Owner income$772k to $15.1M

Owner income$772k to $15.1MAcrobatics And Tumbling Owner Income: $772k Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$772k to $15.1M  Net margin55.5% to 83.4%

Net margin55.5% to 83.4% Revenue for target pay$1.39M

Revenue for target pay$1.39M Business difficultyMedium

Business difficultyMedium

Key Takeaways

- Enrollment drives cash and covers fixed overhead.

- Better mix raises revenue without adding rent.

- Fuller schedules lift margin, but safety matters.

- Add-ons help only when they don't crowd classes.

Owner income$772k to $15.1MNet margin55.5% to 83.4%Revenue for target pay$1.39MBusiness difficultyMediumWant to test your own tumbling gym income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. The model also shows a Month 1 breakeven and about $884k minimum cash need at launch.

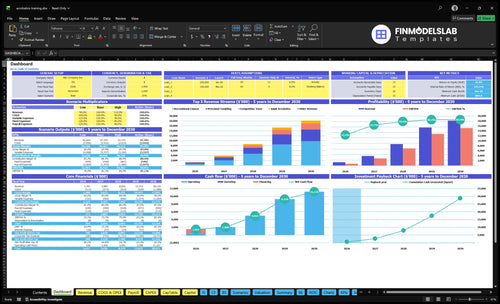

How does the model turn enrollment into owner income?

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions. Open the Acrobatics and Tumbling Training Financial Model Template.

Owner-income model highlights

- Dashboard and income statement

- Enrollment, pricing, payroll

- Scenario and owner pay

How many students does a tumbling gym need to be profitable?

Acrobatics and Tumbling Training can be profitable without a single fixed student count, because the model depends on fill rate, tuition mix, and collections timing. The core case uses 195 program places in Year 1 at 45% occupancy, then 460 places by Year 5 at 90% occupancy; with tuition from $85 to $250 in Year 1 and $105 to $290 in Year 5, it can reach breakeven in Month 1 if the class mix holds.

Year 1 setup

- 195 places in Year 1

- 45% occupancy in Year 1

- $85 to $250 tuition range

- $9,150 monthly facility overhead

Profit drivers

- $212k Year 1 payroll

- 460 places by Year 5

- 90% occupancy by Year 5

- Team pricing lifts athlete revenue

Can you make a living owning a tumbling gym?

Yes, you can make a living owning an Acrobatics and Tumbling Training gym in this case if enrollment, pricing, and class use hold; see How Increase Profits For Acrobatics And Tumbling Training? for the profit levers. Year 1 EBITDA, meaning cash profit before interest, taxes, depreciation, and amortization, is $772k, but owner draw still comes after taxes, debt, reserves, and reinvestment.

Profit Case

- $772k Year 1 EBITDA

- $65k gym director salary included

- $112k coach payroll included

- $35k front desk role included

Owner Reality

- $1.098m annual facility overhead

- Owner-operated may replace director cost

- Manager-led keeps director as real cost

- Below 45% occupancy pressures income fast

What profit margin can an acrobatics training business make?

Acrobatics and Tumbling Training can look very profitable on paper, but the number that matters is owner income after payroll, rent, and staffing. If you’re mapping the setup, How Do I Launch Acrobatics And Tumbling Training Business? fits right before pricing and staffing decisions. The model shows EBITDA margin at about 555% in Year 1 and about 834% in Year 5, but low class utilization and extra staff can still erase the owner’s draw. Year 1 rev-based COGS and variable costs are 19%, and fixed facility costs are $9,150 per month.

Owner take-home

- Watch owner income, not just EBITDA.

- Year 1 EBITDA margin: 555%.

- Year 5 EBITDA margin: 834%.

- Low utilization cuts the draw fast.

Main cost stack

- Year 1 variable costs: 19%.

- Fixed facility costs: $9,150 monthly.

- Big costs: payroll, rent, insurance, utilities.

- Also: marketing, fees, apparel, inspections.

Want the six main owner-income drivers?

1

195-460Enrollment

More students spread rent and coach pay across more tuition, so take-home rises fast.

2

$85-$290Tuition Mix

Higher-priced team and adult classes lift revenue per slot without adding much space.

3

45%-90%Schedule Use

Filling more of the 22 billable days turns the same floor time into more cash.

4

$212K-$423KCoach Pay

Keeping coach staffing close to demand protects EBITDA as class counts grow.

5

$9.15K/moFixed Costs

Rent and other fixed bills stay flat, so each extra class carries more profit.

6

$1.2K-$3.5KAdd-ons

Birthday parties add cash with limited extra labor, which lifts owner income.

