Owner income$145k/yr

Owner income$145k/yrHow Much Can An Apprenticeship Training Program Owner Make? $145k+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145k/yr  Net margin72%–84%

Net margin72%–84% Revenue for target pay$202k/yr

Revenue for target pay$202k/yr Business difficultyMedium

Business difficultyMedium

You’re pricing employer contracts before you know what the owner can safely take home This five-year planning view covers $9815M to $182142M in annual revenue, $7041M to $153181M in EBITDA, direct costs, payroll, overhead, reserves, and owner pay assumptions These are planning estimates, not guaranteed earnings, payroll advice, tax advice, or required distributions

Owner income$145k/yrNet margin72%–84%Revenue for target pay$202k/yrBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

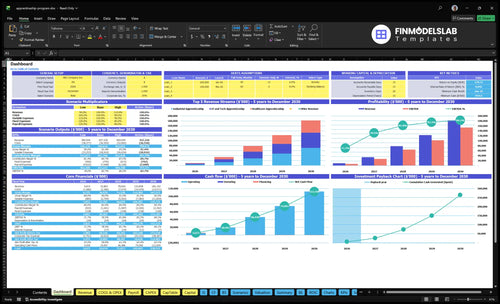

Want to see the full Apprenticeship Training Program financial model?

The dashboard shows revenue, EBITDA, cash, break-even, payback, and owner pay. Apprenticeship Training Program Financial Model Template also includes assumptions for occupancy, billable days, apprentice segments, sponsor fees, implementation fees, COGS, overhead, wages, and capex, plus scenario testing.

Model highlights

- Owner pay output included

- Revenue and EBITDA tracked

- Scenario tabs built in

- Year 1 and 5 compare

Can an apprenticeship training program owner pay themselves?

Yes, an Apprenticeship Training Program owner can pay themselves, and the linked cost view in How Much To Launch Apprenticeship Training Program? should tie that pay to filled cohorts, sponsor contracts, grant timing, staff capacity, and cash reserves. The model supports a $145,000 annual Executive Director salary from Month 1, but early draws shouldn’t outrun the cash plan because minimum cash need is $955,000.

Paycheck test

- Fill cohorts before increasing owner pay

- Secure sponsor contracts first

- Time grants before payroll commitments

- Protect the $955,000 cash need

Owner upside

- Use the $145,000 salary plan

- Add distributions only after taxes

- Pay debt and reserves first

- EBITDA of $7041M–$153181M isn’t take-home

What affects apprenticeship program owner income the most?

Owner income in an Apprenticeship Training Program is driven most by employer retention, active apprentice volume, and completion rate. Moving occupancy from 45% to 90% is the biggest scale lift, and pricing from $450 to $700 by segment raises revenue per seat. Grant funding can help cash flow, but it adds reporting and timing risk, so pay improves only when the operation scales without breaking quality.

Revenue drivers

- Retention protects recurring revenue.

- Filled seats drive monthly income.

- $700 beats $450 by segment.

- Completion supports future renewals.

What slows owner pay

- Program managers lag on demand.

- Recruitment stalls seat fill.

- Records and compliance add workload.

- Employer coordination weakens renewals.

Are apprenticeship training programs profitable after operating costs?

Yes—under these assumptions, the Apprenticeship Training Program stays profitable after operating costs, with EBITDA margin moving from about 717% in Year 1 to 841% in Year 5. Here’s the quick math: COGS is only 11% of revenue in Year 1 and 8% in Year 5, while sales and recruitment costs rise from 9% to 65%; for the KPI view, see What Are The 5 Core KPIs For Apprenticeship Training Program Business?.

Profit drivers

- 11% COGS in Year 1

- 8% COGS in Year 5

- $132k monthly fixed overhead

- 717% to 841% EBITDA margin

Cost risks

- 9% sales and recruitment in Year 1

- 65% sales and recruitment in Year 5

- Payroll rises from $565k to $1.84M

- Don’t cut training or compliance

Want the six main income drivers?

1

$450-$700Sponsor Fees

Higher monthly sponsor fees lift recurring revenue on every active apprentice, and that cash flows into income before taxes, reserves, distributions, and reinvestment.

2

330-2.6KApprentice Volume

More active apprentices turn the same delivery setup into more billable months and more total sponsor revenue.

3

89%-92%Delivery Margin

Keeping COGS tight preserves most of each fee after instruction and screening, so more of each dollar stays in EBITDA.

4

$132K/moOverhead Control

Fixed overhead of about $132K a month, plus payroll rising from $565K to $1.84M, can squeeze take-home fast if hiring runs ahead of demand.

5

45%-90%Retention Rate

Retention keeps occupancy near 45% to 90%, so seats stay billed and revenue does not reset every time a cohort ends.

6

$5K-$6KFunding Mix

The $5K to $6K implementation fee adds early cash and reduces pressure on monthly sponsor collections.

