Owner income17.8% ROE

Owner income17.8% ROEHow Much Does an Apartment Development Owner Make Across 7 Projects

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income17.8% ROE  Net margin2.0% IRR

Net margin2.0% IRR Revenue for target pay$251M basis

Revenue for target pay$251M basis Business difficultyHard

Business difficultyHard

This 60-month apartment development owner income view covers 7 owned projects, $73M of acquisition costs, and $178M of construction budgets It tracks fees, overhead, payroll, reserves, financing logic, sale timing, and owner take-home, but it does not provide tax advice, guaranteed salary claims, or market-specific investment recommendations

Owner income17.8% ROENet margin2.0% IRRRevenue for target pay$251M basisBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it is not lending advice or an appraisal.

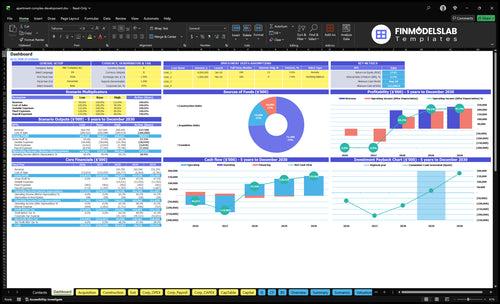

How do you check owner income in an apartment development model?

This screenshot shows how Apartment Development tracks revenue, margin, costs, reserves, and owner take-home—open the Apartment Development Financial Model Template.

Owner-income model highlights

- Owner take-home outputs

- $73M acquisition costs

- Month 33-55 exit

Is apartment development profitable for owners?

Yes—Apartment Development can be profitable, but the owner’s seat changes the risk and the payout. An active sponsor who manages entitlement, financing, construction, reporting, and exit can earn fees and upside; a passive equity owner usually relies on distributions and has less control. The timeline is long too: acquisitions can start Month 3 to Month 20, construction can start Month 6 to Month 23, projects can run 12 to 18 months, and sales can land anywhere from Month 33 to Month 55.

Active sponsor

- Earnings include fees and upside

- Control sits with the operator

- Workload covers the full project

- Reward rises with execution

Key risks

- Delays push out cash flow

- Leverage raises downside fast

- Capital calls can surprise owners

- Reserves can block distributions

How do apartment developers make money?

Apartment Development makes money from fees during the project, cash flow after lease-up, and upside when the asset refinances or sells; the sharper KPI question is here: What Is The Most Critical Indicator For Success In Your Apartment Development Business?. Not every deal pays every stream: known fixed pay is CEO salary at $250,000/year, or about $20,833/month, while first sale timing starts in Month 33, so most equity upside is back-ended.

Predictable Income

- Earn developer fees during execution

- Collect asset-management fees after stabilization

- Receive rental cash flow from held properties

- Pay CEO salary: $250,000/year

Back-Ended Upside

- Capture refinance proceeds if debt allows

- Realize sale profits from Month 33

- Earn promote from outperformance

- Receive equity distributions per agreements

What affects apartment development profit margin?

Apartment Development profit margin is most sensitive to construction cost, land basis, rents, lease-up speed, interest costs, and operating expenses; with a $73M acquisition and $178M construction budget, a 1% construction overrun is $1.78M before financing. For the cost side, see What Is The Estimated Cost To Open Your Apartment Development Business? Profit also depends on cap rates, but rent, debt, unit count, and sale price are not supplied, so the margin has to be scenario-based.

Key margin drivers

- Construction and reserves hit hardest

- Land basis sets the cost floor

- Rents and lease-up speed drive revenue

- Interest and operating expenses squeeze take-home

Model gaps

- Year 1 variable expense load: 100%

- Year 2 variable expense load: 88%

- Year 3 variable expense load: 75%

- Year 4: 62%, Year 5: 50%

Want the six biggest income drivers?

1

$251MProject Scale

The $73M land buys plus $178M build budget set the profit ceiling, so scope is the biggest dollar swing in owner take-home.

2

$222MCapital Stack

The cash trough reaches about -$222.1M, so debt terms and equity timing can keep more upside in the owner's pocket.

3

M33-M55Exit Window

Sales start in Month 33 and run to Month 55, so delays push payback past the model's Month 33 break-even point.

4

$178MBuild Cost

Construction is the largest direct spend, and overruns hit equity fast because cash burn is heavy before sales begin.

5

$620K-$1.39MPayroll Ramp

Payroll climbs from $620K in Year 1 to $1.39M by Year 3, so staffing pace has to match project timing.

6

$34K/moOverhead Burn

Fixed non-payroll costs run about $33.5K a month, and every saved dollar drops straight to owner take-home.