Acrobatics and Tumbling Training Core Six Income Drivers

Active Student Enrollment

Active Enrollment

When active enrollment stays full, tuition turns into predictable monthly cash that covers rent, payroll, and insurance. This model grows from 195 program places in Year 1 to 460 in Year 5, with occupancy moving from 45% to 90%. More paying athletes also spread $9,150 in monthly facility overhead across a larger base, which helps protect owner draw.

Here’s the quick math: more enrolled students means more recurring collections without adding a new facility. What this hides is churn, weak trial conversion, and poor schedule fit. If families do not renew or classes do not match after-school timing, occupancy slips and fixed costs stay the same. One empty spot is lost monthly revenue until it is filled.

Track Fill Rate Weekly

Measure occupancy, trial-to-member conversion, and 30-day churn by age group and class time. If a class runs below target fill, fix the schedule, coach coverage, or offer before adding more spots. The goal is simple: more paid spots that renew, so the same facility produces more cash for owner pay.

- Watch fill rate by class.

- Test trial times with families.

- Protect peak-hour schedule fit.

1

Tuition Pricing And Program Mix

Tuition Mix Drives Revenue per Athlete

Tuition pricing changes average revenue per athlete fast. In Year 1, tuition ranges from $85 for preschool to $250 for competitive team; by Year 5, it rises to $105 to $290. That extra $20 to $40 per athlete lifts monthly revenue without adding rent, so more of each dollar can flow to profit and owner draw.

Higher-priced competitive team and adult acrobatics can raise revenue when coach time is priced correctly. What this includes: class tuition, camps, clinics, and privates. What can block it: local market limits, skill level, facility positioning, and affordability. If the mix is off, you get more work without enough cash back.

Track Price by Program and Coach Time

Measure revenue per athlete, fill rate by program, and coach hours per dollar collected. Test whether camps, clinics, and privates lift average monthly revenue per family without dragging down margin. If a program needs more coach time, price it so the extra labor is covered, not absorbed by the core class schedule.

- Track tuition by program weekly.

- Price coach-heavy classes higher.

- Use add-ons in open slots.

- Watch affordability by age band.

2

Class Capacity And Schedule Utilization

Class Capacity And Schedule Utilization

Fuller classes matter because rent, software, insurance, cleaning, and inspections are mostly fixed. If occupancy moves from 45% in Year 1 to 90% in Year 5, the same facility cost supports far more paid spots, so EBITDA before taxes and reserves improves without a matching rise in overhead.

Here’s the quick math: more filled spots spread the $9,150 monthly facility overhead across more athletes. The risk is pushing too hard on density; unsafe athlete-to-coach ratios, crowded stations, and weaker instruction can hurt retention and reduce take-home income.

Track Fill Rate By Class

Measure fill rate by class, waitlists, coach coverage, and peak-hour utilization every week. Those four inputs show where empty slots sit, where demand is strongest, and where you can add classes without hurting quality.

Use the schedule to protect ratios first, then push density. A one-line rule helps: fill the class, not the floor. If a class looks full but stations are crowded, the schedule is already hurting both safety and margin.

- Track filled spots by class

- Watch waitlists by age group

- Match coach coverage to demand

- Test peak-hour class times

3

Coach Payroll And Labor Leverage

Coach Payroll and Labor Leverage

Labor leverage means getting more class revenue from each coaching dollar. Year 1 payroll totals $212,000 a year from a $65k gym director, $48k head coach, two $32k assistant coaches, and a $35k front desk coordinator, or about $17,667 a month. If enrollment and class fill do not cover that base, owner take-home gets squeezed fast.

By Year 5, staffing grows to 2 head coaches, 6 assistant coaches, and 2 front desk coordinators. That only helps if paid spots, safe ratios, and schedule fill rise with it. The owner’s teaching time is a separate cost from owner draw. If the owner is on the floor too much, burnout can hit service quality before the P&L shows the damage.

Track Hours Before You Add Headcount

Watch payroll as a share of tuition revenue, coach hours per class, fill rate, and owner teaching hours. Here’s the quick math: if a coach hour does not bring in enough paid spots to cover that wage, it is a margin leak. Add staff only when enrollment and class density make the extra payroll pay back.

Separate owner labor replacement cost from actual owner draw. Price the owner’s teaching hours at the wage it would take to replace them, then compare that to profit after payroll. That keeps cash flow honest and helps protect margins and safety when schedules get tight.

4

Facility And Fixed-Cost Control

Facility Cost Control

Fixed costs set the break-even floor before the first class is sold. Monthly overhead is $9,150 made up of $6,500 rent, $1,200 utilities and internet, $450 liability insurance, $250 software, $600 cleaning, and $150 equipment inspections. One clean rule: every dollar of overhead saved lowers the enrollment needed for owner pay.

