Owner income$67k to $963k

Owner income$67k to $963kHow Much Does An Asian Fusion Restaurant Owner Make? $67K–$963K

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$67k to $963k  Net margin10.4% to 50.0%

Net margin10.4% to 50.0% Revenue for target pay$642k to $1.925m

Revenue for target pay$642k to $1.925m Business difficultyHard

Business difficultyHard

An Asian fusion restaurant owner could plan around $67k of Year 1 EBITDA as the pre-tax, pre-debt owner-pay pool, rising to $272k in Year 2 and $963k by Year 5 under the researched model That is not the same as automatic take-home pay Owner income depends on covers, average check, food cost, labor, rent, technology and delivery fees, marketing, reserves, and whether the owner replaces paid management labor The model reaches breakeven in Month 4, but it also shows a $802k minimum cash need in Month 2, so early draws should stay cautious

Owner income$67k to $963kNet margin10.4% to 50.0%Revenue for target pay$642k to $1.925mBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, labor, reserves, financing, and taxes not modeled here.

Want to check owner income in the model?

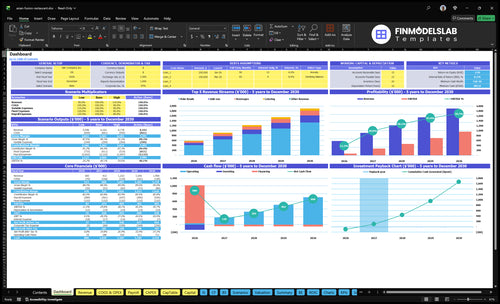

The Asian Fusion Restaurant Financial Model Template ties dashboard, sales assumptions, menu mix, COGS, payroll, overhead, capex, cash flow, scenarios, and owner income into one view. It also shows revenue from $642k to $1.925m, EBITDA from $67k to $963k, breakeven in Month 4, minimum cash of $802k in Month 2, and payback at 20 months.

Owner-income model highlights

- Owner pay is built in

- Revenue and EBITDA charts

- Breakeven and cash timing

How much revenue does an Asian fusion restaurant need to pay the owner?

An Asian Fusion Restaurant needs enough revenue to cover $1.22M in fixed overhead, rising payroll from $250k in Year 1 to $419k in Year 5, and still leave room for owner pay and reserves. In the model, $6.422M of revenue produced only $67k EBITDA in Year 1, while $9.253M produced $272k EBITDA in Year 2, so sales alone do not equal cash for the owner. Here’s the quick math: target owner pay ÷ EBITDA margin, then add a reserve cushion.

Revenue drives pay

- $6.422M revenue = $67k EBITDA

- $9.253M revenue = $272k EBITDA

- Fixed overhead is $1.22M/year

- Payroll rises to $419k by Year 5

Covers and cash

- Weekly covers grow from 645 to 1,605

- Owner pay comes after labor and rent

- Delivery fees can cut margin fast

- Reserves matter if costs rise

How does owner involvement change Asian fusion restaurant income?

Owner involvement can make income look higher because the owner is doing kitchen, purchasing, scheduling, or front-of-house work instead of paying someone else. In the manager-run case, payroll already includes a $68k store manager and a $58k head chef from Month 1 Year 1, and total payroll is $250k before any separate owner salary. So when paid management replaces owner labor, distributions fall even if the restaurant stays profitable, while hands-on owners may save on waste and buying but can also hit burnout and slow growth.

Chef-owner or floor-owner

- Hides unpaid labor in income

- Can cut waste and buying errors

- May raise take-home cash flow

- Burnout can cap growth

Absentee or manager-run

- $68k store manager starts at Month 1

- $58k head chef starts at Month 1

- Total payroll hits $250k

- Owner distributions drop

How much can a new Asian fusion restaurant owner make?

A new Asian Fusion Restaurant owner can make up to about $67k in Year 1 EBITDA, but that’s the upper pre-tax, pre-debt owner-pay pool—not automatic take-home cash; track guest sentiment early with What Is The Current Customer Satisfaction Level For Your Asian Fusion Restaurant? because weak reviews can cut repeat covers fast. Year 1 sales are about $642.2k from 645 weekly covers, with $18 midweek and $20 weekend average order values.

Owner pay reality

- Treat $67k EBITDA as the ceiling

- Subtract taxes, debt, and reserves

- Break-even hits in Month 4

- Early draws can starve operations

Cash pressure points

- Minimum cash need peaks at $80.2k

- Peak cash gap lands in Month 2

- Startup capex totals $136.5k

- Hiring, inventory, marketing, repairs limit draws

What drives owner income most?

1

645-1,605/wkCover Volume

Weekly covers rise from 645 in year 1 to 1,605 in year 5, and that is the biggest swing in owner income because it drives total revenue from $642K to $1.925M.

2

$18-$24Check Mix

Average check moves from $18 on midweek days to $24 on weekends, and more add-ons and beverages raise revenue without needing more seats.

3

12%-10%Food Cost

Fish, produce, ingredients, and packaging run at 12% of sales in year 1 and 10% by year 5, so buying and prep discipline protects gross margin.

