Owner income$0 to $2.656M

Owner income$0 to $2.656MHow Much Can an Aid Distribution Owner Make on $167M-$844M Revenue?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0 to $2.656M  Net margin-32% to 31%

Net margin-32% to 31% Revenue for target pay$3.37M

Revenue for target pay$3.37M Business difficultyHard

Business difficultyHard

Key Takeaways

- Longer contracts steady cash and founder pay.

- Small pricing gaps hurt when payroll stays fixed.

- Logistics savings matter more as revenue scales.

- Profits can still hide a cash crunch.

Owner income$0 to $2.656MNet margin-32% to 31%Revenue for target pay$3.37MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with revenue, gross margin, payroll, overhead, reserves, taxes, and payment timing.

Want to see the full model?

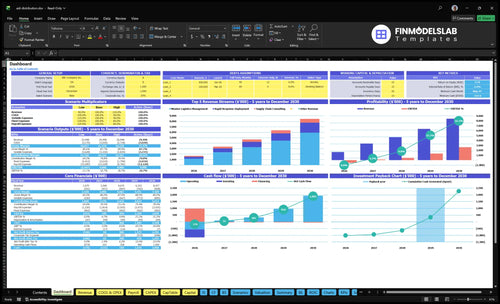

This dashboard in the Humanitarian Aid Distribution Service Financial Model Template shows revenue, EBITDA, cash, breakeven, payback, and owner income assumptions—open it.

Charts show $167M to $844M revenue growth, -$533k to $2656M EBITDA, $238k cash trough, and 47-month payback.

Model highlights

- Pricing, billable hours, mix

- Direct costs and payroll

- Marketing, capex, working capital

- Reserves, payment lag, scenarios

Use it as a next-step planning tool, not a salary promise or compliance approval.

How much can the owner of a humanitarian aid distribution service make?

The owner of a Humanitarian Aid Distribution Service should expect little to no profit-based take-home in Year 1: the model shows -$533k EBITDA on $167M revenue, so owner pay must come from a budgeted salary or replacing a paid role, not surplus; see How Increase Humanitarian Aid Distribution Service Profitability? for the profit levers. By Year 2, EBITDA is only $160k before taxes and reserves, while Year 5 reaches $2,656M EBITDA on $8,437M revenue, or a 31.5% EBITDA margin.

Owner take-home

- Year 1 surplus: $0

- Year 1 EBITDA: -$533k

- Year 2 EBITDA: $160k

- Taxes and reserves come first

What changes pay

- Replace a paid operating role

- Draw only approved salary

- Wait for true surplus

- Contractor economics aren’t guaranteed salary

How much revenue is needed to pay an aid distribution founder?

For Humanitarian Aid Distribution Service, the founder pay question starts with true fee revenue, not gross contract billings. With $1.587M in fixed overhead and 27% direct and variable costs, break-even before owner pay is about $2.174M; adding a $185k owner-operator role lifts the need to about $2.427M. Restricted or reimbursed funds still are not free cash.

Base revenue math

- $402k fixed overhead

- $1.065M payroll

- $120k marketing

- $1.587M operating load

Founder pay impact

- 73% contribution margin

- $2.174M break-even before founder pay

- $185k owner-operator role

- $2.427M revenue needed after founder pay

Can an aid distribution service owner earn more by scaling contracts?

Yes—the Humanitarian Aid Distribution Service can earn more by scaling contracts, but only if contract volume outruns payroll, overhead, reserves, and payment lag. In the model, higher-scale contract management supports $8,437M Year 5 revenue and $2,656M EBITDA, but cash still falls to -$238k in Month 17. Here’s the trade: lean outsourced coordination lowers assets but can cap control and margin, while hybrid warehousing adds storage control but raises working capital risk.

Scale helps revenue

- Year 1 starts with 8 FTE-equivalent roles.

- Mission, engineering, and response teams grow later.

- More contracts can lift EBITDA fast.

- Volume has to beat cash lag.

Watch the cash risk

- Month 17 minimum cash hits -$238k.

- Payroll rises before cash comes in.

- Warehousing adds control and storage cost.

- Outsourcing cuts assets but may trim margin.

Want the six main income drivers?

1

$1.7M-$8.4MContract Reliability

More steady aid contracts lift revenue fast, and missed deliveries or weak repeat work cut owner take-home just as quickly.

2

$250-$550/hrRate Mix

Higher hourly rates and a better split across service lines raise income without adding the same level of cost.

3

11%-15%Cost Control

Local partner fees and data feed costs sit on the revenue line, so tighter logistics control drops more cash to the bottom line.

4

$1.1M-$2.7MStaffing Scope

Payroll is the biggest cash drain, so hiring pace and how much the owner covers directly shape take-home profit.

5

$402KCompliance Load

Fixed overhead for security, liability, software, and admin sets the cash floor, so any creep here hits income hard.

6

-$238KCash Cushion

Minimum cash turns negative in month 17, so reserve funding can mean the difference between growth and expensive stopgaps.

