Owner income$130k base

Owner income$130k baseAsbestos Removal Owner Income: $130K Salary And 8-Month Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$130k base  Net margin73% to 81%

Net margin73% to 81% Revenue target~$178k

Revenue target~$178k Business difficultyHard

Business difficultyHard

An asbestos removal business owner can model $130,000 in pre-tax salary from the CEO / Lead Project Manager role, while business profit depends on volume, crew use, and compliance costs In the researched case, EBITDA, meaning operating profit before interest, taxes, depreciation, and amortization, is -$50,000 in Year 1, then rises to $629,000 in Year 2 and $6984 million in Year 5 That does not mean the owner should pull all profit out The model also needs $619,000 minimum cash in Month 7, a 22-month payback, and reserves for payroll, disposal, insurance renewals, equipment, and slow periods

Owner income$130k baseNet margin73% to 81%Revenue target~$178kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, marketing, reserves, and target pay.

Planning note: Research-based planning estimate only; it is not guaranteed salary, tax advice, or owner distribution advice.

Want to stress-test owner income in Asbestos Removal?

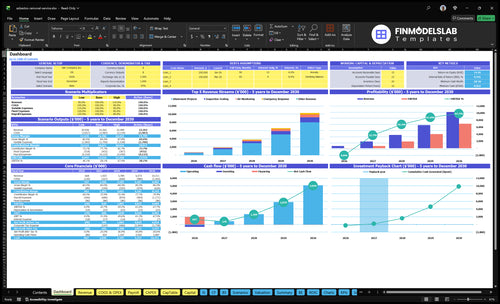

This dashboard shows revenue, EBITDA, cash, breakeven, and owner salary in the Asbestos Removal Financial Model Template.

Owner-income model highlights

- Owner salary and take-home

- Year 1 EBITDA: -$50,000

- Year 2 EBITDA: $629,000

- Year 5 EBITDA: $6,984 million

- Month 7 cash: $619,000

- Month 8 breakeven

- 22-month payback, IRR 0.09

- ROE 1,426%

- Prices, hours, CAC, capex

Is an asbestos removal business profitable, and how do you scale it?

Asbestos Removal can be profitable, but only when licensed crew capacity, pipeline, pricing, safety systems, insurance, and cash reserves all line up. The model shows Month 8 breakeven, a 22-month payback, and Year 1 EBITDA of -$50,000 before rising to $629,000 in Year 2. The hard part is cash and staffing: it needs $619,000 minimum cash in Month 7, $230,000 startup capex, and growth is not simple revenue multiplication.

Profit drivers

- Month 8 breakeven

- 22-month payback

- $629,000 Year 2 EBITDA

- 3 field FTEs in Year 1

Scale risks

- $619,000 cash need in Month 7

- $230,000 startup capex

- 9 field FTEs by Year 5

- Insurance, downtime, compliance load

How much revenue does an asbestos removal business need to pay the owner?

For Asbestos Removal, plan on about $660,000 in Year 1 revenue to pay a $130,000 owner salary. With 27% direct costs, you keep a 73% gross margin, but that still has to cover $191,000 technician payroll, $48,000 admin pay, $86,400 fixed overhead, and $25,000 in marketing, so the target lands at about $658,000 before reserves and the $230,000 startup capex.

Year 1 math

- $130,000 owner salary

- $191,000 technician payroll

- $48,000 admin salary

- $86,400 fixed overhead

What pushes revenue up

- 27% direct-cost load cuts margin

- $25,000 Year 1 marketing adds pressure

- $230,000 capex needs cash too

- Lower utilization means more sales

What affects asbestos removal profit margins?

Asbestos removal margins come down to direct job cost control and scope accuracy: in Year 1, direct job costs are 27% of revenue, then fall to 19% by Year 5 as disposal, materials, subcontractors, and commissions drop. For launch budgeting, see What Is The Estimated Cost To Open And Launch Your Asbestos Removal Business? The biggest leaks are containment labor overruns, PPE use, negative air setup, air monitoring coordination, waste transport, landfill fees, insurance, rework, and documentation delays, so safety and compliance stay non-negotiable.