Apartment Development Core Six Income Drivers

Project Scale And Total Development Cost

Project Scale and Total Development Cost

When project base gets bigger, owner income can rise because fees and upside sit on a larger dollar pool. Here, the known pipeline is 7 owned projects, with $73M in acquisition costs and $178M in construction budgets, or $251M total land plus construction. That works out to about $35.9M per project before soft costs and financing, so scale can lift gross earnings fast.

But bigger is not automatically better. Projects at $25M to $50M before soft costs need more capital, more debt capacity, and tighter execution. Delays, overruns, and investor splits can reduce risk-adjusted owner take-home, so the real question is not project size alone; it is whether the team can deliver on time and keep cash flow alive through lease-up, debt service, and exit timing.

Track the Full Project Base

Here’s the quick math: track total development basis as land + construction + soft costs + financing carry. The owner should test each project against debt capacity and expected partner split before start. If a $35.9M average base is moving toward $50M, the income plan must show how fee income and profit still survive a delay or a change-order run-up.

- Measure land, hard, soft, carry.

- Stress test debt capacity early.

- Watch delay and overrun risk.

What this estimate hides is timing risk. A larger project can pay more, but only if the budget, lender draw schedule, and investor terms are locked early. Track budget variance, days of delay, and capital raised versus capital needed on every deal; those three items tell you whether scale is adding owner income or just adding stress.

1

Developer Fee Structure

Developer Fee Income

The apartment developer fee is cash the owner can earn before stabilization or sale, but it is not the same as profit, promote, or equity distributions. Use the fee as an editable assumption: on the disclosed $251M land plus construction base, each 1% of fee equals $2.51M gross before sharing, overhead, and any deferral.

That gross number can shrink fast if lenders cap fees, partners split them, or cash flow pushes payment into later draws. One line matters: fee rate × project base = fee pool. The owner’s take-home depends on timing as much as rate, because a deferred fee helps revenue on paper but not payroll or draws.

Track Fee Rate And Payment Timing

Set the fee schedule in the project model and loan docs, then test it against each deal’s capital stack. Here’s the quick math: 1% on $251M is $2.51M; 2% is $5.02M. If the fee is split with partners or deferred until milestones, owner cash can lag even when project value is rising.

- Track fee rate by project.

- Track lender fee caps.

- Track partner fee splits.

- Track deferred fee balances.

- Track monthly cash collected.

What this estimate hides: overhead, reinvestment, and any fee haircut from debt terms. If fee cash is slow, owner pay slows too, so build a monthly forecast that separates earned fees from collected fees.

2

Rent, Occupancy, And Stabilized NOI

Rent, Occupancy, and Stabilized NOI

NOI means rental revenue minus operating expenses, before debt service and capital reserves. In apartment development, higher rent and lower vacancy lift stabilized NOI, which then drives valuation, refinance proceeds, sale proceeds, and distributable cash flow. Gross rent alone does not equal owner take-home; lender payments, reserves, and investor splits come first.

The key inputs are unit count, monthly rent, vacancy, operating expenses, and cap rate. Faster lease-up helps, but only if extra rent beats added costs like concessions, turnover, and property ops. If vacancy stays high, NOI falls and exit value usually drops too, because buyers price the asset off income, not headline rent.

Track lease-up and net collections

Measure physical occupancy, economic occupancy, and monthly NOI together. Physical occupancy shows filled units; economic occupancy shows cash collected after concessions and bad debt. That gap can be the difference between a property that looks full and one that actually throws off distributable cash.

To improve owner income, forecast stabilized NOI under conservative rent and vacancy assumptions, then compare it to debt service and reserves. If rent growth slows, protect cash flow by cutting vacancy loss first. The best signal is not asking rent; it’s collected rent after operating costs.

3

Construction Cost Control

Construction Cost Control

If you’re building apartments, this is the margin gate. The known $178M construction budget is the largest cost bucket, and the land plus construction base is $251M. On that base, a 1% overrun is about $1.78M before extra interest, contingency use, or change orders, so cost drift can erase sale profit and delay owner distributions.

Track Variance Before It Hits Cash Flow

Measure hard costs, soft costs, contingency, change orders, and financing carry separately. Use a live budget-to-actual view, then compare it against the 12 to 18 month construction period. If a slip pushes the exit past Month 33 to Month 55, debt needs rise and the owner’s take-home drops even if the project still sells.

Here’s the quick math: every extra dollar of construction spend comes out of sale profit or distributable cash flow after debt service and reserves. Track committed cost, remaining contingency, and delay days each month so you can cut scope, reprice trades, or reset the exit plan before overruns compound.