Humanitarian Aid Distribution Service Core Six Income Drivers

Contract Volume And Reliability

Contract Volume and Reliability

Contracted mission volume is what makes owner pay predictable. When source revenue rises from $167M in Year 1 to $8,437M in Year 5 and the recurring mission logistics mix climbs from 60% to 80%, cash is easier to forecast, reserves build faster, and founder draws can be steadier.

This driver includes signed mission hours, renewal rate, and the split between contracted service revenue and pass-through aid value. Rapid response work still pays well at $450 to $550/hour, but it can create cash swings, so more repeat contracts usually support more consistent profit and owner distributions.

Track the recurring mix

Build the forecast from contracted hours, not total aid value moved. Separate service fees, reimbursable costs, and pass-through goods so you can see what actually hits gross margin and cash flow.

Push the revenue mix toward 80% recurring work instead of 60%. That makes payroll, compliance, and reserve planning less jumpy, and it gives the owner a cleaner path to regular draws.

1

Pricing And Fee Structure

Rate Card and Margin

Pricing has to cover direct field costs, reporting, risk, overhead, and margin. In this model, mission logistics runs $250 to $300/hour, rapid response runs $450 to $550/hour, and consulting runs $300 to $350/hour. If the rate only covers labor, owner pay gets squeezed because payroll and compliance are fixed-heavy.

Cost-plus or management-fee pricing works when allowable costs are clear. Fees are not free cash; they are tied to approved costs and documented service. A $25/hour pricing miss across 1,000 billable hours is $25,000, so small gaps cut cash fast.

Track the Real Billable Rate

Build each quote from the same inputs: billable hours, direct labor, local partner fees, overhead, risk cost, and target margin. Keep mission logistics, rapid response, and consulting separate so you can see which work funds the business and which work only covers cost.

- Billable hours by service line

- Allowable costs by contract

- Gross margin after direct spend

- Cash timing on invoices

- Owner draw after reserves

If reimbursement is slow or cost rules are vague, raise the fee or tighten billing terms. Track margin by mission, because flat rates with rising payroll and compliance costs will cut founder income even when revenue looks strong.

2

Direct Logistics Cost Control

Direct Logistics Cost Control

For humanitarian aid distribution, this driver is the gap between service revenue and the costs tied to moving aid. The model shows direct and variable cost ratios falling from 27% in Year 1 to 19% in Year 5. That means on $1M of revenue, direct cost drops from $270k to $190k, adding $80k in gross margin before overhead and owner pay.

Watch the cost stack closely: local partner fees, real-time data feeds, high-risk insurance, cloud infrastructure, freight, temporary storage, loading, routing, last-mile delivery, and damaged supplies. The quick math is simple: gross margin = revenue - direct logistics costs. If those costs slip by even 1%, that hurts take-home income more as missions and revenue scale.

Track Cost per Mission

Measure direct cost by mission, lane, and partner, not just by month. Split out freight, storage, local fees, insurance, cloud costs, and damage/write-offs. That shows where margin leaks happen and whether a project is truly profitable after field work.

- Track cost as a % of service revenue.

- Compare planned vs actual mission cost.

- Flag damage and reroute losses fast.

- Test partner rates before scale-up.

What this estimate hides: a low headline rate can still miss profit if last-mile failures, re-delivery, or emergency storage spike. Better routing, tighter partner terms, and cleaner reporting raise gross margin, which is the cash pool that helps cover overhead and owner draw.

3

Staffing And Founder Role

Founder Labor Replacement Cost

This driver is the cost of replacing the founder’s work in operations, contract management, compliance, and executive oversight. Inputs are founder hours, role scope, and market salary rates. In this model, payroll starts at $1065M in Year 1 and reaches $2735M by Year 5, so take-home income depends on whether added revenue covers that labor before any owner draw.

A Director of Global Logistics is modeled at $185k/year. That matters because hiring too early can absorb cash fast, even when sales are rising, and it can delay founder distributions until the business has enough margin after payroll.

Track Role Replacement Before Hiring

Measure the work the founder is actually doing, then price each role at market pay. Use that to test whether the business can support a hire without squeezing owner pay. If the new role does not lift billable missions, contract reliability, or compliance capacity fast enough, distributions stay tight.

Keep a simple staffing forecast for operations, contract management, compliance, and executive work. Separate replacement cost from profit, and only add a full-time leader when the cash forecast still shows room for payroll, reserves, and owner income after the hire.

- Track founder hours by role.

- Price replacement labor at market rates.

- Hire only when cash still covers distributions.

4

Compliance, Insurance, And Administration

Compliance and risk overhead

This driver cuts distributable cash, but it can also unlock bigger aid contracts. The fixed load here is about $53k/month from $45k cybersecurity and compliance monitoring, $3k professional liability and errors and omissions coverage, and $5k legal and audit fees, before any zone-based insurance.

