Owner income$11.0M-$31.5M

Owner income$11.0M-$31.5MHow Much AAC Block Plant Owners Can Make On $1835M Year 1 Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$11.0M-$31.5M  Net margin59.7%-66.1%

Net margin59.7%-66.1% Revenue for target pay$18.4M

Revenue for target pay$18.4M Business difficultyHard

Business difficultyHard

You’re planning an autoclaved aerated concrete (AAC) plant where income is modeled from five-year researched assumptions, including $1835M first-year revenue growing to $4771M This is not a guaranteed salary, tax advice, or automatic distribution it estimates revenue, gross margin, operating costs, owner pay, reinvestment, reserves, and scenario-based take-home

Owner income$11.0M-$31.5MNet margin59.7%-66.1%Revenue for target pay$18.4MBusiness difficultyHardWant to test your AAC block plant profit?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, debt, reserves, and operating discipline.

Want to see the income model?

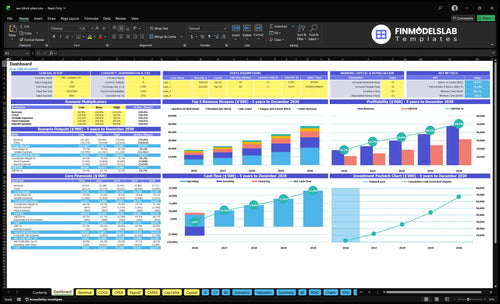

In this screenshot, AAC Block Manufacturing Plant Financial Model Template shows revenue, margin, costs, reserves, and owner-income assumptions—open it.

Owner-income model highlights

- Dashboard and assumptions

- Income statement, cash flow

- Scenario analysis included

- Capacity, pricing, product mix

- COGS, freight, commissions

- Overhead, payroll, debt

- Reserves, distributions, owner take-home

- Revenue: $1.835M, $2.994M, $4.771M

- Planning only, not promised

How much can an AAC block plant owner make?

An AAC Block Manufacturing Plant owner should not treat revenue or listed profit as take-home pay; in the researched case, Year 1 shows $1.835M revenue, 77.0% gross margin, and about $1.13M listed operating profit before owner pay, debt, taxes, reserves, and unprovided labor. By Year 5, the model reaches $4.771M revenue, 79.1% gross margin, and about $3.24M listed operating profit, so the real owner income depends on how much cash is paid as salary, distributed, or reinvested; see How Much To Start AAC Block Manufacturing Plant? for startup cost context.

Profit is not pay

- Year 1 revenue: $1.835M

- Year 1 gross margin: 77.0%

- Listed operating profit: about $1.13M

- Owner pay still deducted separately

Cash split

- Year 5 revenue: $4.771M

- Year 5 gross margin: 79.1%

- Listed operating profit: about $3.24M

- Separate salary, distributions, reinvestment

How much revenue does an AAC block plant need to pay the owner?

An AAC Block Manufacturing Plant does not have one universal revenue target to pay the owner; using the listed 68.5% contribution rate, $960k of fixed overhead plus $325k of payroll means break-even before owner pay, debt, reserves, taxes, and unprovided labor is about $1.88M in revenue. At that same margin, every $100k of owner draw needs about $146k of extra revenue.

Break-even math

- 68.5% contribution rate

- $960k fixed overhead

- $325k payroll

- $1.88M break-even revenue

Owner pay impact

- $100k owner draw

- $146k extra revenue needed

- Before debt and reserves

- Before taxes and unprovided labor

What AAC block manufacturing gross margin should owners watch?

Owners should watch gross margin every month at the AAC Block Manufacturing Plant, because small changes in cement, lime, gypsum, aluminum expansion paste, labor, packaging, energy, testing, insurance, waste, and maintenance can move it fast; see How Much To Start AAC Block Manufacturing Plant?. The model shows Standard AAC Block at $0.85 listed unit COGS plus 30% revenue-based production costs, and Reinforced Wall Panel at $17.55 plus 40%. Expected gross margin ranges from 77.0% in Year 1 to 79.1% in Year 5, but those are assumptions, not fixed industry rules.

Cost Drivers

- Cement and lime matter most

- Gypsum and paste add volatility

- Labor and energy hit margin fast

- Waste and maintenance erode profit

Margin Watch

- $0.85 unit COGS for Standard AAC Block

- 30% revenue-based production costs

- $17.55 unit COGS for Wall Panel

- 40% revenue-based production costs

Want the six AAC block plant income drivers?

1

$18.35M-$47.71MCapacity Utilization

Higher uptime and sell-through spread fixed plant costs over more output, so owner take-home rises faster as revenue climbs from Year 1 to Year 5.

2

$9.5-$11.8Price Mix

A richer mix of lintels and wall panels lifts weighted selling price, moving average revenue per unit from about $9.5 to $11.8.

3

77.0%-79.1%Gross Margin

Gross margin stays around 77.0% to 79.1%, and every point saved on sand, energy, and testing drops straight to operating profit.