Cost mix

- 10% disposal fees in Year 1

- 8% equipment and consumables

- 5% project subcontractors

- 4% commissions and bonuses

Margin risks

- Containment labor overruns

- PPE and negative air setup

- Air monitoring and waste transport

- Rework and documentation delays

Want the six levers that drive owner income?

1

CAC $1.25K-$800Lead Flow

Cut CAC from $1.25K in Year 1 to $800 by Year 5, so each won job keeps more cash after sales spend.

2

$6K-$10.2KProject Value

Raise average abatement project value from $6,000 to $10,200, and owner take-home rises faster than headcount.

3

40-60 hrsCrew Use

Push billable abatement hours from 40 to 60, so each crew day produces more revenue before overtime or new hires.

4

73%-81%Job Margin

Lift gross margin from 73% to 81% by holding disposal, materials, and subcontractor costs in check.

5

$7.2K/moOverhead

Keep fixed overhead near $7.2K a month, because insurance, permits, and back-office costs hit cash every month.

6

$619KCash Buffer

Hold at least $619K in cash, since $230K of startup capex and slow payback mean owner pay should stay separate from distributions.

Asbestos Removal Core Six Income Drivers

Project Volume And Lead Flow

Project Volume And Lead Flow

More qualified abatement, inspection, air monitoring, emergency, renovation, demolition, and referral jobs lift revenue only when licensed crews can finish them safely. With $25,000 of marketing in Year 1 and $1,250 CAC, that implies about 20 projects; by Year 5, $110,000 and $800 CAC imply about 138 projects, before capacity limits.

The owner’s take-home rises only when volume matches crew capacity. If lead flow outruns field staffing, overtime, rework, and compliance risk can eat the margin fast, so more jobs do not always mean more profit.

Track CAC Versus Crew Load

Measure qualified leads, CAC, booked jobs, and licensed crew hours each week. Lower CAC improves pipeline efficiency, but the real test is whether each added project can be completed without overtime or safety shortcuts, especially on inspection-referred abatement and emergency response work.

- Track leads by source.

- Track booked jobs by type.

- Cap sales at crew capacity.

- Watch overtime and rework.

- Price rush work separately.

If lead flow grows but field hours do not, profit usually leaks into payroll and compliance costs instead of owner distributions.

1

Average Project Value

Average Project Value

Average project value is the dollar size of each completed job. For asbestos abatement, bigger tickets lift revenue fast: abatement projects rise from $6,000 in Year 1 to $10,200 in Year 5, emergency response from $4,000 to $6,900, inspection from $960 to $1,350, and air monitoring from $660 to $1,000.

Here’s the quick math: that is a $4,200 jump for abatement, $2,900 for emergency response, $390 for inspection, and $340 for air monitoring. Income only improves if the scope is right and crews stay productive, because higher value also brings more labor, containment, disposal, documentation, and testing coordination cost.

Price the Full Scope

Track quoted value, actual labor hours, disposal cost, and testing coordination time by job type. Break out inspection, removal, air monitoring, and emergency work so you can see which jobs raise gross margin and which just add workload. A higher hourly rate helps only when waste and containment needs are priced in.

- Project mix

- Waste volume

- Containment needs

- Documentation steps

- Testing handoffs

If a bid misses any of those inputs, owner pay gets hit twice: first in lower gross margin, then in cash flow when unplanned labor and disposal bills land before the client pays.

2

Crew Utilization And Labor Productivity

Crew Utilization

If your licensed crews sit idle, payroll keeps running but revenue does not. In this business, owner income improves when each project carries steady billable hours, less downtime, and fewer scope misses. A practical shift from 40 to 60 billable hours per project lifts labor productivity, which supports more gross margin and better distributions after salary.

