Owner income$115k base

Owner income$115k baseHow Much Aquatics Facility Management Owners Make at $32M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$115k base  Net margin-40% to 29%

Net margin-40% to 29% Revenue for target pay$393k

Revenue for target pay$393k Business difficultyHard

Business difficultyHard

An aquatics facility management owner can target a $115,000 operator salary in this model, but distributions depend on profit and cash reserves The business shows $548,000 revenue and negative $218,000 EBITDA in Year 1, then reaches breakeven around Month 16 By Year 5, revenue reaches $3203 million and EBITDA reaches $938,000, before taxes, debt service, reinvestment, and owner distributions These are researched planning assumptions, not guaranteed owner income

Owner income$115k baseNet margin-40% to 29%Revenue for target pay$393kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only; not guaranteed salary, tax advice, or owner distribution advice.

Need the full forecast view for owner income?

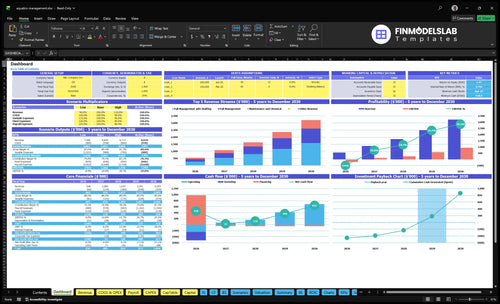

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Aquatics Facility Management Financial Model Template; open the model.

Owner-income model highlights

- Contract mix changes owner pay

- EBITDA runs -$218K to $938K

- Payback takes 47 months

Can seasonal pool management support full-time income?

Aquatics Facility Management can support full-time income, but it is not passive and the cash timing is rough. Seasonal outdoor pools create uneven receipts, payroll starts before collections catch up, and this model needs $438,000 of minimum cash to hold the line, with breakeven in Month 16. Owner-operated work can preserve the $115,000 General Manager salary if the owner fills that seat, while manager-led setups add payroll but can free up capacity.

Cash timing

- $438,000 minimum cash needed

- Month 16 breakeven timing

- Payroll rises before cash arrives

- Seasonal pools create off-season gaps

Operating model

- Owner can fill the GM role

- $115,000 salary can stay in-house

- Manager-led models add payroll cost

- Indoor contracts smooth revenue

How many pool management contracts to make $100k?

To make $100,000 from Aquatics Facility Management, plan on roughly 4 average contracts before overhead, but closer to 20+ contracts after non-owner wages, fixed overhead, and marketing; see How Much To Start Aquatics Facility Management Business? for startup cost context. Here’s the quick math: $3,043 monthly weighted revenue × 12 = $36,510 annual revenue, with about $29,800 contribution left after chemical and fleet costs.

Contract Math

- Use $100,000 target-pay logic

- Average contract revenue: $36,510/year

- Average contribution: $29,800/year

- Owner-pay break-even: about 4 contracts

Volume Reality

- Model mix: 45% maintenance contracts

- Add 35% full management contracts

- Add 20% staffing contracts

- With overhead, expect 20+ contracts

Which contract pricing model creates better owner income?

Aquatics Facility Management usually creates better owner income with staffing-heavy cost-plus contracts, because Year 1 pricing can be $7,500 per month versus $1,250 for maintenance. Fixed fee can pay more when labor, chemicals, and repairs stay under plan, but the owner absorbs overruns. Cost-plus protects margin by reimbursing payroll and direct costs, so the real upside comes from clear payroll reimbursement, maintenance markup, and performance incentives.

Fixed fee upside

- Higher margin if costs stay low

- Owner keeps savings on labor

- Chemicals and repairs stay in plan

- Overruns hit owner income fast

Cost-plus income

- $7,500 monthly Year 1 pricing

- $1,250 maintenance baseline

- Payroll reimbursement protects margin

- Markup and incentives lift owner income

Want the six owner-income drivers?

1

$1.25K-$7.5KService Mix

More full management and staffing work lifts the monthly contract value fast, but it also adds labor and service load.

2

$548K-$3.2MVolume Ramp

Winning more sites is the real growth engine, since revenue rises from $548K in Year 1 to $3.2M in Year 5.

3

2-9 FTEStaffing Load

The lead tech team scales from 2 to 9 FTE, so labor control decides how much revenue turns into owner cash.

4

10%-12%Chem Margin

Chemicals and replacement parts fall from 12% to 10% of sales, and that margin gain drops straight to EBITDA.

5

$11.6K/moOverhead Burn

Fixed overhead runs about $11.6K a month, so every extra dollar of gross profit helps fund take-home.

6

$438KCash Buffer

Minimum cash of $438K shows how much working capital the business needs before owner draws get safe.

Aquatics Facility Management Core Six Income Drivers

Contract Count and Facility Mix

Contract Count and Facility Mix

More contracts lift recurring revenue, but the mix decides how much reaches the owner. In Year 1, monthly fees range from $1,250 for maintenance and chemical work to $7,500 for full management with staffing, a 6x spread. Staffing contracts rise from 20% of customers in Year 1 to 40% in Year 5, so revenue can grow fast, but labor, supervisor coverage, and account handling get heavier too.