4

6-13 FTELabor Load

Staffing rises from 6 to 13 FTE, so keeping output ahead of headcount protects margin and keeps more cash for the owner.

5

8.5%-7.7%Freight Drag

Local demand cuts the freight radius and the 2.5% commission bite, so more of each sale reaches the bank account.

6

-$335KCash Trough

The model dips to -$335K in Month 6 before payback in Month 9, so debt-service pressure and early cash discipline decide how much profit turns into take-home.

AAC Block Manufacturing Plant Core Six Income Drivers

Capacity Utilization And Sell-Through

Capacity Utilization and Sell-Through

Higher plant utilization spreads fixed costs across more saleable output, but the gain only counts when production is sold and collected. Output grows from 12M Standard AAC Blocks in Year 1 to 25M in Year 5, plus lintels, panels, U-block shells, and tongue-and-groove blocks. If the plant makes inventory faster than builders, contractors, and distributors buy it, cash gets stuck on the floor.

That hits owner income fast: more unsold units raise carrying costs and delay cash for debt service, payroll, and owner draws. The best case is high utilization with fast sell-through; the weak case is high production with slow collections. Sold units pay the bills.

Track Output, Orders, and Cash

Measure units produced, units sold, and cash collected each month. A simple sell-through check is sold units ÷ produced units. Track it by product line, because standard blocks, panels, and specialty units can move at different speeds and change margin and cash flow in different ways.

- Match production to booked orders

- Watch ending inventory weekly

- Track days inventory on hand

- Delay runs when stock builds

If production outruns demand, pause extra shifts and push the sales channel first. The owner keeps more cash when the plant turns output into collected revenue, not just finished goods.

1

Selling Price And Product Mix

Selling Price and Product Mix

Revenue per unit comes from price and mix, so this driver sets how much cash each AAC sale can throw off. In Year 1, the range runs from $450 for a Standard AAC Block to $8,500 for a Reinforced Wall Panel. If the mix shifts toward panels, top-line dollars rise fast, but handling, damage risk, and unit cost also rise.

By Year 5, prices move to $507 and $9,568, about 12.7% and 12.6% higher. That helps owner pay only if discounts stay tight and the customer mix supports premium pricing. Mix drives cash more than the price sheet does.

Track Realized Price by SKU

Measure net price, not list price. You need unit volume by product, contract price, discount rate, and the share of sales coming from blocks versus panels. If a high-price panel sale needs extra freight or handling, the owner’s take-home income can drop even when revenue looks strong.

- Track net price by SKU

- Watch discount leakage weekly

- Forecast mix by customer type

- Protect premium pricing on panels

Test whether contractors buy more at a small discount or hold volume at full price. Use that data to set contract terms, limit off-invoice discounts, and steer more sales toward products that keep gross margin strong after unit cost and handling. Price discipline pays owner draws.

2

Raw Material And Energy Costs

Raw Material and Energy Costs

This driver is the gap between selling price and what it takes to make each AAC unit. The base cost is $0.85 per Standard AAC Block plus 30% of revenue in production costs; a Reinforced Wall Panel starts at $17.55 per unit plus 40%. When cement, lime, gypsum, aluminum paste, steel mesh, or steam costs rise, gross margin shrinks fast, and the owner has less cash for pay.

Energy is a clear swing factor: the model uses a 12% surcharge for most products and 15% for panels. That means a cleaner mix, better yield, and tighter batching matter. If input inflation outruns price resets, accounting profit can look fine on paper but distributable cash drops, especially on high-cost panel orders.

Track Input Cost per Saleable Unit

Measure raw material cost per saleable unit, not just per batch. Split cement, lime, gypsum, aluminum paste, steel mesh, and steam so you can see where margin leaks start. One clean rule: every 1% cost increase on a high-volume line hits owner income more than a small gain on a low-volume line.

Test price resets and waste cuts by product. Use sensitivity checks on the 12% and 15% energy loads, plus the 30% and 40% production cost layers, before you lock annual contracts. If a panel order needs extra steam or rework, price it to protect gross margin; don’t let busy volume turn into weak cash flow.

3

Plant Uptime And Labor Efficiency

Plant Uptime And Labor Efficiency

Plant uptime is the share of scheduled hours that become saleable AAC blocks and panels. When autoclaves, cutting, or handling stop, revenue drops fast because fixed labor keeps running. Direct labor is already in COGS, at $0.12 per Standard AAC Block and $2.30 per Reinforced Wall Panel, so yield loss hits gross margin and owner draw.

Here’s the quick math: plant manager payroll alone is $135,000 a year, or about $11,250/month, before other staff. So downtime, rejects, and poor cutting yield do more than delay shipments; they raise cost per good unit and can trap cash in unfinished or unsold inventory even when demand is strong.

Track uptime where cash is lost

Measure scheduled hours, actual good output, autoclave queue time, reject rate, and cutting yield by line and shift. If one step starves the next, the plant is not really running at full capacity. The owner should watch good units per labor hour and labor cost per saleable unit, not just total production.

- Track downtime by cause.

- Log rejects before packaging.

- Compare shifts weekly.

