Owner income$160k

Owner income$160kHow Much Can an Astronomical Timer Switch Owner Make? $160k Plan?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$160k  Net margin93%

Net margin93% Revenue for target pay$172k+

Revenue for target pay$172k+ Business difficultyHard

Business difficultyHard

You’re selling automatic sunrise/sunset timer switches, not installing them as an electrical contractor This five-year planning view covers $152k Year 1 revenue, product margin, fixed costs, payroll, inventory cash, and owner take-home before personal taxes, with no guaranteed salary or tax advice

Owner income$160kNet margin93%Revenue for target pay$172k+Business difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and timing.

Want to stress-test the $160k owner income plan?

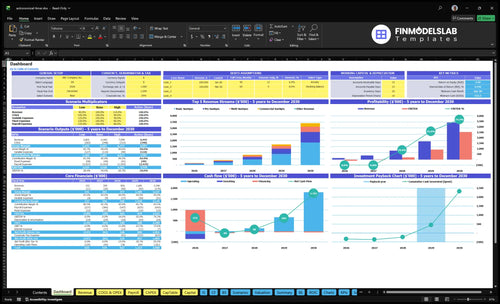

The screenshot ties revenue, margin, costs, reserves, and owner take-home in Astronomical Timer Switch Sales Financial Model Template; open the model for $152k Year 1 revenue, $532k Month 25 cash, 427% IRR, and 35% ROE.

Owner-income model highlights

- Traffic drives owner pay

- Revenue and margin charts

- Scenario testing on costs

What is the profit margin on astronomical timer switches?

Astronomical Timer Switch Sales does not have one fixed profit margin. In Year 1, product cost is 7% and gross margin after product cost is 93%; by Year 5, product cost falls to 5% and gross margin rises to 95%. Shipping, fulfillment, and payment fees also improve from 25% to 15%, but actual owner take-home still depends on freight, returns, warranties, marketplace fees, discounting, and slow-moving inventory; see What Are Operating Costs For Astronomical Timer Switch Sales?

Margin moves

- 7% product cost in Year 1

- 5% product cost in Year 5

- Gross margin lifts from 93% to 95%

- Lower cost raises room for profit

Cost risks

- Fees fall from 25% to 15%

- Freight can still squeeze take-home

- Returns and warranties cut margin fast

- Discounting and dead stock hurt cash

Is selling timer switches online or to contractors better?

Astronomical Timer Switch Sales will usually keep more control over margin with direct online sales, but contractor accounts can give you better repeat orders and cleaner forecasting. The best channel is the one with the stronger contribution per order after support, returns, and cash timing. Commercial maintenance buyers can also lift average order value by buying premium models and multi-unit baskets.

Direct online

- Protects price and margin

- Needs more content and ads

- Raises support and return work

- Fits first-time buyers well

Contractors

- Can drive repeat orders

- Improves forecasting quality

- Lifts multi-unit baskets

- May delay cash collection

How much can I make selling astronomical timer switches?

You can plan for $160,000 in owner pay from Astronomical Timer Switch Sales, but Year 1 does not fully fund it: projected revenue is $152,000 and the operating result after wages is about negative $77,000 before launch capex. For setup detail, see How Do I Write An Astronomical Timer Switch Sales Business Plan?; the short answer is that income depends on unit volume, customer mix, markup, overhead, and how soon you hire.

Year 1 math

- Revenue: $152,000

- Product cost: 7%

- Variable fees: 25%

- Fixed overhead: $9,720

Pay drivers

- Owner role included in $205,000 wages

- Hiring early pressures cash flow

- Higher markup improves owner pay

- More units reduce overhead strain

Want to see what moves owner income most?

1

$152K-$3.4MUnit volume

Visitor growth plus a 1.5% to 2.9% buy rate drives most of the revenue swing, so traffic comes first.

2

$39.99-$154.52Selling price

The price ladder runs wide, so a better product mix lifts income without needing more orders.

3

93%-95%Product cost

Product cost stays at 7.0% to 5.0% of sales, which keeps gross margin very high on each unit sold.

4

70/20/7/3Mix shift

Shifting away from the entry unit toward higher-tier units raises order value, even if traffic stays flat.

5

$9.7K/yrOverhead

Fixed overhead is light, so added gross profit drops faster to owner income as volume scales.

6

$532KCash turns

The $150K inventory build and the Month 25 cash low to $532K show why slow turns can trap owner capital.

Astronomical Timer Switch Sales Core Six Income Drivers

Monthly Unit Sales Volume

Monthly Unit Sales Volume

Monthly unit sales volume is the count of timer units sold each month. In the Year 1 model, that is about 204 orders per month at a $6,221 AOV, or about 244 units per month using 12 units per order. More units lift gross profit only if pricing holds and fulfillment does not force extra payroll.

