Owner income$119k-$1.06M

Owner income$119k-$1.06MHow Much Does An Asian Restaurant Owner Make? $119k-$1064M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$119k-$1.06M  Net margin2.8%-6.2%

Net margin2.8%-6.2% Revenue for target pay$4.21M-$17.20M

Revenue for target pay$4.21M-$17.20M Business difficultyHard

Business difficultyHard

You’re trying to see what owner take-home can look like before you sign a lease or hire staff In this five-year researched model for a US Asian restaurant, annual revenue rises from about $421k in Year 1 to $172M in Year 5, with EBITDA from $119k to $1064M before taxes, debt payments, reserves, and owner distributions This covers revenue, gross margin, payroll, fixed costs, startup cash, payback, and break-even, not tax advice or a guaranteed salary

Owner income$119k-$1.06MNet margin2.8%-6.2%Revenue for target pay$4.21M-$17.20MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full Asian Restaurant model?

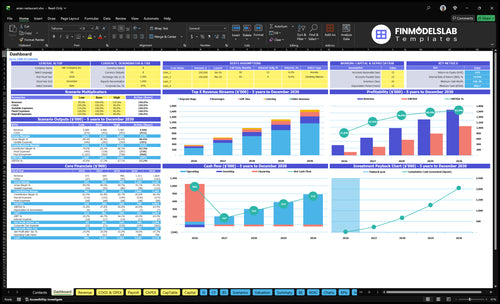

The dashboard shows revenue, margins, EBITDA, cash, break-even, and payback; Asian Restaurant Financial Model Template also opens the assumptions tabs for covers, AOV, sales mix, COGS, variable costs, fixed costs, wages, and capex. It shows $119k Year 1 EBITDA, $308k Year 2 EBITDA, $1064M Year 5 EBITDA, $861k cash need, Month 3 break-even, and 13-month payback. It’s a planning bridge, not a guaranteed income claim.

Model highlights

- Owner income and cash

- Revenue, margins, EBITDA

- Scenarios and assumptions

Can an Asian restaurant owner make good money?

Yes, an Asian Restaurant owner can make good money if traffic and cost control hold; this model shows $4,209k Year 1 revenue and $119k EBITDA before taxes, debt, reserves, and distributions. For context on scaling that profit, see What Is The Primary Goal Of Your Asian Restaurant'S Growth Strategy?.

Profit picture

- Year 1 revenue: $4,209k

- Year 1 EBITDA: $119k

- Year 1 margin: 2.8%

- Year 2 EBITDA: $308k

Owner reality

- Cover $100k Year 1 payroll

- Cover $5,630 monthly fixed costs

- Manage 190% COGS plus variable fees

- Take-home depends on financing and reserves

How sensitive is Asian restaurant profit to food and labor cost?

For an Asian Restaurant, profit is most sensitive to food cost and labor cost. In Year 1, COGS is modeled at 100% of revenue, then falls to 86% by Year 5, so every 1-point move in Year 1 revenue shifts annual gross profit by about $42k; see What Is The Estimated Cost To Open And Launch Your Asian Restaurant Business? for setup context. Payroll rises from $100k in Year 1 to $210k in Year 5 as staffing expands.

Food cost

- Year 1 COGS is 100% of revenue.

- Year 5 COGS drops to 86%.

- Each 1-point shift moves about $42k gross profit.

- Menu mix matters, but no format is assumed.

Labor cost

- Payroll starts at $100k in Year 1.

- Payroll reaches $210k by Year 5.

- Staffing grows with kitchen prep and portion control.

- Wage rates, scheduling, and fees hit take-home profit.

How does the owner’s role change Asian restaurant income?

If the owner works the kitchen or management shifts, Asian Restaurant can protect cash by cutting payroll, but the owner’s labor becomes the hidden cost. In a manager-run setup, the model already carries a $55k annual manager plus staff payroll, so owner draws come only after that layer. Absentee ownership works only if cash earnings can cover management, controls, reserves, and slower issue response.

Owner-operator cash effect

- Owner shifts can replace hired labor.

- Cash stays inside the business.

- Owner time becomes the hidden cost.

- One person can’t cover every gap.

Manager-run tradeoff

- Model already includes $55k manager pay.

- Owner distributions come after payroll.

- Absentee owners need enough cash earnings.

- Slow issue response can hurt margins.

Want the six income drivers?

1

$421K-$1.72MOrder Volume

Weekly covers grow from 710 in Year 1 to 2,500 in Year 5, so this is the biggest lever on owner take-home.

2

$9.5-$14.5Average Check

Midweek and weekend checks rise over time, and even small price gains flow straight into revenue if traffic holds.

3

10.0%-8.6%COGS Control

Food and packaging cost fall from 10.0% of sales to 8.6%, which keeps more gross profit on each order.

4

$100K-$210KLabor Productivity

Payroll climbs from about $100K to $210K a year, so staffing efficiency has a direct hit on margin.

5

$5.63K/moOccupancy Cost

Rent is $4,500 a month and other fixed costs add $1,130, so fixed overhead stays heavy until sales density improves.