- Set a yield target by product.

Use the data to cut bottlenecks, match staffing to demand, and protect cash flow. If the plant cannot turn labor into shipped product, payroll becomes a margin leak instead of a growth lever.

4

Customer Demand And Delivery Cost

Customer Demand And Freight Cost

For AAC blocks, demand is not just units sold; it’s how fast repeat builders, contractors, and masonry distributors can take delivery. In the model, outbound logistics and freight are 60% of Year 1 revenue and ease to 52% by Year 5, while sales commissions stay at 25%. That means selling can still leave very little c ash if routes are long or sell-through is slow.

The main inputs are orders, repeat-customer share, delivery distance, and unsold inventory. Long freight routes and stock that sits too long cut distributable cash, even when top-line revenue looks fine.

Trim Miles, Not Demand

Track freight cost as a percent of revenue by customer and route. Here’s the quick math: 60% freight plus 25% commissions means 85% of revenue is already spoken for before plant overhead, so route density matters as much as sales volume. Push the accounts that reorder and cluster by job site.

Watch these inputs each month:

- Repeat orders by account

- Freight cost per mile

- Inventory days on hand

- Quote-to-ship conversion

5

Debt Service And Cash Reserves

Debt Service And Cash Reserves

This driver is the cash left after loan principal, interest, and reserve transfers. In this model, accounting profit is not the same as money the owner can take home. If Year 1 operating profit before owner pay, debt, taxes, reserves, and unprovided labor is $113M, the owner’s draw still depends on debt terms, reserve policy, and working capital needs.

By Year 5, operating profit before owner pay rises to $324M, but cash can still stay in the business for equipment maintenance, inventory, loan payments, and expansion. The owner only gets paid what remains after those claims. One clean rule: profit on paper is not distributable cash until the debt schedule and reserve plan say it is.

- Loan principal and interest

- Payment timing and maturity

- Reserve target and capex

- Inventory and receivable days

- Maintenance and expansion cash

Track Cash Before Owner Pay

Track cash after debt service, reserve balance, and months of coverage. Inputs include loan principal, interest rate, payment schedule, capex, maintenance spend, inventory days, and receivable days. If debt service rises faster than cash generation, owner pay gets squeezed even when profit looks strong.

Use a reserve floor tied to one repair cycle and one payment cycle, then only distribute cash above that floor. Separate operating cash, debt-payment cash, and expansion cash so you do not pay out funds needed for autoclave work, raw material buys, or shipment timing.

6

Compare lean, base, and high AAC block plant income cases

Owner income scenarios

Revenue scales fast here, but owner take-home still swings with freight, labor, and fixed overhead. These cases show profit before owner pay across lean, base, and strong operating levels.

| Scenario | Lean CaseLean case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the lower earnings path, using Year 1 scale and the first operating cost stack. | This is the modeled middle path, using Year 3 scale and a steadier operating mix. | This is the stronger earnings path, using Year 5 scale and the highest modeled output. |

| Typical setup | Year 1 revenue is $18.35M, with about 77% gross margin and the opening labor build. | Year 3 revenue reaches $29.94M, with about 78% gross margin and a larger staffing base as throughput rises. | Year 5 revenue reaches $47.71M, with about 79% gross margin and a heavier sales and plant support team. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.13MLean case | $1.95MBase case | $3.24MHigh case |

| Best fit | Use this when you want a cautious opening-year view and a stress test for launch-year cash flow. | Use this as the planning case for budget work, lender talks, and mid-cycle operating targets. | Use this to test upside, capacity pressure, and whether the plant can hold margin at full run rate. |

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- AAC Block Manufacturing Plant Porter's Five Forces Analysis

- AAC Block Manufacturing Plant BCG Matrix

- AAC Block Manufacturing Plant Business Model Canvas

- What Are The 5 KPIs For AAC Block Manufacturing Plant Business?

- AAC Block Manufacturing Plant Business Plan Template in Pre-Written Word

- How Increase AAC Block Manufacturing Plant Profitability?

- What Does It Cost To Run AAC Block Plant?

- AAC Block Plant Startup Costs: $25M Autoclaves To Opening

- AAC Block Manufacturing Plant Financial Model Template in Excel

- How To Open An AAC Block Manufacturing Plant In 9 To 18 Months

- How To Write AAC Block Manufacturing Plant Business Plan?

- AAC Block Manufacturing Plant Marketing Mix

- AAC Block Manufacturing Plant Marketing Plan

- AAC Block Manufacturing Plant Business Proposal

- AAC Block Manufacturing Plant PESTEL Analysis

- AAC Block Manufacturing Plant Pitch Deck Example Editable PPTX

- AAC Block Manufacturing Plant Business SWOT Analysis

- AAC Block Manufacturing Plant Value Proposition Canvas

Frequently Asked Questions

It can show strong operating profit under the supplied assumptions, but owner cash is lower after debt, taxes, reserves, and reinvestment The model shows $1835M in Year 1 revenue, about 770% gross margin, and roughly $113M listed operating profit before those deductions and unprovided labor items