One clean rule: pay for motion, not waiting. Compliance time, decontamination, PPE setup, containment, and records are real production costs, so they must be built into scopes. If the field mix grows from 2 entry technicians plus 1 senior technician in Year 1 to 6 entry technicians plus 3 senior technicians in Year 5, the owner needs enough project flow and pricing to keep that larger team fully used.

Track Billable Hours Per Crew

Measure utilization as billable hours divided by paid field hours, then compare it by project type. If the ratio drops, you are carrying payroll on non-billable time. If the ratio rises too fast, rushed crews can create safety and rework costs, which still hit profit.

- Track billable hours by project

- Log downtime and rework separately

- Price for compliance time up front

- Staff to match scope, not hope

What matters most is the spread between planned hours and actual hours. Accurate scopes, tight dispatch, and less waiting on containment or testing keep crews productive and protect the cash that turns into owner pay.

3

Direct Job Cost Control

Direct Job Cost Control

Direct job costs decide gross margin, and gross margin decides how much cash is left for payroll, overhead, reserves, and owner pay. In asbestos removal, the big levers are disposal fees, equipment and consumables, subcontractors, and commissions or bonuses. If those move from 27% of job revenue to 19%, gross margin improves by 8 points.

That matters fast. A few points of waste in PPE, containment material, transport, or landfill charges can erase profit on a project. Here’s the quick math: every $100,000 of revenue with an 8-point cost drop creates about $8,000 more gross profit before fixed overhead. Cost control must not cut safety or legal steps.

Track the cost stack weekly

Measure each job by disposal fees, equipment and consumables, subcontractors, and commissions or bonuses. Watch whether disposal falls from 10% to 8%, equipment from 8% to 6%, subcontractors from 5% to 3%, and commissions from 4% to 2%. Those are the inputs that move owner take-home income.

- Track waste loads and landfill tickets.

- Separate rented gear from consumables.

- Approve subcontracted testing upfront.

- Price containment and PPE by scope.

- Compare budgeted versus actual job cost.

Use job-level cost reports, not just monthly totals. If negative air equipment, containment supplies, protective gear, or transport run high, fix the estimate or the process before the next bid. Tight control protects cash for payroll and owner pay, but it should never pressure crews to skip decontamination, documentation, or disposal rules.

4

Insurance, Licensing, Compliance, And Overhead

Insurance, Licensing, And Overhead

For asbestos removal, required overhead cuts owner pay even when project margins look fine. The disclosed fixed costs are $1,500 for general liability and pollution insurance, $300 for licensing and permits, $200 for training and certifications, and $800 for accounting and legal, with $7,200 per month total fixed overhead . That is $86,400 per year before owner distributions.

Here’s the quick math: the listed compliance items total $2,800 per month, so the rest of the overhead bucket is $4,400 in other fixed costs like vehicles, admin, workers’ comp, training, and medical surveillance. If those costs rise and revenue stays flat, distributable cash shrinks fast. Cleaner compliance systems protect margin by reducing rework, delays, and permit problems.

Track Compliance Cost Per Month

Measure this driver as a monthly overhead ratio against revenue and gross profit. Track insurance, permits, certifications, accounting/legal, and the other fixed items inside the $7,200 base. Keep a separate line for workers’ comp, medical surveillance, and vehicles so you can see which costs are permanent and which move with crew count.

Use the data to price jobs with overhead in mind, not after the fact. If licensing renewals, training, or admin hours climb, raise your overhead allocation per project and check owner draw timing. One clean rule: if compliance spend rises faster than revenue, distributions should wait until the cash gap is covered.

5

Cash Reserves And Reinvestment Discipline

Cash Reserves And Owner Pay

Accounting profit does not mean safe owner distributions. This business needs cash to cover payroll timing, insurance renewals, waste bills, equipment replacement, and slow months. The model shows a $619,000 minimum cash need in Month 7, $230,000 startup capex, Month 8 breakeven, and a 22-month payback, so owner draws should stay conservative until cash is durable.

