Owner income$0-$85K

Owner income$0-$85KHow Much AV Wiring Business Owners Make: $0 To $274K By Year 2

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0-$85K  Net margin-16% to 45%

Net margin-16% to 45% Revenue for target payAbout $1.1M

Revenue for target payAbout $1.1M Business difficultyHard

Business difficultyHard

An audio visual wiring installation owner can plan around low or no true owner distributions in Year 1 if the company follows this staffed model The researched assumptions show $661K in Year 1 revenue, $380K in payroll, $1248K in fixed overhead, and -$103K EBITDA, so cash is tight even if the owner fills the operations role By Year 2, revenue rises to $1475M and EBITDA reaches $274K before taxes, reserves, and debt service Treat that $274K as the available profit pool, not guaranteed take-home

Owner income$0-$85KNet margin-16% to 45%Revenue for target payAbout $1.1MBusiness difficultyHardWant to test your AV wiring owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Taxes, personal benefits, loan terms, and guaranteed distributions are excluded.

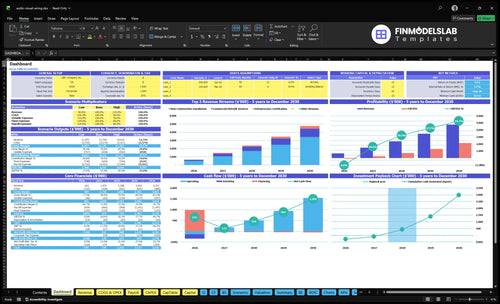

How do you check owner income in the Audio Visual Wiring Installation model?

The dashboard in the Audio Visual Wiring Installation Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions—open it.

Owner-income model highlights

- Owner take-home assumptions

- Revenue and margin view

- Scenario testing by month

What profit margin does an audio visual wiring business need?

If your Audio Visual Wiring Installation business is priced well, Year 1 gross margin can land near 44%, and it can reach about 63% by Year 5 as crew output improves and material and subcontractor shares fall. For the cost mix, What Are Operating Costs For Audio Visual Wiring Installation? points to 18% materials, 5% subcontracted labor, 4% fuel, and 1% disposal after field technician wages. Cable waste, connectors, wall plates, racks, rework, and missed change orders are the margin leaks to watch.

Year 1 margin

- 44% gross margin target

- 18% materials cost

- 5% subcontracted labor

- 4% fuel and 1% disposal

Year 5 margin

- 63% gross margin potential

- Lower material share helps

- Higher crew output lifts margin

- Rework cuts profit fast

How much revenue does an audio visual wiring business need to pay the owner?

Audio Visual Wiring Installation can’t pay the owner from revenue alone. With $104K in fixed overhead each month before payroll, Year 1 at $661K revenue still lands at -$103K EBITDA, so there isn’t enough cushion for steady owner pay. By Year 2, $1.475M revenue and $274K EBITDA before taxes and reserves can support pay, but only if gross margin, backlog, crew use, and cash reserves all hold up.

Year 1 pressure

- $661K revenue

- -$103K EBITDA

- $104K monthly overhead

- No safe owner draw

Pay depends on more

- $1.475M revenue in Year 2

- $274K EBITDA before taxes

- Gross margin sets pay room

- Reserves protect owner salary

How much can a solo audio visual wiring installer make?

With the provided Year 1 model, a solo Audio Visual Wiring Installation owner should separate paycheck from profit: replacing the $85K operations manager role can be owner compensation, but the business still shows -$103K EBITDA after staffing and overhead; for the operating drivers, see What Are The 5 KPIs For Audio Visual Wiring Installation Business?.

Paycheck vs profit

- $85K can be owner labor pay

- -$103K EBITDA means no distributable profit

- Solo work may reduce payroll

- Capacity drops when selling time disappears

Real take-home math

- Start with billable hours

- Multiply by hourly rate

- Subtract materials, fuel, insurance

- Subtract tools and overhead

Want the six AV wiring income drivers?

1

$661K-$4.77MCrew Capacity

Billable hours per active customer rise from 45 to 60, and revenue scales from $661K in Year 1 to $4.77M in Year 5.

2

$95-$175/hrProject Mix

A better mix of new construction, retrofit, and certification work pushes the hourly rate from $95 to $175 and lifts take-home.

3

77%-81%Margin Control

Materials fall from 18% to 16% and subcontracted labor from 5% to 3%, so gross margin widens from about 77% to 81%.

4

HighChange Orders

Tighter scopes and paid change orders stop free work and protect margin when jobs expand after the bid.

