Owner income$1.1M–$4.4M

Owner income$1.1M–$4.4MHow Much Attic Conversion Owners Make At 51 To 147 Jobs

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.1M–$4.4M  Net margin44%–53%

Net margin44%–53% Revenue for target pay$8.2M

Revenue for target pay$8.2M Business difficultyMedium

Business difficultyMedium

You’re pricing big home projects, so revenue is not owner income Using the researched model, Year 1 revenue is $245M from 51 completed projects, with potential pre-tax owner take-home of $147M before debt service, reserves, reinvestment, and personal taxes Results vary by market, scope mix, crew model, permit timing, and completed project volume

Owner income$1.1M–$4.4MNet margin44%–53%Revenue for target pay$8.2MBusiness difficultyMediumWant to test your own attic conversion owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner pay depends on revenue, margin, labor, overhead, debt, reserves, and taxes.

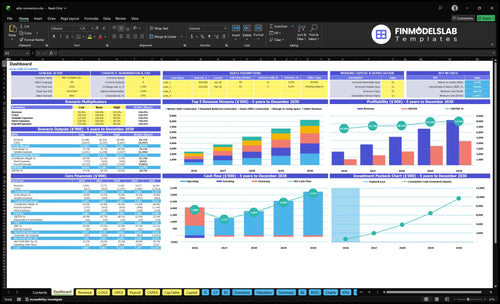

How do owner-income scenarios look in the Attic Conversion Service model?

This dashboard in the Attic Conversion Service Financial Model Template shows revenue, gross profit, operating profit, and owner-income scenarios—open the model.

Owner-income model highlights

- Assumptions, pricing, direct costs

- Marketing, overhead, hiring, reserves

- Owner pay by scenario

- 51, 99, 147 projects

- $245M, $518M, $824M cases

- Scenario testing, not a promise

How much does an attic conversion business owner make per year?

An Attic Conversion Service owner does not make one flat salary; income depends on the owner’s role and completed project volume. In the provided model, potential pre-tax owner take-home runs from $147M in Year 1 to $556M in Year 5 before debt, reserves, reinvestment, and personal taxes; use How To Write An Attic Conversion Service Business Plan? to map that forecast into a working plan.

Owner earnings by stage

- Year 1: 51 completed projects

- Year 1 revenue: $245M

- Year 1 take-home: $147M

- Owner role: operator-led

Growth case math

- Year 3: 99 projects

- Year 3 revenue: $518M

- Year 3 take-home: $335M

- Year 5: 147 projects, $824M revenue, $556M take-home

Can an attic conversion owner make more by hiring crews?

Yes — the Attic Conversion Service can make more by hiring crews if it keeps quality and cash flow tight. The model grows from 51 completed projects in Year 1 to 147 in Year 5, so income can scale when the owner is not the bottleneck. But the upside can get eaten by warranty exposure, inspection delays, schedule gaps, and subcontractor pricing.

Why crews can raise income

- 51 projects in Year 1

- 147 projects in Year 5

- $797k direct carpentry labor

- Crews free the owner from field work

Where margin gets hit

- $1,002k electrical and plumbing subs

- Warranty calls can drain profit

- Inspection delays slow cash collection

- Schedule gaps raise overhead per job

What profit margin should an attic conversion business have?

For Attic Conversion Service, the real question is not just gross margin; it’s what’s left after overhead and owner pay. Based on listed direct costs only, researched gross margin is 748% in Year 1, 758% in Year 3, and 768% in Year 5, but that is not the same as net profit. Per-project direct costs run from $65k for storage-to-living-space work to $170k for master suite conversions, plus 65% revenue-based direct costs; How To Write An Attic Conversion Service Business Plan? should model each scope separately.

Margin drivers

- $65k direct cost floor

- $170k master suite direct cost

- 65% revenue-based direct costs

- Price by project scope

What to watch

- Gross margin is not net profit

- Owner income sits below margin

- Track framing and insulation costs

- Watch permits and rework

Want the six attic conversion income drivers?

1

51-147/yrProject Count

More finished attic jobs lifts revenue straight away, and the model scales from 51 to 147 annual projects.

2

$35K-$96KDeal Size

Higher-priced suite and office builds push annual revenue up without adding the same fixed cost each time.

3

44%-53%Margin

Stronger margin keeps more of each job after labor, materials, permits, and site waste.

4

1-4 PMsCrew Capacity

More project management coverage keeps more jobs moving at once, so backlog turns into cash faster.

5

8%-10%Lead Quality

Better leads cut the sales and marketing drag, which protects cash before a job even starts.

6

$37K/moOverhead Control

Keeping salary and fixed cost growth in check helps the business hold take-home as volume builds.

