Keep a tight watch on subsidy size, bad installs, and repeat visits, because each one pushes cash payback out. One clean rule helps: every avoided truck roll keeps more of the monthly subscription in the business instead of tied up in field work.

5

Overhead, Debt, And Reserves

Owner Cash After Overhead

EBITDA is not owner take-home here. For a 5G ISP, cash for the owner comes after payroll, support, insurance, billing systems, debt service, maintenance, and growth reserves. Fixed overhead is $12,250 a month, or $147,000 a year. The model also shows payroll rising from $770,000 to $1.465 million, so distributions only work when cash stays positive after those claims.

The model’s minimum cash hits -$426,000 before breakeven, so debt and reserve settings can wipe out owner pay even if EBITDA looks strong. Enter debt service and a reserve policy before estimating draws; reserve discipline protects uptime and keeps the business from paying the owner with cash the network still needs.

Set A Cash Reserve Floor

Track cash, not just EBITDA. Set a monthly reserve floor for network uptime, support load, and billing delays, then block distributions until that floor is funded. If debt payments or support costs rise, trim owner draws first.

- Enter debt service before any draw.

- Hold cash above -$426,000.

- Review overhead and payroll monthly.

6

Compare low, base, and high 5G ISP owner income scenarios

Owner income scenarios

Income shifts with subscriber density, ARPU (average revenue per user), churn, and CPE cost while fixed payroll stays high. The model runs from -$606k EBITDA in Year 1 to $17.645m in Year 5.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | Owner income stays under pressure because subscriber growth is slower and churn stays higher. | Owner income follows the modeled path as growth, pricing, and cost control line up with plan. | Owner income lifts faster when demand stays dense and acquisition cost falls. |

| Typical setup | The mix skews to Basic plans, CPE cost stays elevated, and overhead absorbs a bigger share of revenue. | ARPU rises from $6,201 in Year 1 to $8,495 in Year 5, the plan mix shifts toward Pro and Business, and EBITDA moves from -$606k in Year 1 to $669k in Year 2. | The mix shifts harder into Pro, Business, and add-ons, CAC drops from $150 in Year 1 to $100 in Year 5, and support load stays controlled. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Negative take-homeLower income | Mid-six-figure take-homeModeled income | Strong take-home upsideHigher income |

| Best fit | Use this to stress-test cash needs if adoption is slower than planned. | Use this as the budget case for planning, hiring, and lender talks. | Use this to test upside if unit economics stay tight at scale. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- 5G Internet Service Provider Porter's Five Forces Analysis

- 5G Internet Service Provider BCG Matrix

- 5G Internet Service Provider Business Model Canvas

- 7 Essential KPIs to Guide Your 5G Internet Service Provider Growth

- 5G Internet Service Provider Business Plan Template in Pre-Written Word

- How to Increase 5G Internet Service Provider Profitability in 7 Practical Strategies

- Calculating the Monthly Running Costs for a 5G Internet Service Provider

- 5G Internet Service Provider Startup Costs: $630K CAPEX Plan

- 5G Internet Service Provider Financial Model Template in Excel

- How To Start A 5G ISP: 6–12+ Month US Launch Plan

- How to Write a 5G Internet Service Provider Business Plan

- 5G Internet Service Provider Marketing Mix

- 5G Internet Service Provider Marketing Plan

- 5G Internet Service Provider Business Proposal

- 5G Internet Service Provider PESTEL Analysis

- 5G Internet Service Provider Pitch Deck Example Editable PPTX

- 5G Internet Service Provider Business SWOT Analysis

- 5G Internet Service Provider Value Proposition Canvas

Frequently Asked Questions

The source case budgets a $180,000 CEO salary, but distributions should wait until cash supports them Year 1 EBITDA is -$606,000, and minimum cash reaches -$426,000 in Month 16 EBITDA turns positive in Year 2 at $669,000, but debt, taxes, reserves, and network reinvestment still come first