6

4.0%Channel Fees

Revenue-share fees hold at 4.0% of sales, and the delivery mix is not provided, so net margin could shift.

Asian Restaurant Core Six Income Drivers

Order Volume

Order Volume

Order volume is the number of covers served each week. In Year 1, the model starts at 710 covers/week, with 180 on Saturday and 150 on Sunday. By Year 5, it reaches 2,500 covers/week, including 580 Saturday and 480 Sunday. More checks spread the $5,630/month fixed cost base over more sales.

Here’s the quick math: using 4.33 weeks/month, fixed costs are about $1,300/week. At Year 1 volume, that is about $1.83 per cover; at Year 5, it drops to about $0.52 per cover. The catch is capacity. If staffing comes too early or the kitchen gets overloaded, stronger volume can still miss EBITDA targets.

Track Covers by Day

Track covers by day and daypart, not just by month. The weekend load matters most here, since Year 5 assumes 580 Saturday covers and 480 Sunday covers. Build the labor plan around peak turns and prep time, then check whether the kitchen can hold service without slowing down.

- Track covers by weekday.

- Match labor to peak hours.

- Watch ticket time and turns.

- Stress-test kitchen throughput first.

Use covers per labor hour and ticket time as the control points. If volume rises but service slips, repeat visits fall and owner pay gets weaker. If volume rises with steady service, the same $5,630 monthly fixed load gets spread wider, and take-home income has room to improve.

1

Average Check And Menu Mix

Average Check and Menu Mix

Average check is revenue per guest, so it moves owner income faster than traffic alone. The model uses $950 midweek and $1,250 on weekends in Year 1, then $1,150 and $1,450 by Year 5. If add-ons, drinks, and higher-priced dishes sell, revenue rises without the same jump in covers.

Menu mix is the share of sales by category. Year 1 model weights are 700%, 150%, 100%, and 50% across four sales categories. That means the check depends on what guests actually buy, not just how many come in. Price moves help only if demand holds; if guests trade down, cash flow and owner pay soften fast.

Track the check, not just the headcount

Watch check size by daypart and item mix. The quick test is simple: if weekends carry the $1,250 to $1,450 range, protect higher-margin drinks and add-ons. Raise prices in small steps and tie each move to guest response so higher menu prices do not slow traffic or hurt repeat visits.

- Track check by weekday and weekend.

- Track add-on and beverage attach.

- Watch mix by sales category.

- Test prices against demand first.

Use the mix to forecast cash flow, since a higher check can lift gross profit even if covers stay flat. If the mix shifts toward lower-priced items, owner draw shrinks before rent and payroll do. Keep the menu board, specials, and server scripts focused on the items that raise the average guest bill.

2

Food Cost And Gross Margin

Food Cost and Gross Margin

This driver is the cost of ingredients, packaging, and beverage supplies. In the model, COGS is 100% of revenue in Year 1, then 97%, 93%, 89%, and 86% by Year 5. That means each $1.00 of sales keeps only $0.03 at 97% COGS and $0.14 at 86% before labor, rent, and owner pay.

Here’s the quick math: better portion control, less prep waste, tighter supplier buys, and a lighter premium-protein mix move cash fast. The model’s gross-margin input shows 900% to 914%, which should be checked, but the real cash driver is the gap between sales and COGS. What this hides: menu mix and waste can swing take-home more than small price cuts.

Control COGS by Recipe

Track recipe yield, portion size, and invoice price for every high-cost item. Build a food-cost sheet that ties covers, average check, and menu mix to target COGS, then compare it with actual spend each week. If a protein item runs hot, cut portions, raise price only where demand holds, or replace it with a lower-cost dish.

Watch packaging and beverage supply use too, because they sit inside COGS and hit cash before reserves. A simple test is to compare theoretical food cost to actual food cost; if the gap widens, waste or theft is creeping in. One clean rule: if COGS slips from 86% to 89%, owner cash falls on every sale, even if traffic stays flat.

3

Labor Productivity

Labor Productivity

Payroll is the largest named cost, so labor productivity drives how much cash the owner can keep. The model lists wages at $100k in Year 1, $1275k in Year 2, $155k in Year 3, $1825k in Year 4, and $210k in Year 5, with one manager, full-time staff, and part-time staff. If labor hours do not match traffic, profit gets squeezed fast.

The key input is covers versus scheduled hours by daypart. Owner-run shifts can cut cash payroll, but if the team is too thin, service gaps, slower turns, and weaker repeat visits can wipe out the savings. This driver matters most when demand swings between weekday meals and weekend peaks, because the wrong schedule lowers the owner’s draw even if payroll looks lean.

Match Hours to Traffic

Track covers per labor hour and labor as a percent of sales by brunch, dinner, and weekend service. Keep the manager, full-time, and part-time mix tight to real demand, not guesswork. If a shift saves payroll but slows tickets or adds mistakes, it is too thin.

Use owner shifts where they protect margin, then step back when fatigue starts to raise errors. The goal is simple: keep labor spend aligned with real traffic so the business preserves cash and the owner can pay themselves from actual profit, not from paper savings that hurt service later.