4

39%-24%Labor Schedule

Labor is about 39% of year 1 revenue and 24% of year 5 revenue, so staffing to traffic keeps profit from getting squeezed.

5

$10.18K/moFixed Overhead

Rent, utilities, insurance, and core admin stay fixed at $10,180 a month, so once sales cover that base, extra volume falls through to EBITDA.

6

5%-10%Channel Mix

Catering grows from 5% of sales in year 1 to 10% in year 5, and those larger orders help spread fixed costs across more revenue.

Asian Fusion Restaurant Core Six Income Drivers

Cover Volume

Cover Volume

Covers means guest meals served. This driver sets the revenue base before pricing or cost control matters. In this model, weekly covers rise from 645 in Year 1 to 1,605 in Year 5, so volume is about 2.5x higher. Saturday goes from 150 to 350 covers, and Friday from 120 to 280.

More lunch and dinner traffic can raise owner income, but only if the room, kitchen, and cleaning flow keep up. Reservations, table turns, counter throughput, and catering pickup timing all shape the count. If volume climbs without staffing discipline, overtime and waste can erase the gain. One clean rule: more guests help only when service stays smooth.

Track Covers by Daypart

Measure covers by lunch, dinner, Friday, and Saturday so you can see where growth is real. Tie each shift to labor hours, prep output, and ticket times. The key inputs are reservations, walk-ins, table turns, and pickup windows. If 1,605 weekly covers is the target, staffing has to match that pace.

- Track covers per shift.

- Watch labor hours per cover.

- Log waste and overtime.

- Adjust staffing before peaks.

Use the data to cap bad volume. If service slows, extra covers can cut owner pay instead of raising it.

1

Average Check And Menu Mix

Average Check And Menu Mix

Average check is the fastest way to lift profit per guest. In this model, midweek order value rises from $18 to $22 and weekend order value from $20 to $24, so each cover carries more gross profit before fixed costs hit. That matters because owner pay comes after food, labor, and rent; a stronger check size can raise take-home income faster than traffic alone.

This driver includes add-ons, beverages, desserts, premium proteins, and catering trays. The mix also shifts from 700% poke bowls, 150% add-ons, 100% beverages, and 50% catering in Year 1 to 600%, 180%, 120%, and 100% in Year 5. The risk is simple: if price moves outrun local value, guests may trade down or skip extras.

Track basket mix and test upsells

Measure AOV by daypart, plus attach rates for add-ons, drinks, and catering. Here’s the quick math: if midweek check size moves from $18 to $22, the same number of covers produces more revenue and more gross profit, with little added fixed cost. That extra margin is what funds owner draw.

Use menu engineering, not blanket price hikes. Test premium proteins, bundled drinks, and catering trays first, then watch whether guest count holds. If competition is tight, keep one clear value item on the menu so the higher mix feels earned, not forced.

2

Food And Beverage Cost Control

Food and Beverage Cost Control

Ingredient control protects gross margin, the share left after food and packaging. On $6.422 million revenue, every 1 percentage point of cost equals about $64,000 in annual cash, so moving fish and fresh produce from 80% to 70% of revenue matters a lot. It raises owner take-home without cheapening the concept.

The leak is usually in seafood, proteins, sauces, specialty produce, pantry items, supplier pricing, spoilage, and portion drift. If portions are loose, add-on profit disappears fast. Inconsistent plating can erase the extra cash you expected from premium items.

Track Recipe Cost and Waste

Use prep sheets, batch sauces, yield tracking, menu engineering, and waste logs to lock portion size and compare actual use to recipe cost. Watch fish, produce, and packaging separately from other ingredients, because they do not move together.

Track these inputs each week:

- Portion size by menu item

- Supplier price by ingredient

- Spoilage by prep batch

- Waste by shift

- Yield from trim to plate

Every saved point of cost drops straight to cash, so test menu prices and portions together before raising volume.

3

Labor Scheduling

Labor Scheduling

Labor scheduling covers shift timing, staffing levels, overtime, and owner labor. It is the biggest controllable operating cost after food, so small hour changes can move take-home pay fast. Payroll is listed at $250k in Year 1, $3125k in Year 2, $357k in Year 3, $3895k in Year 4, and $419k in Year 5.

The key inputs are actual covers, prep complexity, wage market, overtime, payroll taxes, and whether the owner fills shifts. Roles include a $68k store manager and $58k head chef, plus kitchen staff, counter service staff, and a catering coordinator from Year 2. Owner-filled shifts can protect cash, but they are not a long-term fix.

Schedule to Covers

Track labor hours against daily covers, not just the weekly payroll total. If lunch and dinner traffic change, the schedule should change with them, or overtime and payroll taxes eat margin. Here’s the quick math: more hours than covers means lower profit per guest; fewer hours than covers means service risk and slower tables.

Build shift templates around reservations, expected walk-ins, and catering timing. Keep owner hours separate from paid staff hours so you can see the real operating cost. That makes it easier to protect take-home income, especially when staffing a manager, chef, and fixed front-of-house roles.