Here’s the quick math: contract count times fee mix drives monthly revenue. What this hides is payroll risk. If scheduling or supervision falls behind, the owner can book more revenue and still see weaker cash flow because staffed sites need more people, more checks, and tighter control.

Track mix before chasing volume

Watch active contracts, staffing share, and monthly fee by tier. The key inputs are contract count, service type, and how much account management each site needs. If the mix moves toward full-service work, price and staff for coverage first, not after margins start slipping.

Use a simple rule: if the next staffed contract needs more supervisor time than your current team can cover, delay the win or raise the fee. That protects gross margin and helps keep owner pay from getting eaten by overtime, rework, and missed service.

- Track fee by service tier

- Track staffing share monthly

- Match supervisors to site load

- Price for added complexity

1

Contract Pricing and Revenue Model

Contract Pricing and Margin

This income driver is the monthly fee structure. In aquatics facility management, fixed fees create upside when labor, chemicals, and repairs stay under budget, while cost-plus pricing protects against cost spikes but caps profit. By Year 5, service tiers reach $1,510, $3,400, and $9,115 per month, so small pricing gaps can change the owner’s draw across every contract.

Here’s the quick math: if one tier is priced too low, the loss repeats every month and every season. The key inputs are active contracts, tier mix, labor hours, chemical use, repair pass-throughs, and staffing markups. What this estimate hides is overage risk; if costs are not tracked by contract, a strong top-line fee can still shrink cash flow and profit.

Track Tier Price and Add-On Margin

Track each contract by tier, then split out maintenance, chemicals, staffing, and repairs. That shows where fixed fees are creating margin and where cost-plus only breaks even. If staffing is billed, keep the markup separate from core service so you can see the real gross margin and protect owner pay.

Test pricing against actual labor and chemical cost per site, not company averages. A $100 monthly miss per contract becomes $1,000 across 10 contracts, and it compounds through peak season. Use a monthly dashboard for billed fee, direct cost, and gross margin by contract so weak tiers get repriced fast.

- Track billed fee by tier.

- Separate staffing markups.

- Review direct cost monthly.

- Reprice weak contracts fast.

2

Staffing Economics

Lifeguard Staffing Cost

Staffing economics is the gap between what clients pay for coverage and what it really costs to fill every shift. The labor line only helps income if billable rates cover guard wages, supervisor pay, recruiting, training, overtime, and no-shows. With salaried roles like $55,000 for a Lifeguard Supervisor and $68,000 for a Lead Service Technician, total wages rise from $416,000 in Year 1 to $1.174 million in Year 5, so missed coverage can turn revenue into leakage fast.

Here’s the quick math: if staffing is sold as a fixed monthly fee, every unpaid overtime hour and every empty post hits gross margin and cash flow at once. One clean shift schedule can protect owner pay; one weak week can erase it.

Price for Full Coverage

Track billable labor rate against fully loaded labor cost, not just guard wages. Include supervisor time, recruiting, training, overtime, and backup labor so the rate per covered hour stays above true cost. If the spread is thin, staffing becomes a cash drain even when the contract looks big.

- Measure cost per billed hour

- Flag overtime above plan

- Price no-show coverage separately

- Review supervisor span weekly

What this estimate hides is the chaos cost: one missed shift can create safety risk, client churn, and extra admin time. If coverage depends on last-minute fixes, owner income drops long before revenue does.

3

Maintenance, Chemicals, and Repair Margin

Maintenance and Repair Margin

This driver covers chemicals, replacement parts, preventive visits, and repair coordination. Here’s the quick math: 120% cost on $1.00 of related revenue leaves -$0.20 before labor; by Year 5, 100% cost is only break-even. With the maintenance and chemical mix falling from 45% to 25%, this line protects cash more than owner pay unless markups are tight.

Emergency calls and rush parts can wipe out the spread fast. If preventive work is weak, overtime and same-day buying turn a small margin into leakage. The owner’s income improves when repair coordination is priced cleanly and every pass-through charge is billed at the stated markup, not absorbed inside the monthly fee.

Track the Spread

Measure chemical spend, parts spend, repair labor hours, and the markup on each ticket by contract. The key inputs are active customers, service mix, and how often work is preventive versus emergency. If a contract needs heavy site visits but the bill still reads like a simple maintenance account, take-home income falls even when revenue looks steady.

Set a separate price for repair coordination and keep pass-through items outside the base service fee. One clean rule helps: if a buy costs more than the bill shows, margin is gone. Track monthly gross margin by line, then push any account with repeated rush buys or low markup into a higher tier or a tighter scope.

4

Seasonality and Facility Mix

Seasonal Cash Flow Mix

If your book is heavy on summer pool work, cash will spike when pools are open but payroll, chemicals, and supervisor coverage still land every month. That’s why the model shows a $438,000 minimum cash need and Month 16 breakeven; summer profit can look strong while owner pay stays tight.