High-risk zone insurance starts at 8% of revenue and can fall to 6%. So the owner’s pay depends on revenue scale and contract quality: if compliance helps win larger, steadier missions, the extra cost can be offset by better gross margin and less cash swing. What this hides is timing, since audit and insurance bills hit now, while contract approvals can lag.

Track compliance cost per contracted dollar

Measure compliance spend as a % of revenue, plus the share of bids that require audits, insurance proof, or monitoring logs. If those costs rise but win rate does not , owner income gets squeezed fast. If they support more awarded work, the spend is earning its keep.

- Track fixed cost at $53k/month.

- Separate insurance from legal and audit.

- Price risky missions at full load.

- Forecast cash before contract starts.

Use the contract model to decide what to accept. A mission that needs the full compliance stack should carry the full cost, including the 8% to 6% insurance band. If pricing does not cover that load, the business may look busy but still leave the owner with thin or no draw.

5

Working Capital And Reserves

Working Capital and Reserves

Humanitarian aid distribution can look profitable on paper and still starve owner pay in the short run. This model reaches breakeven in Month 10, but cash still bottoms at -$238k in Month 17, and payback takes 47 months. Upfront freight, field mobilization, insurance, payroll, and slow reimbursement tie up cash, so reserve-adjusted owner income can stay low even when contracts are signed.

What matters is the cash gap, not just margin. Track reimbursement lag, mobilization timing, and how much cash is trapped in active missions versus the reserve you keep for the next deployment. If the reserve is too thin, distributions to the owner should stay low until collections catch up.

Improve reserve coverage and cash timing

Build the forecast from mission hours, billing terms, payroll timing, freight deposits, and insurance payments. Then test how much cash is needed to fund the worst month, not the average month. A -$238k trough means the owner needs a real buffer before drawing income.

- Track days to reimbursement.

- Separate billable hours from pass-through costs.

- Hold a mission cash reserve.

- Delay owner draws until cash turns positive.

Reserve policy changes owner pay fast: higher buffers protect operations, but they also cut near-term distributions. The goal is to keep enough cash to fund the next deployment without forcing the owner to finance working capital personally.

6

Compare lean, base, and higher-scale owner-income scenarios

Owner income scenarios

Owner income moves with revenue timing, gross margin, payroll load, and reserve needs. Year 1 is loss-making, Year 3 turns positive, and Year 5 supports the strongest distribution base.

| Scenario | Lean CaseLean case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Year 1 stays in a low-income ramp with negative EBITDA and no profit-based owner draw. | Year 3 becomes the modeled middle case with positive EBITDA and a workable owner-income base. | Year 5 is the stronger earnings path with a much larger EBITDA pool for owner income and reinvestment. |

| Typical setup | Year 1 uses $1.670M revenue and 73% gross margin, but payroll, fixed overhead, and launch costs still drive EBITDA to -$533k. | Year 3 uses $4.670M revenue and 77% gross margin, with $459k EBITDA before tax and reserves after payroll, overhead, and marketing. | Year 5 uses $8.437M revenue and 81% gross margin, with $2.656M EBITDA before tax and reserves as the team and service base scale. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0No draw | $459k EBITDAProfit base | $2.656M EBITDAUpside pool |

| Best fit | Use this to stress-test early cash needs, especially if payment lag pushes the cash low point toward Month 17. | Use this for a steady operating plan where the owner can model distributions only after reserve and timing needs are covered. | Use this to test upside if staffing, reserves, and payment lag stay controlled while demand and contract size keep rising. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Humanitarian Aid Distribution Service Porter's Five Forces Analysis

- Humanitarian Aid Distribution Service BCG Matrix

- Humanitarian Aid Distribution Service Business Model Canvas

- What 5 KPIs Should Humanitarian Aid Distribution Service Business Track?

- Humanitarian Aid Distribution Service Business Plan Template in Pre-Written Word

- How Increase Humanitarian Aid Distribution Service Profitability?

- What Are Operating Costs Of Humanitarian Aid Distribution Service?

- Cost To Start A Humanitarian Aid Distribution Service: $585K CAPEX

- Humanitarian Aid Distribution Service Financial Model Template in Excel

- How to Open a Humanitarian Aid Distribution Service in 3 to 6 Months

- How To Write A Business Plan For Humanitarian Aid Distribution Service?

- Humanitarian Aid Distribution Service Marketing Mix

- Humanitarian Aid Distribution Service Marketing Plan

- Humanitarian Aid Distribution Service Business Proposal

- Humanitarian Aid Distribution Service PESTEL Analysis

- Humanitarian Aid Distribution Service Pitch Deck Example Editable PPTX

- Humanitarian Aid Distribution Service Business SWOT Analysis

- Humanitarian Aid Distribution Service Value Proposition Canvas

Frequently Asked Questions

In the researched model, profit-based owner pay is not supported in Year 1 because EBITDA is -$533k on $167M revenue Year 2 shows $160k EBITDA before taxes, reserves, and reinvestment By Year 5, EBITDA reaches $2656M on $8437M revenue, but distributions still depend on contracts and cash timing