4

Occupancy And Fixed Overhead

Fixed Overhead Squeeze

Fixed overhead is the rent-and-bills layer that gets paid before owner draw. Here it totals $10,180/month or $122,160/year across rent, utilities, insurance, subscriptions, accounting, cleaning, and website/app upkeep. That means the dining room has to fund these costs first, so weak sales hit take-home income fast. Fixed costs don’t wait for a good month.

Here’s the quick math: at $642k revenue, fixed overhead is about 19% of sales; at $1.925m, it drops to about 6%. So the lease burden matters most early, when each slow week can wipe out cash for the owner. Repairs, permits, maintenance, and common area charges can push that burden higher if they’re not tracked.

Control the Lease Load

Track fixed overhead as a monthly cash number and as a % of revenue. Build the estimate from the lease, utility bills, insurance policy, software invoices, accountant fees, cleaning contracts, and web/app maintenance. If occupancy rises or extra charges show up, update the forecast right away so owner pay doesn’t get set off stale numbers.

- Watch fixed cost per sales dollar.

- Flag lease escalators early.

- Reserve cash for repairs.

- Review common area charges monthly.

5

Delivery, Catering, And Private Events

Delivery, Catering, And Private Events

This driver is the profit gap between dine-in, takeout, delivery, catering trays, lunch specials, and private events. Sales can rise fast, but take-home income only improves if each channel covers labor and packaging. If technology and delivery fees sit at 40% of revenue and the goal is 30%, the margin gain matters only when prep and service stay tight.

For this model, catering mix rises from 50% to 100%, and a catering coordinator starts at 0.5 FTE in Year 2, then 1.0 FTE from Year 3. FTE means full-time equivalent. The owner earns more when events are priced to cover trays, staff time, delivery delays, and lost kitchen capacity.

Price each channel on its own margin

Track each channel separately: guest count, order value, fees, packaging, labor minutes, and delivery time. Here’s the quick test: if a catering order needs extra prep and a coordinator, the price must cover those costs before it helps owner pay. Separate margins keep strong channels from hiding weak ones.

- Measure dine-in and delivery margin separately.

- Price trays for labor and packaging.

- Watch app fees and late deliveries.

- Test lunch specials against event margins.

What this estimate hides: prep bottlenecks, app fees, and delivery delays can erase profit even when revenue grows. If catering turns into a bigger share of sales, the owner should forecast extra labor and check that each event still leaves cash after direct costs. That cash is what pays the owner.

6

Compare lean, base, and strong owner-income cases

Owner income scenarios

Owner income moves with covers, pricing, fees, and payroll. The model needs $802k minimum cash, reaches breakeven in Month 4, and pays back in 20 months.

| Scenario | Low CaseCautious draw | Base CaseStable operator | High CaseScale case |

|---|---|---|---|

| Launch model | The low case assumes a Year 1 ramp with tighter earnings and a thin cushion. | The base case models a steadier Year 3 run with better volume and pricing. | The high case assumes a stronger Year 5 run with more volume and better mix. |

| Typical setup | About 645 weekly covers, $18 midweek AOV, $20 weekend AOV, 12% COGS, 6% variable fees, and $250k payroll. | About 1,125 weekly covers, $20 midweek AOV, $22 weekend AOV, 11% COGS, 5.1% variable fees, and $357k payroll. | About 1,605 weekly covers, $22 midweek AOV, $24 weekend AOV, 10% COGS, 4.2% variable fees, and $419k payroll, with catering and add-ons doing more of the work. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $67k EBITDACautious draw | $465k EBITDAStable operator | $963k EBITDAScale case |

| Best fit | Use this to stress-test a slow ramp, higher labor drag, or tighter cash use. | Use this as the core planning case for steady traffic and a more balanced cost structure. | Use this to test upside if the owner stays hands-on, protects reserves, and keeps growth tight. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Asian Fusion Restaurant Porter's Five Forces Analysis

- Asian Fusion Restaurant BCG Matrix

- Asian Fusion Restaurant Business Model Canvas

- 7 Essential KPIs to Track for an Asian Fusion Restaurant

- Asian Fusion Restaurant Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Asian Fusion Restaurant Profitability

- How Much Does It Cost To Run An Asian Fusion Restaurant Monthly?

- Asian Fusion Restaurant Startup Costs: $1365K CAPEX Before Cash

- Asian Fusion Restaurant Financial Model Template in Excel

- How To Open An Asian Fusion Restaurant In 4–9 Months

- How to Write an Asian Fusion Restaurant Business Plan

- Asian Fusion Restaurant Marketing Mix

- Asian Fusion Restaurant Marketing Plan

- Asian Fusion Restaurant Business Proposal

- Asian Fusion Restaurant PESTEL Analysis

- Asian Fusion Restaurant Pitch Deck Example Editable PPTX

- Asian Fusion Restaurant Business SWOT Analysis

- Asian Fusion Restaurant Value Proposition Canvas

Frequently Asked Questions

The researched model shows $67k of Year 1 EBITDA and $963k by Year 5 before taxes, debt service, and owner reserves Revenue grows from $642k to $1925m over the same period Take-home can be lower if the owner keeps cash for repairs, debt payments, working capital, or expansion