Apprenticeship Training Program Core Six Income Drivers

Employer sponsor revenue

Employer Sponsor Fees

Employer sponsor revenue comes from monthly fees per apprentice seat plus $5k to $6k implementation fees per employer. Current pricing bands are $450 to $550 a month for Industrial, $600 to $700 for IT and Tech, and $500 to $600 for Healthcare. Longer contracts and renewals make revenue steadier, but owner pay only improves after direct training costs, admin, reporting, and cash reserves are covered.

The risk is underpricing a high-touch service. Recruiting, onboarding, records, and completion reporting all take labor, so sponsor fees have to cover more than delivery time. One filled seat at the wrong price can look busy and still lose money.

Price by segment and scope

Track revenue per employer as monthly seat fees + setup fees, then subtract direct training cost, admin time, and reserves. Watch segment mix closely, because the same seat is worth more in IT and Tech than in Industrial. If contracts renew well, you cut sales pressure and smooth cash flow, which makes owner draws easier to plan.

Build pricing around the work the employer needs, not just the apprentice seat count. Test these inputs: filled seats, setup fee collected, direct cost per seat, renewal rate, and hours spent on recruiting and reporting. If service scope grows without a price increase, gross margin drops fast.

- Price by industry segment

- Charge setup fees upfront

- Track renewal rates monthly

- Measure admin hours per employer

1

Active apprentice volume

Active apprentice volume

Filled seats drive this model. Occupancy means the share of seats filled, and it rises from 45% in Year 1 to 90% in Year 5, so more of the fixed base gets covered by paying apprentices instead of idle capacity. Total capacity also grows from 330 seats to 2,550 seats across Industrial, IT and Tech, and Healthcare.

The upside is real, but not every enrolled apprentice becomes profit. Completion, program manager capacity, recruitment load, instructor availability, employer placements, and apprentice support all limit how many seats stay active. If those limits tighten, owner income can lag even when headcount grows.

Track fill, not just enrollments

Measure active seats by segment, then compare them with the stated capacity plan. Here’s the quick math: at 2,550 seats and 90% occupancy, you have about 2,295 active apprentices; at 45%, you have about 1,147.5. That gap is what turns fixed overhead like $132k per month into operating leverage.

- Active seats by segment

- Completion and placement rates

- Manager and instructor load

- Apprentice support case volume

Keep weekly watch on completions, employer placements, and staffing load before opening more seats. If fill rises but placements or support lag, revenue quality drops and the owner ends up carrying more cost per apprentice. The best growth is the kind that keeps seats full and service levels stable.

2

Funding mix

Funding Mix

Employer-paid revenue is the cleaner base here because the fee is recurring and easier to forecast than public money. If sponsor pricing runs $450 to $700 per seat per month plus $5,000 to $6,000 per employer setup, owner pay improves only when that cash covers direct training labor, admin, and compliance, not just headline revenue.

Grants and workforce development funds can help pay for implementation or training delivery, but they are uneven and can arrive late. That matters when fixed overhead is $132,000 per month; reimbursement delays can force the owner to hold more cash and delay their own draw. Don’t model public funding as guaranteed income.

Track the mix that pays on time

Use funding as an editable input, not a promise. Build the model around employer renewals, seat counts, and monthly sponsor fees, then layer grants on top only after you confirm timing, reporting, and reimbursement terms. One clean rule: if the grant is late, the business still has to make payroll.

Watch three things each month: cash collected, grant receivables, and compliance hours. Grant-heavy models need documentation, reporting, and reserve cash for gaps, so test whether public funding really raises owner income or just adds work. If it doesn’t lift free cash after overhead, it won’t pay the owner more.

- Separate sponsor cash from grant cash.

- Model reimbursement lag by month.

- Hold reserves for payroll gaps.

3

Training delivery margin

Training Delivery Margin

Training delivery margin is the cash left after direct training costs like technical instruction, screening, curriculum, learning systems, and instructor scheduling. In this model, COGS falls from 11% in Year 1 to 8% in Year 5, so gross margin after COGS improves from 89% to 92%. That means each $100 of training revenue keeps $89 to $92 before overhead.

Here’s the quick math: better standardization and remote delivery can raise instructor utilization, but only if hands-on support stays funded. If quality slips, the extra margin can disappear through rework, safety issues, weak records, or poor employer outcomes. For the owner, this driver affects EBITDA and take-home pay only after direct service quality stays intact.

Protect Margin Without Cutting Quality

Track direct cost per apprentice seat, instructor hours per cohort, screening cost, and support time by program. If a remote or standardized curriculum lowers delivery cost, test it against completion, safety, and employer satisfaction, not just margin. The right benchmark is simple: keep 89% to 92% gross margin while outcomes stay stable.

Watch where the money goes. A lower-cost format helps only when it cuts repeated instruction and admin load, not when it shifts work into unpaid overtime or weak learner support. If hands-on help is needed, fund it directly, because missed support can raise churn and wipe out the margin gain.

- Track cost per filled seat.

- Measure instructor load monthly.

- Review completion and employer outcomes.

