Owner income$90k to $5.8M

Owner income$90k to $5.8MHow Much Can a Sports Analytics Consulting Owner Make at $56M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$90k to $5.8M  Net margin-10% to 62%

Net margin-10% to 62% Revenue for target pay$289k

Revenue for target pay$289k Business difficultyHard

Business difficultyHard

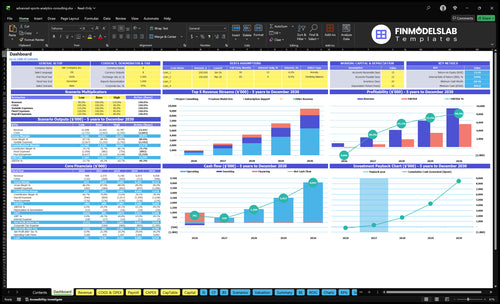

A sports analytics consulting owner in this model is paid a $180,000 annual CEO / lead consultant salary, but true owner income depends on whether the firm also has profit to distribute The researched assumptions show about $877,000 revenue in Year 1 with -$90,000 EBITDA, so the salary needs funding during ramp-up By Year 2, revenue rises to about $22 million and EBITDA reaches $696,000 before taxes, reserves, capex, and debt By Year 5, the model reaches about $90 million revenue and $56 million EBITDA, but that is a planning scenario, not guaranteed take-home pay

Owner income$90k to $5.8MNet margin-10% to 62%Revenue for target pay$289kBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, labor cost, fixed overhead, marketing, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Sports Analytics Consulting model?

The dashboard connects revenue, margin, costs, reserves, and owner take-home assumptions in the Sports Analytics Consulting Financial Model Template; open the model.

Owner-income model highlights

- Owner salary stays separate

- Revenue ramps $877k to $90M

- Cash bottoms at $644k

How much can a sports analytics consulting founder take home?

A Sports Analytics Consulting founder can take home $180k in Year 1 salary, but that isn’t profit because Year 1 EBITDA is -$90k; for the main success driver, see What Is The Most Critical Measure Of Success For Your Sports Analytics Consulting Business?. By Year 2, EBITDA reaches $696k before taxes and reserves, creating possible distribution capacity if cash isn’t retained for hiring or growth.

Founder cash

- $180k Year 1 CEO salary

- -$90k Year 1 EBITDA

- Salary is not self-funded profit

- $696k Year 2 EBITDA pre-tax

What changes it

- Client count and contract pricing

- Delivery workload per account

- Cash kept for hiring

- Year 5: $5.602M EBITDA on about $90M revenue

How much revenue does a sports analytics consulting business need to pay the owner?

If the owner wants a $180k salary and roughly zero EBITDA in Year 1, Sports Analytics Consulting needs about $10.0M in revenue, using about $7.214M of payroll, fixed overhead, and marketing at a 72% contribution margin. Actual Year 1 revenue is only $877k, so the business is still far below that pay level. Taxes and owner distributions are separate; Year 2 still shows about -$90k EBITDA, and the zero-EBITDA run rate is about $1.26M at a 74% margin.

Year 1 pay target

- $180k owner salary is the goal.

- 72% contribution margin drives the math.

- $7.214M cost base implies about $10.0M revenue.

- $877k actual revenue falls well short.

What the gap means

- Year 2 EBITDA is about -$90k.

- Zero-EBITDA revenue is about $1.26M.

- 74% margin improves the payback math.

- Taxes and distributions stay separate.

How do sports analytics consulting margins affect owner income?

In Sports Analytics Consulting, owner income is mostly a margin story after volume is set. If you’re sizing launch spend, see What Is The Estimated Cost To Open And Launch Your Sports Analytics Consulting Business?; Year 1 delivery costs run 28% of revenue, leaving 72% before payroll and overhead, and by Year 5 they drop to 20%, so each 1-point cost change can move EBITDA by about $22k at $22M revenue and about $90k at $90M.

Margin sensitivity

- Year 1 delivery costs: 28%

- 72% left before overhead

- Year 5 delivery costs: 20%

- Each cost point hits EBITDA fast

Owner income levers

- Contractors add capacity

- But contractors cut gross margin

- Data and software protect quality

- Price them into fees or take-home falls

What changes owner income most?

1

$275-$415Hourly Rate

Higher rates lift revenue on the same billable hours, and that drops straight to owner take-home.

2

20-120hBillable Hours

More billed hours per service spread the team across more revenue, so margin improves fast.

3

$495K-$1.26MDelivery Labor

Staff cost climbs hard as FTEs scale, so labor discipline matters as much as sales.

4

15%-30%Custom Mix

More custom model work pushes hours into the highest-rate work, but delivery has to stay tight.

5

$14.7K/moMonthly Overhead

Rent, admin, legal, insurance, utilities, content, and training keep breakeven close until volume builds.