4

Rent And Occupancy Cost

Rent and Occupancy Cost

$4,500 in rent plus $1,130 for utilities, subscriptions, insurance, permits, cleaning, and accounting puts named fixed occupancy cost at $5,630 per month. That is $67,560 on the monthly math, and it hits profit before owner pay. Every cover has to help carry this load.

This only helps if the site supports demand. A cheap space with weak foot traffic, parking, or visibility can lower covers and push break-even up, even when rent is low. One line says it best: low rent is not low cost if it cuts sales.

Track the lease against covers

Measure the full occupancy bucket, not just base rent. Track rent, utilities, insurance, permits, cleaning, and accounting against covers by daypart and sales per cover. If the site cannot hold traffic at lunch, brunch, dinner, or weekends, the lease is too heavy for the volume plan.

- Track occupancy cost monthly.

- Test foot traffic and parking.

- Watch covers after opening.

- Compare lease cost to sales.

Use the location only if its access lifts revenue enough to offset the fixed bill. If demand slips, occupancy does not flex, so cash flow tightens fast and owner draws get squeezed first. The goal is not the cheapest space; it is the space that protects covers and profit.

5

Takeout And Channel Economics

Channel Cost Mix

This driver can raise sales and still cut owner pay if the blended cost of each order stays high. The model assumes a 40% revenue-share fee every year plus 30% packaging or beverage supplies in Year 1, easing to 26% by Year 5, so the combined burden still sits near 66% to 70% before food labor and overhead.

Use calculator inputs for direct pickup, third-party delivery, and dine-in share. What this estimate hides is channel mix: a $10,000 takeout month with a 40% fee and 30% supplies leaves $3,000 before food labor and overhead, so commissions, discounts, and kitchen capacity matter.

Reduce Fee Drag

Track takeout revenue by channel each week and model commission + packaging + discounts together. If the Year 1 blended burden is near 70% of takeout sales, then the owner’s draw depends on shifting more orders to pickup and cutting low-margin promos, not just pushing more tickets.

- Pickup share vs delivery share

- Commission rate by channel

- Packaging cost per order

- Discounts and refund rate

- Orders per kitchen hour

Watch capacity during rush periods. If delivery spikes while the kitchen is full, extra sales can add fee drag and slow service, which hurts repeat orders and cash flow.

6

Compare low, base, and high Asian restaurant owner income scenarios

Owner income scenarios

Owner income moves with covers, ticket size, and labor. The model ramps from Year 1 to Year 5, so each case shows launch, steady, and capacity-led earnings.

| Scenario | Low CaseRamp | Base CaseStable | High CaseUpside |

|---|---|---|---|

| Launch model | A Year 1 ramp keeps earnings near $119k of EBITDA before owner draw and tax. | Year 2 to Year 3 steadier traffic lifts EBITDA into the $308k-$566k band before owner draw and tax. | Year 5 fuller capacity pushes EBITDA to about $1.064M before owner draw and tax. |

| Typical setup | Traffic starts at 710 weekly covers, with $9.50 midweek tickets and $12.50 weekend tickets, while payroll stays at $100k and fixed overhead runs $5,630 a month. | Weekly covers rise to 1,090 in Year 2 and 1,610 in Year 3, with AOV up to $10.00 midweek and $13.50 on weekends as staffing scales. | Weekly covers reach 2,500 in Year 5, with $11.50 midweek tickets and $14.50 weekend tickets, so the site is running closer to capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $119kLow band | $308k-$566kBase band | $1.064MHigh band |

| Best fit | Use this to stress-test launch risk, slow traffic, and a thin opening cushion. | Use this for the working plan once the store has repeat traffic and a stable labor setup. | Use this to test what happens if the site fills up and keeps strong weekend demand. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Asian Restaurant Porter's Five Forces Analysis

- Asian Restaurant BCG Matrix

- Asian Restaurant Business Model Canvas

- 7 Essential KPIs to Track for Asian Restaurant Profitability

- Asian Restaurant Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Asian Restaurant Profitability and Control Costs

- How To Calculate Monthly Running Costs for an Asian Restaurant

- Asian Restaurant Startup Costs: $715k Opening Outlay Plus Cash Reserve

- Asian Restaurant Financial Model Template in Excel

- How to Open an Asian Restaurant in 4–9 Months With a Launch Plan

- How to Write an Asian Restaurant Business Plan in 7 Steps

- Asian Restaurant Marketing Mix

- Asian Restaurant Marketing Plan

- Asian Restaurant Business Proposal

- Asian Restaurant PESTEL Analysis

- Asian Restaurant Pitch Deck Example Editable PPTX

- Asian Restaurant Business SWOT Analysis

- Asian Restaurant Value Proposition Canvas

Frequently Asked Questions

The researched model shows EBITDA of $119k in Year 1, $308k in Year 2, and $1064M in Year 5 That is business cash flow before taxes, debt payments, reserves, and owner distributions Actual owner take-home depends on financing, reinvestment needs, payroll choices, and how much cash the business keeps