Annuity Insurance Sales Startup Costs: $843K First-Year Cash Need

You’re planning for licensing, compliance, errors and omissions insurance, technology, office setup, marketing, and cash runway before commissions settle into a pattern The researched base case separates $585K of CAPEX, $45K of Year 1 marketing, $595K of monthly fixed overhead, and a $843K minimum cash need in Month 2 It excludes personal living costs, guaranteed carrier approval, and any promise that commission timing will match the model

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for an annuity insurance sales business before launch.

CAPEX limits Excludes inventory, payroll runway, deposits, debt service, working capital, commissions, marketing spend, licensing fees, E&O premiums, and recurring SaaS unless you intentionally capitalize it.

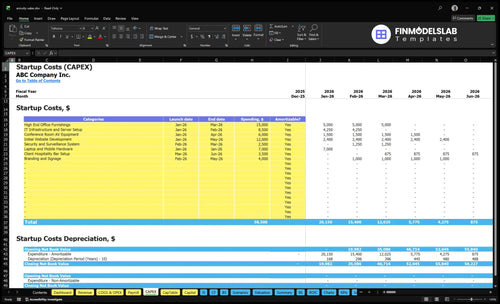

What does the Annuity Insurance Sales model screenshot show?

This Annuity Insurance Sales Financial Model Template tracks each expense category, launch timing, and whether costs are depreciated or amortized. Review $585K in Month 1 to Month 6 assets, Month 3 breakeven, and $843K Month 2 cash as validation, not a promise.

Key screenshot highlights

- 585K CAPEX, Months 1-6

- 595K monthly overhead

- 45K Year 1 marketing

- 600 E&O monthly

- 850 CRM and planning

- 60-month model period

- 1.672M revenue, 794K EBITDA

- Month 3 breakeven

- 843K cash, Month 2

How should I fund an annuity insurance sales startup?

If you're starting Annuity Insurance Sales, fund it in stages, not all at once: cover Month 1 setup, then bridge the Month 2 cash peak of $843K with founder capital, partner capital, or an agency credit line. Month 1 should start office rent, CRM, E&O, telecom, dues, utilities, principal advisor, client service coordinator, and part-time compliance officer, while CAPEX runs from Month 1 to Month 6 and totals $585K. Breakeven hits in Month 3 and payback lands in 6 months in the researched case, but don’t rely on unapproved carrier contracts or immediate variable annuity production.

Funding plan

- Start Month 1 fixed costs.

- Stage CAPEX through Month 6.

- Use founder and partner capital.

- Bridge Month 2 with credit.

Cash risk

- Peak cash need: $843K.

- CAPEX total: $585K.

- Breakeven starts in Month 3.

- Do not count on instant commissions.

What hidden costs come with starting an annuity insurance sales business?

For Annuity Insurance Sales, the hidden cost is cash timing: separate operating needs from capital spending (CAPEX), because the $585K asset budget does not cover E&O premiums, marketing, payroll, or runway. What Are The Operating Costs For Annuity Insurance Sales? still points to about $2,000 a month in core overhead, and if carrier appointments or broker-dealer onboarding slip, plan on a $843K minimum cash need in Month 2, not immediate commission income.

Cash burn

- $850 CRM and planning software

- $600 E&O insurance

- $300 telecom and high-speed internet

- $250 professional membership dues

Delay risks

- State license renewals and continuing education

- Compliance review time and ad approval

- Chargebacks, deductibles, and complaint support

- Secure document storage and appointment delays

What are the biggest startup costs for an annuity insurance sales business?

Annuity Insurance Sales gets expensive first in licensing, oversight, compliance, and lead generation. A Year 1 working mix is 10% of revenue for carrier lead referral fees, 5% for broker-dealer transaction charges, 12% for marketing and lead gen, and 3% for compliance and audit fees, with a $45K marketing budget and about $850 CAC. Fixed annuities stay simpler, but variable annuities add securities supervision and can cut payout through platform charges, splits, and approval rules.

Year 1 cost stack

- 10% carrier lead referral fees

- 5% broker-dealer charges

- 12% marketing and lead gen

- 3% compliance and audit

What drives the gap

- Variable annuities add securities supervision

- Fixed annuities avoid some oversight

- Broker-dealer rules can delay payouts

- $850 CAC anchors lead cost

Calculate Fuding Needs

Startup Cost Summary

This table shows the main startup asset costs and the separate cash reserve needed before launch.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| High-end office furnishings | $15,000 | Office fit-out and client meeting setup | Yes |

| IT infrastructure and server setup | $8,500 | Systems, network, and data handling setup | Yes |

| Initial website development | $12,000 | Lead capture and online presence buildout | Yes |

| Laptop and mobile hardware | $7,000 | Advisor devices and field work tools | Yes |

| Conference room AV equipment | $6,000 | Client presentation and meeting room setup | Yes |

| Minimum cash reserve | $843,000 | Month 2 cash gap from $5,950 fixed overhead and $225k Year 1 core payroll | No |

Annuity Insurance Sales Core Five Startup Costs

Licensing, Exams, and Regulatory Setup Startup Expense

Licensing Stack

One national license price won’t fit this model. Build the startup line state by state for pre-licensing education, state exam fees, producer application, background check, and, for the 30% variable annuity mix, securities licensing plus FINRA registration such as Series 6 or Series 7.