Indoor pool and institutional contracts smooth revenue across winter, improve payroll planning, and cut the risk of hiring too early. The real test is mix, not just contract count: year-round accounts protect cash flow, while seasonal work needs a larger reserve and tighter draw control.

Balance the Calendar

Track revenue by facility type, month, and staffing load. Split the book into seasonal outdoor, indoor year-round, and institutional work so you can forecast payroll against the weakest cash months. Here’s the quick math: if the business still needs $438,000 of cash support, summer sales are not free profit.

- Track cash by month and facility type.

- Delay owner draws until reserves build.

- Hire to booked hours, not peak demand.

- Use indoor contracts to flatten payroll.

What this estimate hi des: fast summer growth can force overtime, onboarding strain, and delayed pay if the off-season pipeline is thin. Keep a reserve tied to the Month 16 breakeven path, and use recurring indoor work to protect margin when seasonal revenue falls.

5

Overhead, Insurance, and Owner Role

Overhead, insurance, and owner role

When fixed overhead is $11,600 per month plus $45,000 of Year 1 marketing, owner pay only comes from EBITDA, or operating profit before interest, taxes, depreciation, and amortization, left after those bills. Rent is $6,500, general liability insurance is $2,200, and portal support is $1,100, so a big chunk of cash is gone before labor or reserves. One clean rule: overhead sets the floor under owner income.

Owner-operated income can also include a $115,000 General Manager role, but only if the owner is truly doing the work and the business still funds reserves. Reserves are planning protection, not optional profit, especially when payroll and contract volume scale. If overhead grows faster than EBITDA, the owner’s draw gets squeezed fast.

Track overhead before you draw

Measure monthly overhead as a share of EBITDA, then compare it with active contracts, payroll, and marketing spend. Here’s the quick check: if fixed costs stay at $11,600 and marketing steps from $45,000 to $135,000, the business needs enough recurring margin to fund growth and owner pay at the same time.

- Track rent, insurance, portal, admin monthly

- Separate reserves from owner draw

- Price for GM labor if used

- Review cash needs before expansion

If the owner fills the $115,000 General Manager seat, document that role separately so profit is not overstated. Otherwise, the business can look healthy on paper while cash for tax, claims, or slow collections is too thin.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with ramp speed, staffing load, and margin. Early months are cash tight, while later years create more room for draws after reserves.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the early ramp case, where owner pay is strained until outside funding closes the gap. | This is the modeled operating case, where the business can start supporting limited owner distributions. | This is the stronger scale case, where the owner can take more cash after reserves and reinvestment. |

| Typical setup | Year 1 reaches $548,000 revenue, with -$218,000 EBITDA, about -39.8% EBITDA margin, $45,000 marketing, and $416,000 wages, so owner salary only works if funded. | Year 3 reaches $1,637,000 revenue, with $240,000 EBITDA, about 14.7% EBITDA margin, $85,000 marketing, and $737,000 wages, so distributions stay limited after reserves. | Year 5 reaches $3,203,000 revenue, with $938,000 EBITDA, about 29.3% EBITDA margin, $135,000 marketing, and $1,174,000 wages, so distribution capacity is stronger. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No stable drawCash gap | Limited draw capacityReserve draw | Stronger draw capacityUpside case |

| Best fit | Use this to stress test the business if sales land slowly and cash stays tight. | Use this as the main planning case for normal execution and modest owner income. | Use this to test upside if staffing stays disciplined and the client base scales cleanly. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Aquatics Facility Management Porter's Five Forces Analysis

- Aquatics Facility Management BCG Matrix

- Aquatics Facility Management Business Model Canvas

- What Are The 5 KPI Metrics For Aquatics Facility Management Business?

- Aquatics Facility Management Business Plan Template in Pre-Written Word

- How Increase Aquatics Facility Management Profits?

- What Are Operating Costs For Aquatics Facility Management?

- Aquatics Facility Management Startup Costs: $438K Cash Need

- Aquatics Facility Financial Model Template in Excel

- How To Open An Aquatics Facility Management Business In 8–16 Weeks

- How Do I Write An Aquatics Facility Management Business Plan?

- Aquatics Facility Management Marketing Mix

- Aquatics Facility Management Marketing Plan

- Aquatics Facility Management Business Proposal

- Aquatics Facility Management PESTEL Analysis

- Aquatics Facility Management Pitch Deck Example Editable PPTX

- Aquatics Facility Management Business SWOT Analysis

- Aquatics Facility Management Value Proposition Canvas

Frequently Asked Questions

The model supports a $115,000 operator salary if the owner fills the General Manager role, but distributions depend on profit and cash Year 1 EBITDA is negative $218,000 on $548,000 revenue By Year 5, EBITDA reaches $938,000 on $3203 million revenue before taxes, debt service, reserves, and reinvestment