- Cap rework and rescheduling waste.

4

Retention and completion

Retention and Completion

Completion is the share of apprentices who finish the program and stay placed through the contract period. It protects renewal revenue, repeat cohorts, and pricing power because employers see better outcomes and fewer failed seats. It also protects reputation and future cohort demand. If dropouts rise, you lose monthly seat fees and pay again for recruiting, screening, and onboarding.

The key inputs are completion rate, dropout timing, employer support, and case manager load. Higher completion improves owner income by keeping sponsor cash flowing and reducing replacement work; weak onboarding or thin support does the opposite and can turn a full cohort into a low-margin cohort.

Track and Protect Finish Rates

Measure completion by cohort, employer, and program manager, then compare it with replacement recruiting and renewal rate. If one employer or site has more exits, fix onboarding, check supervisor support, and tighten case management before the next cohort starts. One clean metric: finished apprentices ÷ started apprentices.

Use outcome reporting early, because higher completion can support sponsor satisfaction and funding eligibility where that applies. The goal is not just full seats; it is filled seats that stay filled long enough to convert into renewals, repeat cohorts, and steadier owner draw.

5

Overhead and compliance efficiency

Overhead and compliance efficiency

This driver is the cost of keeping the program legal, tracked, and on time. Fixed overhead is $132k per month for rent, hosting, liability insurance, sales tools, and the legal and compliance retainer, so the business starts with $1.584M a year in fixed load before payroll scales from $565k in Year 1 to $184M in Year 5.

That means owner income depends on how many filled seats can absorb admin work. Compliance, credential tracking, employer coordination, insurance, payroll support, and records management are not optional, and if they run ahead of cohort growth, EBITDA gets squeezed fast. One clean rule: if overhead rises faster than seat occupancy, the owner’s draw gets delayed.

Track admin cost per filled seat

Measure overhead per active apprentice, compliance hours per employer, and payroll support load. The key inputs are filled seats, sponsor count, renewal rate, and records volume. If a new cohort does not lift revenue enough to cover the extra admin, the extra headcount just lowers margin.

Test optional overhead against cohort growth and EBITDA impact before hiring. Keep a simple monthly check on fixed overhead, compliance backlog, and employer service time. If a process can’t be tied to seat growth, renewal support, or risk reduction, it should wait.

6

Compare low, base, and high owner-income scenarios

Owner income scenario table

Owner income moves with occupancy, sponsor conversion, and how fast cohorts fill. The base case tracks the model's 45% to 90% occupancy path, while the high case assumes stronger renewals and better utilization.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | Owner income stays close to salary only because cohort fill is weak and sponsor conversion is slow. | Owner income follows the model's planned ramp, with salary plus modest distributions after reserves and reinvestment. | Owner income rises faster when cohorts fill, renewals improve, and distributions can follow stronger cash flow. |

| Typical setup | Occupancy runs below the model path, recruiting friction stays high, reserves stay tight, and most cash goes to payroll and delivery costs. | Occupancy moves from 45.0% to 90.0%, monthly fees rise from $450 to $700, revenue scales from $9.815M to $182.142M, and EBITDA rises from $7.041M to $153.181M. | Filled cohorts, better completion, and higher instructor use lift revenue and margin while the owner keeps salary at $145,000 and takes distributions only after taxes, debt, reserves, and reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyTight cash | Salary plus modest distributionsModeled base | Salary plus larger distributionsUpside fill |

| Best fit | Use this to stress-test the business if hiring takes longer and enrolled apprentices lag plan. | Use this as the main planning case for budgeting, staffing, and cash reserve targets. | Use this to test upside if placement volume and retention outperform the base plan. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Apprenticeship Training Program Porter's Five Forces Analysis

- Apprenticeship Training Program BCG Matrix

- Apprenticeship Training Program Business Model Canvas

- What Are The 5 Core KPIs For Apprenticeship Training Program Business?

- Apprenticeship Training Program Business Plan Template in Pre-Written Word

- How Increase Apprenticeship Training Program Profitability?

- What Are Operating Costs For Apprenticeship Training Program?

- Apprenticeship Training Program Startup Costs: $955K Cash Need

- Apprenticeship Training Program Financial Model Template in Excel

- How To Start An Apprenticeship Program In 4 To 9 Months

- How To Write Apprenticeship Training Program Business Plan?

- Apprenticeship Training Program Marketing Mix

- Apprenticeship Training Program Marketing Plan

- Apprenticeship Training Program Business Proposal

- Apprenticeship Training Program PESTEL Analysis

- Apprenticeship Training Program Pitch Deck Example Editable PPTX

- Apprenticeship Training Program Business SWOT Analysis

- Apprenticeship Training Program Value Proposition Canvas

Frequently Asked Questions

The model supports a $145,000 annual Executive Director salary if the owner fills that role and cash flow holds EBITDA ranges from $7041M in Year 1 to $153181M in Year 5, but that is not owner take-home Taxes, debt service, reserves, reinvestment, and distributions come after operating profit