Pre-Opening Cost Line

Use one line per state: education hours × provider fee, exam fee × attempts, application fee, and fingerprinting/background check. Then add any FINRA and securities registration work only where variable annuities are sold. That keeps the licensing budget tied to your 45% fixed annuities, 30% variable annuities, and 25% income riders sales mix.

- Map each selling state first

- Price exam retakes separately

- Include carrier onboarding rules

Renewal Run Rate

Keep a recurring line for license renewals and continuing education planning, because both are ongoing compliance costs, not one-time setup. This usually sits outside launch CAPEX and should be budgeted as annual operating expense. For variable annuities, renewals also need to track any securities registration maintenance tied to the affiliation model and state rules.

- Track renewal dates by state

- Reserve CE budget each year

- Watch product and carrier changes

Rule Differences

Requirements vary by state, product type, carrier, and affiliation model, so the cheapest path can still be wrong if it blocks variable annuity sales. Fixed annuities usually stay inside insurance rules, but variable annuities add securities registration and FINRA oversight. Build the budget from the exact states you will open in, not from a national average.

Carrier Appointment, Broker-Dealer, and Compliance Startup Expense

Setup Scope

If you sell only fixed annuities, setup stays closer to carrier rules and state insurance licensing. Add variable annuities, and you usually bring in broker-dealer onboarding, suitability review, advertising approval, recordkeeping, and a compliance manual. That choice changes both launch time and the budget.

Licensing

Budget licensing state by state: life insurance producer pre-licensing, state exams, applications, background checks, and continuing education. If variable annuities are part of Year 1, you also need securities licensing, which means registration to sell products treated as securities. The mix assumption is 45% fixed, 30% variable, and 25% income riders.

- State-by-state pre-opening cost

- Recurring renewal line

- Continuing education line

Compliance Load

Carrier contracting and broker-dealer review are often paid as fee splits or platform charges, not just invoices. Using the planning anchors, carrier lead referral fees run 10% of Year 1 revenue, broker-dealer transaction charges 5%, and compliance and audit fees 3%. On the stated revenue base, that maps to $1,672K, $836K, and $5,016K.

- Direct fee or payout split

- Platform charge or audit bill

- Review before launch

Spend Control

Keep the spend down by starting with the narrowest product set that still fits your client. Pre-clear ads, use one document process, and write down who approves what before sales start. The common mistake is funding variable-annuity supervision before the license stack and carrier appointments are ready, which burns cash fast.

Errors and Omissions Insurance Startup Expense

E&O Cover

Errors and omissions insurance (E&O) is a fixed startup cost at $600 per month, or $72,000 in year 1. It helps defend against claims tied to advice, paperwork, or the sales process, but it does not guarantee the claim outcome or give legal immunity. If your book has more complex annuity work, the risk goes up.

What It Covers

Price it from 12 months of coverage, the policy limit, the deductible, and the product mix. Ask for coverage on annuity suitability complaints, product restrictions, and cyber liability if client data is involved. Premiums vary by state, carrier rules, claim history, sales volume, and how much variable annuity and income rider business you place.

- State rules change pricing.

- Variable annuities raise scrutiny.

- Documentation supports the defense.

Keep Risk Tight

Keep the cost in check by cleaning up the sales file before launch: use dated notes, signed disclosures, and carrier-approved forms. That won’t make a bad sale safe, but it can cut avoidable disputes. A fixed-annuity-heavy book usually carries less pressure than one centered on variable annuities and income rider recommendations.

- Match limits to sales volume.

- Use only approved scripts.

- Review deductibles for cash flow.

Policy Reality

E&O is a planning requirement, not a shield. It can help pay defense costs and covered settlements within policy terms, but it does not erase poor disclosure, missing records, or regulatory review. If your workflow includes variable annuities or income rider recommendations, verify that complaint handling and recordkeeping fit the real sales process before you open.

Technology, CRM, and Secure Client Management Startup Expense

Launch tech stack

Start with a $110K one-time technology CAPEX base: $85K for IT infrastructure and server setup, $7K for laptop and mobile hardware, $12K for the website, and $6K for conference room AV equipment. That covers the core setup before any recurring software, storage, or security tools.

Monthly SaaS run rate

The recurring base is $1,150 per month: $850 for CRM and financial planning software plus $300 for telecom and high-speed internet. Here’s the quick math: 12 months of that base run rate equals $13,800 a year, before compliance archiving, secure email, e-signature, call tracking, proposal tools, or cyber add-ons.