Attic Conversion Service Core Six Income Drivers

Average Contract Value

Average Contract Value

Average contract value is the mix of attic jobs you sell, from $35k storage-to-living-space work up to $85k master suite conversions. Revenue rises when the mix shifts to bigger scopes, and the model shows weighted average project revenue of $479k in Year 1 and $561k in Year 5. Bigger jobs can lift owner pay, but only if margin holds.

- Job mix by scope

- Base price per scope

- Change orders

- Permit and trade add-ons

Here’s the quick math: completed projects × average contract value. What this estimate hides is risk; larger scopes often add bathrooms, dormers, structural work, HVAC changes, and higher-end finishes, which can push permits, trades, schedules, and rework costs higher. If scope creep is not priced, cash flow gets tight even when sales look strong.

Price the Scope Mix

Track contract value by job type, then compare quote price to final billed amount. Break out storage-to-living-space, office, bedroom, and master suite work so you can see which scopes carry the best gross margin, not just the highest revenue. A $85k suite can be a better job than a $35k conversion only if extra trade and permit costs stay controlled.

Build a change-order rule for every added bathroom, dormer, or HVAC shift. Tie approvals to updated labor, material, and schedule costs before work starts. That protects take-home income by stopping high-revenue jobs from turning into low-cash jobs.

1

Gross Margin And Job Costing

Gross Margin and Job Costing

If estimates miss field reality, owner pay shrinks fast. This model assumes direct costs of $65k to $170k per project plus 65% revenue-based costs for permits, drafting, structural review, software allocation, and disposal. The disclosed gross margin is 748% in Year 1 and 768% in Year 5, but that spread still has to absorb rework and change orders before the owner draws cash.

Gross margin is not final owner pay. The real pressure points are change orders, framing surprises, insulation, drywall, electrical, plumbing, and HVAC adjustments, because each one can push the job past the bid and delay collection. If estimates are tight but field costs drift, the business can look busy and still leave less cash for the owner.

Measure Job Cost Drift

Build each bid from the same cost buckets and compare estimate to actual on every closeout. Track permit, drafting, structural review, software allocation, and disposal separately from trade labor so you can see where margin slips. One clean rule: if the same surprise shows up twice, it belongs in the estimate, not in profit.

Use a job-cost sheet on every project and flag overruns early. Watch change orders, rework hours, and trade adjustments by job, then reset pricing when the pattern repeats. The owner’s take-home improves only when the bid covers real field costs and the gross margin stays intact after cleanup, punch list work, and final billing.

- Track estimate versus actual by cost code.

- Price framing surprises before the job starts.

- Separate rework from planned labor.

- Log every change order the same day.

- Review margin after each closeout.

2

Completed Project Volume

Completed Project Volume

Leads do not pay the owner; completed and collected projects do. In this model, volume moves from 51 completed projects in Year 1 to 99 in Year 3 and 147 in Year 5, while revenue rises from $245M to $824M. Faster closeout beats a bigger backlog that stalls cash.

Volume only helps if scheduling, inspections, crew availability, materials, and quality control all hold. If any one of those breaks, jobs sit open, invoices lag, and owner draw gets pushed back. The key metric is completed jobs per year, not leads or signed estimates.

How to Raise Finished Job Count

Track the handoff from sold job to finished job: permit timing, start date, labor crew assigned, inspection date, punch list close, and invoice collection. That tells you where jobs slow down and where cash gets stuck.

- Measure completed jobs monthly.

- Track days from start to closeout.

- Watch inspection and rework delays.

- Limit jobs that start without crews.

If closeout slips, revenue may look booked but cash still trails. Keep the schedule tight, line up materials early, and clear punch items fast so completed volume turns into usable profit and owner pay.

3

Lead Quality And Quote Close Rate

Lead Quality And Quote Close Rate

Quote close rate means signed jobs divided by quotes sent. It drives owner income because poor-fit leads burn estimating time and lower the share of quotes that turn into revenue. Focus on homeowners with code-compliant attic space, realistic budgets, and urgent space needs, so the sales team spends time on jobs that can actually close and collect.

Here’s the quick math: sales commissions are 40% of revenue each year, and local digital marketing falls from 60% in Year 1 to 40% in Year 5, so total sales and marketing burden moves from 100% to 80%. Better leads protect margin because more booked gross profit survives to cover overhead and owner pay.

Track Booked Gross Profit, Not Lead Count

Measure each lead source by closed jobs, booked gross profit, and estimate hours per win. A source that sends lots of quotes but few signed projects raises selling cost per job and drags cash flow, even if the top of the funnel looks busy. That’s the wrong kind of growth for the owner’s take-home income.

- Score attic fit before quoting.

- Reject weak budgets fast.

- Track quote-to-close by source.

- Review booked gross profit monthly.

- Cut high-hour, low-close leads.