6

10%-14%Data Costs

Premium data and cloud spend run about 10% to 14% of revenue, so vendor control protects margin.

Sports Analytics Consulting Core Six Income Drivers

Pricing And Engagement Model

Pricing and engagement mix

This driver is the fee mix across $55k subscription support, $13k project consulting, and $30k custom model work in Year 1. Retainers smooth cash flow, projects create spikes, and custom models lift average fee but use more senior time. If scope drifts, owner pay gets squeezed even when revenue looks better.

By Year 5, billings rise to $945k, $219k, and $498k. That higher recurring pricing can improve utilization and take-home income, but only if delivery hours stay tied to the contract. One clean rule: price the work you can repeat, then protect the scope.

Control the mix, not just the rate

Track retained revenue, project revenue, custom-model hours, and realized rate on every client. Estimate each deal from these inputs:

- Clients signed

- Hours sold and used

- Rates by service type

- Scope changes and add-ons

When recurring work covers more of the base load, cash gets steadier and the owner can draw more reliably. When custom model work expands without tighter scope control, senior labor gets tied up fast and profit falls.

1

Client Mix

Client Mix

Client mix changes fee size, cash timing, and workload. In this business, professional teams, college athletics departments, leagues, and other sports organizations buy different blends of support, project work, and custom model development, so the same sales effort can produce very different revenue and margin. A shift in service attachment from 40% to 85% for subscription support, 70% to 50% for project consulting, and 15% to 30% for custom model development changes both revenue quality and delivery load.

Procurement cycles and season timing can push cash receipts later, even when booked revenue looks strong. More retained and custom work usually improves predictability and owner pay, but it also means tighter delivery planning, because custom models use more senior time and support work adds ongoing reporting and client contact.

Track Mix by Client Type

Measure mix by client type and by service line: support, project consulting, and custom models. The key inputs are client count, attachment rate, average fee, renewal timing, and days to collect. If support moves from 40% to 85%, revenue gets steadier; if project work dominates, cash can spike and stall.

- Track revenue by client segment.

- Forecast cash by season and procurement.

- Price custom work for senior time.

- Limit scope creep in project work.

What this hides: a stronger mix can raise gross margin, but only if delivery capacity is planned first. If retained clients expand faster than staffing or model QA, owner pay gets squeezed by overtime, rework, and delayed billing. One clean rule: book the work, then staff the work.

2

Utilization And Billable Capacity

Billable Capacity

Utilization is the share of staff time that gets billed, not just the hours people work. In sports analytics consulting, sales, research, client meetings, reporting, admin, and model QA all eat into it, so not every available hour turns into revenue. The model’s service load uses 20 to 30 hours for support, 40 to 60 hours for projects, and 80 to 120 hours for custom model development.

Here’s the quick math: when billed hours stall but payroll climbs from $495k in Year 1 toward $126M by Year 5, margin pressure rises fast. Higher utilization lifts revenue without matching overhead, but weak utilization cuts owner pay because the same payroll base is carrying too much nonbillable time.

Track Billable Hours

Measure billable hours ÷ available hours by service line each week. Split time into support, projects, custom models, and nonbillable work like QA and admin, then compare that mix to what you sold. One clean rule: if nonbillable time is growing, fix scope or staffing before adding headcount.

Protect utilization with tighter scheduling and cleaner scopes. Use retained support to fill baseline hours, reserve senior staff for custom model work, and track where delivery leaks time. If onboarding, reporting, or QA takes too long, cash flow slips because payroll keeps running while invoicing lags.

3

Delivery Labor And Staffing

Delivery Labor And Staffing

This driver covers contractors, full-time staff, and the role mix that delivers client work. In sports analytics consulting, project-specific contractor fees start at 9% of revenue and fall to 7%, while payroll grows from $495k in Year 1 to $126M in Year 5 as senior data scientists, analysts, junior data scientists, sales, and admin are added.

That growth expands capacity, but it also cuts gross margin if demand does not keep up. Contractors hit delivery margin first, while employees flow into operating expenses, so the owner’s take-home pay gets squeezed when staffing runs ahead of retained work or signed projects. Here’s the quick math: more labor only helps if billable revenue rises faster than payroll.

Hire Against Signed Work

Track three inputs every month: retained demand, signed project backlog, and labor cost as a share of revenue. If contractor spend is near 9% of revenue and payroll is moving up, use that as a warning signal, not a target. The goal is simple: staff to demand, not hope.

- Hire only after bookings support it

- Separate delivery margin from overhead

- Watch payroll against backlog coverage

- Use contractors for short spikes

What this estimate hides is timing. If a team adds senior or junior staff before renewals land, cash flow can tighten fast and owner pay usually falls first. Keep scope, utilization, and staffing plans tied to the actual mix of support, project work, and custom model demand.