- Track seats, not just licenses.

- Price archiving separately.

- Renew telecom on term deals.

Compliance and security

Compliance archiving matters because client calls, emails, proposals, and signed forms need to stay searchable and retained. Build it into the stack with secure document storage, secure email, e-signature, and call tracking, then add a separate cybersecurity reserve if your policy requires tighter controls. What this estimate hides is the vendor quote for retention length and storage volume.

- Keep retention rules in writing.

- Archive before deleting anything.

- Test access after every update.

Budget split

Separate one-time setup from monthly SaaS so the model stays clean: capex for hardware, server setup, website build, and AV; opex for CRM, planning software, telecom, archiving, and security tools. If onboarding takes 14+ days, delay revenue assumptions until the workflow is stable and compliant.

Launch Marketing and Lead Generation Startup Expense

Launch Budget

Count launch marketing as a pre-opening operating expense, not CAPEX, except website development if your policy lets you capitalize it. The Year 1 budget is $45K; at $850 CAC, that funds about 53 customers ($45,000 ÷ $850). For this business, the spend has to cover trust-building and follow-up, not just clicks.

Cost Drivers

Build this line from website launch, local search visibility, paid leads, direct mail, educational seminars, referral marketing, compliance-approved ads, and follow-up campaigns. Use vendor quotes, monthly lead goals, and approval time to size it. The budget belongs in pre-opening or early operating expense unless website development is capitalized under policy.

- Use monthly lead targets.

- Price compliance review time.

- Separate website build cost.

Spend Control

Keep the first spend wave narrow: local search, referrals, and follow-up usually come before paid leads and direct mail. Build compliance review into the launch calendar so ads do not stall. One line to remember: results are not guaranteed, and the real CAC can move if lead quality or approval timing changes.

Variable Cost View

The prompt’s variable-cost view uses 12% of revenue and shows about $20,064K; reconcile the revenue base before you lock the budget. If you tie spend to sales, this line scales with growth, but compliance approval and lead quality still shape the real outcome.

Compare 3 Startup Cost Scenarios

Scenario table

A home-based fixed-annuity launch needs less cash than a staffed office plan, while variable-annuity and heavier compliance add more burn. The base case anchors the model at $843K minimum cash in Month 2.

| Scenario | Lean LaunchHome-based start | Base LaunchIndependent producer | Full LaunchOffice and variable |

|---|---|---|---|

| Launch model | A home-based fixed-only launch keeps the team small and avoids a full office buildout. | This is the anchor model for an independent producer with a modest office and full core staffing. | A fuller launch adds office space, variable-annuity capability, and tighter supervision needs. |

| Typical setup | Use remote work, basic software, and low-overhead marketing with no office-heavy spend. | Use the model's base staffing, $45K Year 1 marketing, and standard office and software costs. | Expect higher compliance, broker-dealer supervision, more lead generation, and a larger office footprint. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $700,000 - $800,000Lower burn | $843,000 - $900,000Anchor case | $950,000 - $1,100,000Heavier build |

| Best fit | Best for a fixed-only agent who wants a lean start and can work mostly from home. | Best for an independent producer who wants the model's base operating setup and steady growth path. | Best for a variable-annuity or office-based launch that plans to scale faster and carry more overhead. |

Planning note: Scenario ranges are researched planning assumptions, not exact vendor, carrier, or quote-based pricing. Use them to size funding before user inputs and written market bids.

Related Products

- Annuity Insurance Sales Porter's Five Forces Analysis

- Annuity Insurance Sales BCG Matrix

- Annuity Insurance Sales Business Model Canvas

- What Are The 5 KPIs For Annuity Insurance Sales Business?

- Annuity Insurance Sales Business Plan Template in Pre-Written Word

- How Increase Annuity Insurance Sales Profitability?

- How Increase Annuity Insurance Sales Profitability?

- Annuity Insurance Sales Financial Model Template in Excel

- How Much Does An Annuity Insurance Sales Owner Make? $125k Plus Profit

- How To Start An Annuity Sales Business In 60–120 Days

- How To Write A Business Plan For Annuity Insurance Sales?

- Annuity Insurance Sales Marketing Mix

- Annuity Insurance Sales Marketing Plan

- Annuity Insurance Sales Business Proposal

- Annuity Insurance Sales PESTEL Analysis

- Annuity Sales Pitch Deck Example Editable PPTX

- Annuity Insurance Sales Business SWOT Analysis

- Annuity Insurance Sales Value Proposition Canvas

Frequently Asked Questions

The researched base case needs about $843K of minimum cash, with the low point in Month 2 That includes $585K of CAPEX, $45K of Year 1 marketing, and monthly fixed overhead of $595K before payroll The number moves fast if you sell variable annuities, rent an office, hire staff early, or buy leads before appointments are complete