4

Financing, Leverage, And Interest Rates

Leverage and Interest Cost

Financing can lift equity returns on apartment development, but only after debt service is paid. Here’s the quick math: rental cash and sale proceeds first cover operating costs, loan interest, and any lender reserve. If the project comes up short, owner distributions can drop to $0 even when the property still looks fine on paper.

This model needs loan-to-cost, interest rate, draw schedule, interest reserve, amortization, debt service, and refinance terms. Higher leverage can improve returns in a strong case, but it also raises downside risk from delays, covenant pressure, and refinance gaps. Treat these as scenario inputs, not lending advice.

Track Cash Before Owner Pay

Model owner income from cash left after debt and reserves, not from gross rent or project profit alone. A higher rate or tighter covenant can absorb cash that would otherwise fund distributions. If refinance proceeds miss plan, the owner may need to wait for stabilization or sale before seeing take-home income.

- Update loan-to-cost monthly.

- Stress test rates by 100 bps.

- Watch covenant headroom each draw.

- Track reserve burn against plan.

- Test refinance proceeds before payout.

Track monthly debt service, interest reserve use, and DSCR (cash after expenses divided by debt payment). Re-run the model when rates move or construction slips. That shows whether the project still supports owner pay after the lender gets paid first.

5

Exit Strategy And Cap Rate

Exit Timing and Cap Rate

Income here depends on when you sell, refinance, or keep the asset for rent. Sale timing is modeled from Month 33 to Month 55, and value usually hinges on stabilized NOI divided by cap rate. A small cap rate move can swing sale value hard, so owner take-home can jump or shrink fast.

Here’s the quick math: sale value = stabilized NOI ÷ cap rate. That means a lower cap rate raises value, while a higher cap rate cuts it. A sale is one-time income, refinance proceeds may be distributable but add leverage, and a long hold pays only what’s left after debt service and reserves.

Track the Exit Math Early

Build the exit case with the missing inputs: sale price, cap rate, stabilized NOI, refinance proceeds, and ownership splits. If those are not current, owner income is just a guess. One clean rule: test the same asset at several cap rates before you promise distributions.

- Measure stabilized NOI monthly

- Stress cap rate by 50-100 bps

- Model Month 33 to 55 exits

- Subtract debt service and reserves

- Map cash splits before closing

If refinance looks better than a sale, check whether the extra debt still leaves room for owner pay. If the project is held, cash flow has to survive operating costs, loan payments, and reserves before anything reaches the owners.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner take-home before taxes and reserves swings with acquisition timing, build cost, sales timing, and how much cash the projects can actually distribute.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Owner take-home stays thin because costs run high, sales lag, and reserves stay locked up. | Owner take-home follows the planned pipeline with normal cost control and staged sales. | Owner take-home improves when costs hold, sales move faster, and distributions start on time. |

| Typical setup | The pipeline still carries the $73M acquisition load and $178M build budget, but delays push the Month 33 to Month 55 sales window and defer cash to owners. | The model uses the known $73M acquisition cost, $178M construction budget, 12 to 18 month builds, and Month 33 to Month 55 sales timing. | The projects close, build, and sell on schedule, with tighter vacancy, stronger pricing, and lighter reserves so more cash can reach owners. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Formula-driven downsideLow Case | Formula-driven baseBase Case | Formula-driven upsideHigh Case |

| Best fit | Use this to test delayed cash and tighter distributions. | Use this as the working case for planning and lender talks. | Use this to see what strong execution can support. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Apartment Development Porter's Five Forces Analysis

- Apartment Development BCG Matrix

- Apartment Development Business Model Canvas

- 7 Critical KPIs for Apartment Development Success

- Apartment Development Business Plan Template in Pre-Written Word

- 7 Strategies to Maximize Apartment Development Profitability

- Running Costs for Apartment Development: $85K to $145K Monthly

- Apartment Development Startup Costs: $251M Project CAPEX Plan

- Apartment Development Financial Model Template in Excel

- How To Start An Apartment Development Business In 18–36+ Months

- How to Write an Apartment Development Business Plan: 7 Essential Steps

- Apartment Development Marketing Mix

- Apartment Development Marketing Plan

- Apartment Development Business Proposal

- Apartment Development PESTEL Analysis

- Apartment Development Pitch Deck Example Editable PPTX

- Apartment Development Business SWOT Analysis

- Apartment Development Value Proposition Canvas

Frequently Asked Questions

In this model, the only fixed owner-like pay shown is a $250,000 CEO salary if the owner holds that role Project-level owner income cannot be calculated from the provided data because sale prices, debt terms, developer fee percentage, rents, cap rates, and ownership splits are not supplied The known pipeline is 7 owned projects with $251M in acquisition plus construction costs