Here’s the quick math: unit sales = orders × units per order. Demand can come from replacement timers, outdoor lighting projects, contractor repeat orders, and ecommerce traffic. The owner’s take-home pay rises only when unit growth outpaces shipping, support, and labor costs; strong traffic alone does not pay the bills if conversion or stockouts block sales.

Track Units, Not Just Traffic

Measure monthly orders, units per order, conversion rate, stockout days, and fulfillment labor. A traffic spike without orders is just more visits. If unit volume rises, keep payroll flat by batching picks, protecting fast-moving SKUs, and checking whether order density is high enough before hiring.

204 orders at 12 units each is the base case, so even small conversion changes move profit fast. If a channel brings more clicks but fewer purchases, or inventory runs short, owner income can fall even when demand looks strong on paper. Watch the gap between traffic and shipped units each week.

- 204 monthly orders model

- 244 units at base case

- 12 units per order

- Track stockouts by SKU

- Delay hiring until density holds

1

Average Selling Price And Order Value

Average Selling Price and Order Value

When each order carries more value, the owner can spread fixed costs and marketing spend over more dollars. In Year 1, the model uses a $5,184 weighted unit price and a $6,221 average order value at 12 units per order, so basket size is a real income driver, not just unit count.

The price ladder at $3,999, $6,499, $9,499, and $13,999 can lift revenue if buyers accept the upgrade. But higher price does not equal higher profit if buyers compare specs, shipping, warranty terms, and delivery speed, because that can hit conversion and delay cash coming back.

Track basket mix and price resistance

Measure tier mix, units per order, conversion rate, and gross margin after freight and payment fees. A higher AOV only helps owner pay if the extra revenue beats the added service and delivery cost. Here’s the quick math: if higher tiers sell slower, revenue can rise while cash draw falls.

- Track orders by price tier.

- Watch units per order monthly.

- Test bundles and commercial baskets.

- Log warranty and shipping complaints.

Use premium controls and multi-unit pricing first, since they can raise order value without needing more traffic. If delivery speed or warranty terms slip, buyers may switch to cheaper options fast, so protect the offer before pushing price higher.

2

Landed Product Cost And Gross Margin

Landed Cost Drives Gross Margin

Use landed cost, not purchase price alone. Here, product manufacturing cost is 7% of revenue in Year 1, so gross margin, the sales left after product cost, is 93%; by Year 5, cost falls to 5% and gross margin rises to 95%. That helps owner pay only if freight, packaging, payment fees, returns, and warranty replacements stay controlled.

A low product cost ratio can still hide cash strain. If bulk buys and replacement units sit in inventory, cash leaves before revenue comes back, so take-home pay can lag even when the margin looks strong.

Measure Full Landed Cost

Track landed cost per unit and per order: manufacturing, freight, packaging, payment fees, returns, and warranty replacements. Tie it to gross margin and cash on hand, not just revenue. The simple check is this: if product cost is 7% of sales, ask what the full all-in cost is before setting owner draw.

- Check cost per unit monthly

- Separate returns and warranty costs

- Watch inventory tied in bulk buys

- Compare gross margin by channel

If landed cost creeps up, cut discounts or reorder size before it eats the cash needed for salary or profit draw.

3

Sales Channel Mix

Sales Channel Mix and Take-Home Pay

Channel mix changes how much cash reaches the owner. Direct online sales can protect price, but they add support, content, ads, and returns. Contractor repeat accounts may accept lower markup for bigger, steadier reorders. The best channel is the one with the highest reliable contribution after service cost, not just the highest top-line sales.

For this model, the owner should compare revenue by channel against workload and cash strain. With 93% gross margin in Year 1 before channel overhead, even small support or freight costs can change draw capacity. If distributor-style deals raise volume but push payment terms out, profit can look fine while cash for inventory and owner pay gets tight.

Track Contribution by Channel

Measure each channel with the same inputs: orders, average order value, repeat rate, return rate, support time, ad spend, and payment terms. That tells you which channel leaves the most cash after selling costs. One line to remember: revenue is not income.

- Track gross margin by channel.

- Load support hours per order.

- Watch payment terms and aging.

- Compare repeat baskets and reorders.

- Cut channels with weak cash conversion.

If a channel lifts volume but needs heavy ad spend or slow pay, it can reduce owner income even when sales rise. Keep a simple monthly view of revenue, service cost, and cash collected by channel, then push the mix toward the channel with the best net margin and fastest cash turn.