The $87,000 equipment capex for the spring floor, tumble track, mats, bars, vault, foam pit, furniture, and signage matters because cash is tied up before tuition starts coming in. Safety gear and insurance are not optional cuts. What this hides: if fixed costs creep up, the business needs more filled spots just to stand still.

Track Overhead Monthly

Use a simple break-even check: $9,150 ÷ monthly contribution per student. That tells you how many enrolled athletes the gym needs before owner draw starts. If rent, cleaning, software, or utilities rise, update the model right away so you don’t overpay yourself.

- Track each fixed line monthly.

- Flag any cost above budget.

- Review utility and cleaning bills.

- Keep inspections on schedule.

- Protect safety spending first.

5

High-Margin Add-On Programs

High-Margin Add-Ons

Private lessons,

Here’s the catch: add-ons only help if they do not crowd out recurring tuition. If they trigger coach overtime, weekend fatigue, insurance exposure, or schedule conflicts, the margin can shrink fast. With fixed overhead already at $9,150 per month, the goal is simple: sell extra hours that would otherwise sit idle, not replace higher-value class revenue.

Measure Add-On Yield

Track add-on revenue by type, hour, and coach load. Compare each event’s cash collected against labor hours, setup time, and any overtime. If a private lesson or party needs premium staffing, price it so the extra labor still leaves profit. One clean rule: if the add-on weakens class fill rate, it is not high-margin.

Watch three inputs every month: add-on revenue, coach hours, and core-class occupancy. Keep the calendar tight so parties, camps, and clinics sit around unused capacity, not prime class slots. Birthday parties moving from $1,200 to $3,500 per month can help owner pay, but only when the schedule protects recurring tuition.

- Track revenue per add-on type.

- Flag every overtime hour.

- Protect class occupancy first.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with occupancy, class volume, and pricing. Year 1, Year 3, and Year 5 show how payroll and fixed overhead absorb cash before any owner draw.

| Scenario | Low CaseEarly ramp-up | Base CaseScaled utilization | High CaseMature schedule |

|---|---|---|---|

| Launch model | This is the early ramp-up case, with 45% occupancy and the lowest modeled owner take-home proxy. | This is the scaled utilization case, with 75% occupancy and a much stronger modeled earnings base. | This is the mature schedule case, with 90% occupancy and the strongest modeled take-home proxy. |

| Typical setup | Year 1-style setup with $1.391M revenue, $772k EBITDA, $212k payroll, 19% rev-based COGS and variable costs, and $9,150 monthly facility overhead. | Year 3-style setup with $8.654M revenue, $6.914M EBITDA, and $3.415M payroll at 75% occupancy. | Year 5-style setup with $18.129M revenue, $15.112M EBITDA, and $423k payroll at 90% occupancy. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $772kLean case | $6.914MBase case | $15.112MHigh case |

| Best fit | Use this to stress-test the opening month and early ramp when fill rates stay weak. | Use this as the planning case for a stable operating year with solid class fill and steady demand. | Use this to test upside when the schedule is full and fixed overhead is well absorbed. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

Related Products

- Acrobatics and Tumbling Training Porter's Five Forces Analysis

- Acrobatics and Tumbling Training BCG Matrix

- Acrobatics and Tumbling Training Business Model Canvas

- What Are The 5 KPI Metrics For Acrobatics And Tumbling Training Business?

- Acrobatics And Tumbling Business Plan Template in Pre-Written Word

- How Increase Profits For Acrobatics And Tumbling Training?

- What Are The Operating Costs Of Acrobatics And Tumbling Training?

- Acrobatics And Tumbling Startup Costs: $87k CAPEX, $884k Cash Plan

- Acrobatics and Tumbling Training Financial Model Template in Excel

- How To Open An Acrobatics And Tumbling Training Business In 3–6 Months

- How Do I Write A Business Plan For Acrobatics And Tumbling Training?

- Acrobatics and Tumbling Training Marketing Mix

- Acrobatics and Tumbling Training Marketing Plan

- Acrobatics and Tumbling Training Business Proposal

- Acrobatics and Tumbling Training PESTEL Analysis

- Acrobatics and Tumbling Training Pitch Deck Example Editable PPTX

- Acrobatics and Tumbling Training Business SWOT Analysis

- Acrobatics and Tumbling Training Value Proposition Canvas

Frequently Asked Questions

In the researched case, owner take-home capacity is best viewed through EBITDA, not a fixed salary EBITDA is $772k in Year 1 on $1391M revenue and reaches $15112M by Year 5 on $18129M revenue Actual draw depends on taxes, reserves, debt, reinvestment, and whether the owner fills the $65k director role