4

Labor And Subcontractor Capacity

Crew Capacity and Subcontractor Control

When crews stay reliable, more attic jobs finish on time and cash comes in faster. Year 1 direct onsite carpentry labor is $797k, and electrical and plumbing subcontractors total $1,002k. Per project, carpentry labor runs $11k to $30k and electrical/plumbing runs $14k to $38k, so labor mix can swing margin hard.

Missed handoffs create rework, warranty calls, and slower collections. That means the owner’s take-home drops twice: first from higher job cost, then from delayed billing. One late trade can turn a clean conversion into a cash drag.

Track Crew Handoff Losses

Measure labor by job, not just by month. Track planned hours versus actual hours, change orders, punch-list time, and how many days each trade waits on the next one. If electrical or plumbing slips, framing, drywall, and inspection timing all move, so capacity falls even when sales stay strong.

- Track job labor variance weekly

- Log handoff del ays by trade

- Price rework into estimates

- Schedule subs before start dates

Set a field foreman to own handoffs and closeout. If crews can’t protect the schedule, the business can’t scale without margin leaks. Faster closeout means faster invoicing, and that directly supports owner pay.

5

Overhead And Owner Pay Discipline

Owner Pay After Cash Needs

Owner pay comes last. In this attic conversion model, fixed overhead is $92k per month or $1,104k per year, and that covers rent, insurance, vehicle, utilities, internet, and software. Sales and marketing add $2,445k in Year 1 and $6,595k in Year 5, so the owner’s draw only works after those costs are funded.

The model also needs a separate reserve input. If you skip reserves, the business can look profitable on paper while cash gets trapped in warranty work or slow payments. One rule: don’t pay the owner from money you still need for the job.

Set The Draw Rule Before You Pay Yourself

Track overhead, sales and marketing, and reserves as separate lines. Use the $92k monthly overhead run rate as the floor, then add a reserve for warranty risk and receivable timing. If cash collected is behind work done, hold the draw until that gap closes.

Build the owner payout rule into the forecast: overhead first, reserves second, owner pay last. Here’s the quick test: if a month ends with open warranty items or unpaid invoices, the cash is not free yet. That discipline protects take-home income later.

6

Compare lean, base, and high attic conversion owner-income scenarios

Owner income scenarios

Owner income moves with project count, mix, and margin. Year 1, Year 3, and Year 5 show how more volume spreads fixed costs and lifts take-home.

| Scenario | Low CaseLean case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | The lean case follows the Year 1 run rate, so income starts with 51 projects and the smallest cost base. | The base case uses the Year 3 modeled run rate after staffing and sales start to settle. | The high case assumes the Year 5 run rate, where the strongest project flow and higher-value jobs lift income. |

| Typical setup | Year 1 reaches 51 projects, $2.445M revenue, and about $1.086M EBITDA, with a 44.4% EBITDA margin before taxes and owner draws. | Year 3 reaches 99 projects, $5.183M revenue, and about $2.494M EBITDA, with a 48.1% EBITDA margin as fixed costs spread. | Year 5 reaches 147 projects, $8.244M revenue, and about $4.400M EBITDA, with a 53.4% EBITDA margin at scale. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.1MLean take-home | $2.5MBase take-home | $4.4MUpside take-home |

| Best fit | Fits founders stress-testing opening month cash draws and a slower ramp. | Fits the main operating plan for staffing, owner draws, and lender talks. | Fits an upside plan if project flow stays strong and the team scales well. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Attic Conversion Service Porter's Five Forces Analysis

- Attic Conversion Service BCG Matrix

- Attic Conversion Service Business Model Canvas

- What Are The 5 KPIs For Attic Conversion Service?

- Attic Conversion Business Plan Template in Pre-Written Word

- How Increase Profits For Attic Conversion Service?

- What Are Operating Costs For Attic Conversion Service?

- Attic Conversion Service Startup Costs for a 51-Job Year 1 Plan

- Attic Conversion Service Financial Model Template in Excel

- How to Start an Attic Conversion Business in 8–16 Weeks

- How To Write An Attic Conversion Service Business Plan?

- Attic Conversion Service Marketing Mix

- Attic Conversion Service Marketing Plan

- Attic Conversion Service Business Proposal

- Attic Conversion Service PESTEL Analysis

- Attic Conversion Service Pitch Deck Example Editable PPTX

- Attic Conversion Service Business SWOT Analysis

- Attic Conversion Service Value Proposition Canvas

Frequently Asked Questions

Using the researched assumptions, potential pre-tax owner take-home is $147M in Year 1 on 51 completed projects and $245M of revenue By Year 3, it reaches $335M on 99 projects and $518M of revenue This is business cash flow before debt, reserves, reinvestment, and personal taxes