4

Operating Cost Control

Operating Cost Control

Operating cost control is mostly about keeping the cost base from outrunning sales. Here, fixed overhead is only $810 per month, or $9,720 per year, but variable shipping, fulfillment, and payment fees take 25% of revenue in Year 1. That means every $10,000 sold leaves about $7,500 before payroll and overhead.

The real pressure point is wages: $205k in Year 1, including $160k CEO pay and $45k marketing payroll. If sales density is still thin, payroll can turn gross margin into cash burn fast, even when product margin looks strong.

Track payroll before you hire

Model owner income as revenue minus 25% variable fees, $810 monthly overhead, and wages. Track monthly orders, revenue per order, fee rate, and payroll as a percent of revenue. One clean test: if added headcount does not raise conversion or repeat orders enough to cover its full cost, delay the hire.

- Watch payroll against monthly sales.

- Hold fixed overhead near $810.

- Test hires after sales density rises.

- Keep fee rates and returns v isible.

5

Inventory Cash Reserve

Inventory Cash Reserve

Owner take-home depends on cash left after stocking inventory. In this model, $150k goes into initial inventory over the first 6 months, and total launch setup reaches $236k. That means profit on paper does not equal cash in hand, because stock ties up money before it can be sold and paid out.

The key inputs are order volume, reorder timing, slow-moving SKUs, and warranty replacements. The model’s $532k minimum cash figure in Month 25 is the guardrail. If cash drops under that floor, owner draws should wait, even when gross margin looks strong.

Protect the Cash Floor

Track inventory by SKU, weeks of cover, and sell-through before paying yourself. Use a reserve that covers seasonal demand, bulk buys, and replacement stock. One clean rule: do not take distributions unless cash stays above the Month 25 floor.

Watch these inputs each month:

- Units on hand by SKU

- Open purchase orders

- Warranty replacement count

- Slow-moving inventory age

- Cash after the next reorder

If a bulk buy or weak SKU pushes cash down, cut the owner draw first. That keeps stock available, protects future sales, and avoids a cash squeeze that can block income even with high gross margin.

6

Compare lean, base, and high owner-income cases

Owner income scenarios

Owner income shifts fast here because Year 1 EBITDA is negative, then the model turns cash positive after Month 23 as conversion, repeats, and mix improve.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | The downside case keeps owner take-home before taxes near zero because traffic and conversion stay below plan. | The base case follows the model, with $152k of Year 1 revenue, -$109k of EBITDA, and breakeven in Month 23. | The upside case tests stronger conversion, more repeat buyers, and a better mix, so owner take-home before taxes can rise faster after breakeven. |

| Typical setup | Year 1 revenue trails the model, so payroll is trimmed and owner draw waits until contribution can cover core costs. | The plan carries 93% gross margin after product cost, 90.5% contribution after fees, $9,720 of fixed overhead, about $205k of wages, and $236k of launch setup plus $150k of inventory. | Traffic quality improves to 2.9% conversion, repeat customers rise to 24%, units per order reach 1.6, and more orders move into higher-priced tiers. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Near-zero owner drawCash tight | Up to $160k payMain case | Above $160k payUpside test |

| Best fit | Use this to stress-test cash if traffic or conversion miss the model. | Use this as the main planning case for budget, cash, and staffing. | Use this to test upside if traffic quality, repeat buying, and mix all beat plan. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Astronomical Timer Switch Sales Porter's Five Forces Analysis

- Astronomical Timer Switch Sales BCG Matrix

- Astronomical Timer Switch Sales Business Model Canvas

- What Are The 5 KPIs For Astronomical Timer Switch Sales Business?

- Astronomical Timer Switch Business Plan Template in Pre-Written Word

- How Increase Astronomical Timer Switch Sales Profitability?

- What Are Operating Costs For Astronomical Timer Switch Sales?

- Astronomical Timer Switch Startup Costs: $532K Funding Plan

- Astronomical Timer Switch Sales Financial Model Template in Excel

- Start an Astronomical Timer Switch Supplier in 8–14 Weeks

- How Do I Write An Astronomical Timer Switch Sales Business Plan?

- Astronomical Timer Switch Sales Marketing Mix

- Astronomical Timer Switch Sales Marketing Plan

- Astronomical Timer Switch Sales Business Proposal

- Astronomical Timer Switch Sales PESTEL Analysis

- Astronomical Timer Switch Sales Pitch Deck Example Editable PPTX

- Astronomical Timer Switch Sales Business SWOT Analysis

- Astronomical Timer Switch Sales Value Proposition Canvas

Frequently Asked Questions

The researched plan includes $160k in owner pay, but it is not funded by Year 1 operating profit Revenue is $152k, product cost is 7%, and total wages are $205k So the owner can take that pay only if startup cash or outside funding covers the early gap