- $40,000 specialized equipment

- $70,000 vehicles

- $30,000 decontamination units

- $25,000 air monitoring devices

- $15,000 PPE inventory

- $10,000 containment materials

- $20,000 office and IT

- $12,000 licensing and permits

- $8,000 digital presence

Track cash by month, not just profit. The key inputs are job timing, gross margin, fixed overhead, and replacement spending. If collections slip or a big waste bill hits before receivables clear, owner pay can stop even in a profitable month.

Reserve Before You Reinvest

Keep a cash floor before taking draws. Set a reserve equal to the worst timing gap, then fund capex only after that floor is intact. In practice, that means matching new spending to cash from completed jobs, not to booked revenue. If payroll, insurance, or disposal bills spike, reinvestment has to pause so owner income stays protected.

- Track cash weekly.

- Separate reserve and operating cash.

- Delay draws before big renewals.

- Replace gear from excess cash only.

The fastest control is a 13-week cash forecast. It shows when a strong margin still won’t fund distributions because cash is trapped in receivables, equipment spend, or mobilization costs.

6

Compare low, base, and high owner income planning scenarios

Owner income scenarios

Owner income changes because early losses, then reserve-first growth, then a scaled operation change what can be paid out beyond the $130,000 salary.

| Scenario | Low CaseEarly strain | Base CaseManaged growth | High CaseScaled upside |

|---|---|---|---|

| Launch model | The low case is a thin early-ramp model with negative EBITDA and no owner distributions. | The base case is a modeled growth path with profits building before any owner payout. | The high case is a mature model with strong EBITDA and strict reserve discipline before any payout. |

| Typical setup | Year 1 starts with a $130,000 owner salary, -$50,000 EBITDA, 73% gross margin, $25,000 marketing, a $1,250 CAC, 3 field technicians, and no planned distributions. | Year 2 pairs a $130,000 owner salary with $629,000 EBITDA, 75% gross margin, $40,000 marketing, a $1,000 CAC, added Operations Manager and Sales & Marketing Coordinator roles, and payouts only after reserves. | Year 5 pairs a $130,000 owner salary with $6,984,000 EBITDA, 81% gross margin, $110,000 marketing, an $800 CAC, 9 field technicians, and strict reserve discipline before any payout. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $130,000 salarySalary only | $130,000 salaryReserve first | $130,000 salaryMature scale |

| Best fit | Use this to stress-test early cash strain and a slow ramp. | Use this as the core planning case for a growing, controlled operation. | Use this to test upside in a fully built operation with tighter cash control. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Asbestos Removal Porter's Five Forces Analysis

- Asbestos Removal BCG Matrix

- Asbestos Removal Business Model Canvas

- 7 Critical KPIs for Scaling Your Asbestos Removal Business

- Asbestos Removal Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Asbestos Removal Profitability

- How Much Does It Cost To Run An Asbestos Removal Business Monthly?

- Asbestos Removal Startup Costs: Plan For $619K Minimum Cash

- Asbestos Removal Financial Model Template in Excel

- How To Start An Asbestos Removal Business In 3 To 6+ Months

- How to Write an Asbestos Removal Business Plan in 7 Steps

- Asbestos Removal Marketing Mix

- Asbestos Removal Marketing Plan

- Asbestos Removal Business Proposal

- Asbestos Removal PESTEL Analysis

- Asbestos Removal Pitch Deck Example Editable PPTX

- Asbestos Removal Business SWOT Analysis

- Asbestos Removal Value Proposition Canvas

Frequently Asked Questions

The model carries a $130,000 pre-tax CEO / Lead Project Manager salary Business EBITDA is -$50,000 in Year 1, then $629,000 in Year 2 and $6984 million in Year 5 Owner distributions depend on cash, reserves, debt service, taxes, and reinvestment, so EBITDA should not be treated as automatic take-home pay