4

Data, Software, And Technology Costs

Data, Software, And Tech Costs

These costs cover premium data licenses, core software, cloud compute, security, video analysis, business intelligence, and reporting. In this model, premium data runs 8% of revenue in Year 1 and 6% in Year 5, while core software and cloud run 6% to 4%. If you don’t price them into contracts, they come straight out of EBITDA and owner pay.

Here’s the quick math: every 1% of unrecovered data or software cost cuts EBITDA by about $9k at Year 1 revenue and $90k at Year 5 revenue. That cost protects model quality, but the margin hit is real unless project fees and recurring tech charges are spelled out in the deal.

Recover It In The Contract

Track three inputs on every job: revenue, data license %, and software/cloud %. Separate recurring pl atform use from project work, then label any pass-through data fees in the scope so recovery is explicit. One clean rule: if the client uses the model, the client helps fund the model.

- Bill premium data as a line item.

- Recover cloud by project or retainer.

- Review cost-to-revenue monthly.

If usage grows but pricing does not, EBITDA shrinks fast and the owner’s draw gets squeezed even when revenue looks strong.

5

Retention And Repeat Work

Repeat Work Stabilizes Income

Retention here means renewals, in-season support, dashboard maintenance, and long-term advisory work. In the model, recurring support attachment rises from 40% in Year 1 to 85% in Year 5, so more revenue comes back without a fresh sale each time. That lowers sales pressure, steadies utilization, and makes owner pay less tied to one-off projects.

Repeat work also reduces cash swings, which matters when the model shows a $644k minimum cash need in Month 7. Here’s the catch: stable revenue only helps if retained accounts stay efficient; if support expands faster than fees, margin falls even while renewals look strong.

Track Renewal Revenue, Not Just New Sales

Measure recurring support by client, season, and service line. Track how much comes from renewals versus project work, then compare that mix with the 40% to 85% attachment path in the model. If retention covers more payroll and software, the owner can draw income with less month-to-month stress.

Watch three inputs: client count, renewal rate, and hours per account. Also keep CAC in view; the model shows it moving between $5k and $35k as marketing efficiency changes. If a retained client needs heavy senior time, reprice the support before it eats the margin that should reach the owner.

6

Compare low, base, and high owner-income planning scenarios

Owner income scenarios

Owner income moves with ramp speed, billable mix, and headcount. Year 1 can support a $180k salary but still lose money; Year 2 and Year 5 can fund more upside.

| Scenario | LowCash-risk ramp | BaseEarly profit | HighScaled upside |

|---|---|---|---|

| Launch model | The owner stays on a cash-funded $180k salary while Year 1 still posts a loss. | The owner keeps pay steady while Year 2 turns profitable enough to support modest upside. | The owner can take salary plus distributions in a Year 5 scale case with strong EBITDA. |

| Typical setup | Year 1 is a ramp case with about $877k revenue, 72% contribution margin, about $721k payroll, and about -$90k EBITDA, so owner pay depends on cash already in the business. | Year 2 runs at about $22M revenue, 74% contribution margin, about $931k payroll, fixed overhead, and marketing, with about $696k EBITDA before taxes and reserves. | Year 5 scales to about $90M revenue, 80% contribution margin, about $1.586M payroll, fixed overhead, and marketing, with about $5.602M EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $180k salarySalary funded | Salary plus profitProfit capacity | Salary plus distributionsScale upside |

| Best fit | Use this to test a cash-risk ramp when client wins are slow and headcount is already in place. | Use this if you expect a normal Year 2 run rate and want to gauge early profit capacity. | Use this if you want to stress test team-supported scale, but not guaranteed owner distributions. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Sports Analytics Consulting Porter's Five Forces Analysis

- Sports Analytics Consulting BCG Matrix

- Sports Analytics Consulting Business Model Canvas

- 7 Critical KPIs to Track for Sports Analytics Consulting

- Sports Analytics Consulting Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Profitability in Sports Analytics Consulting

- How Much Does It Cost To Run Sports Analytics Consulting Monthly?

- Sports Analytics Consulting Startup Costs: $155K CAPEX Plan

- Sports Analytics Consulting Financial Model Template in Excel

- How to Open a Sports Analytics Consulting Business in 6–12 Weeks

- How to Write a Sports Analytics Consulting Business Plan

- Sports Analytics Consulting Marketing Mix

- Sports Analytics Consulting Marketing Plan

- Sports Analytics Consulting Business Proposal

- Sports Analytics Consulting PESTEL Analysis

- Sports Analytics Pitch Deck Example Editable PPTX

- Sports Analytics Consulting Business SWOT Analysis

- Sports Analytics Consulting Value Proposition Canvas

Frequently Asked Questions

The model pays the owner a $180,000 CEO / lead consultant salary each year Profit available beyond that depends on EBITDA, which is -$90,000 in Year 1, $696,000 in Year 2, and $5602 million in Year 5 before taxes, debt, capex, reserves, and personal distributions