5

$10.4K/moOverhead Control

Fixed overhead runs about $10.4K a month, so rent, insurance, vehicles, software, and admin can still erode EBITDA if volume slips.

6

6.5-20 FTEOwner Leverage

Take-home improves when the owner sells and coordinates instead of doing field work, because staffing grows from 6.5 FTE to 20 FTE.

Audio Visual Wiring Installation Core Six Income Drivers

Billable Crew Capacity

Billable Crew Capacity

Income here comes from scheduled billable hours, not headcount alone. In this model, new construction brings 120 to 150 hours, retrofit 40 to 50, and certification 16 to 24; average active-customer hours rise from 45 to 60 per month. More hours only help if they are actually billable and not lost to travel, blocked ceilings, missing materials, or callbacks.

Here’s the quick math: a crew can look busy and still lose income if nonbillable time rises. Higher utilization, the share of crew time that is billable, lifts revenue and gross profit after wages, subcontractors, fuel, and overhead. One clean rule: every unscheduled hour is a margin leak.

Track Scheduled Hours, Not Headcount

Track booked hours by service line each week: new construction, retrofit, and certification. Compare scheduled hours to billed hours, then log lost time from travel, access delays, or rework. If active-customer hours stay near 45 instead of 60 per month, the crew is underused before cash flow tightens.

- Measure billable hours by crew.

- Separate travel from onsite work.

- Flag callback causes fast.

- Plan materials before dispatch.

- Review blocked-access jobs weekly.

Use the gap between scheduled and billed hours to set staffing, price jobs, and forecast owner draw. If the crew is busy but revenue stalls, the issue is usually utilization, not demand.

1

Project Mix And Average Ticket

Project Mix and Average Ticket

This driver is the split of jobs by type and the revenue per mobilization. When the mix shifts toward larger new construction and multi-room cabling jobs, revenue per trip rises because setup time gets spread over more billable hours. Year 1 rates are $95 for new construction, $110 for retrofit, and $150 for certification, so mix changes can move owner pay fast.

Certification pays the highest rate but usually uses fewer hours, so it lifts revenue density more than total volume. Small service jobs can fill schedule gaps, but they often cap ticket size. The owner should watch billable hours per mobilization, service mix, and rework, because weak mix can raise travel and labor cost without lifting gross profit.

Track Mix by Job Type and Ticket

Measure the share of new construction, retrofit, and certification work each month, plus average hours and revenue per job. The stated mix target moves from 40% to 60% for new construction, 30% to 45% for retrofit, and 15% to 35% for certification. If the mix shifts toward higher-rate work, owner draw can rise without adding crews.

- Track revenue per mobilization.

- Track hours by service line.

- Price small jobs to cover setup.

- Push larger prewire jobs first.

Use this rule: if a job adds travel, ceiling access, or rack setup, it needs enough billable hours to protect margin. Commercial prewire and multi-room cabling usually support crews better than short service calls, while certification can lift rate to $150/hr but still leave idle time if demand is thin.

2

Gross Margin On Labor And Materials

Gross Margin on Labor and Materials

Gross margin is what’s left after direct job costs, before overhead, reserves, taxes, and owner distributions. In Year 1, the stated direct cost lines total 28% of revenue: 18% materials, 5% subcontracted labor, 4% fuel, and 1% disposal. Field technician payroll is the largest direct labor load, so labor control is the main swing factor in owner pay.

Here’s the quick math: tighter cable pull planning, correct counts for connectors and plates, and low rework protect margin on every invoice. If subcontractors are used only when pricing supports them, more of the job stays available for overhead and profit. Miss one material item or spend extra time on callbacks, and the same revenue produces less cash for the owner.

Measure Margin Leakages

Track each job against the 28% direct-cost baseline, then add field technician payroll by hour. Estimate using revenue, labor hours, material counts, fuel miles, disposal charges, and subcontract rates. If actual cost drifts above plan, fix the estimate, the crew plan, or the scope before the next job starts.

- Count connectors and plates up front.

- Log rework and callback hours.

- Use subs only with margin left.

3

Estimating Accuracy And Change Orders

Estimating Accuracy And Change Orders

Bad estimates cut owner income before the first invoice goes out. For AV wiring, the bid has to lock down drawings, cable counts, pathways, ceiling access, rack locations, after-hours rules, disposal, and testing scope; if any of those shift, the crew burns paid hours that were never priced.

Protect Margin With Written Scope

Use a bid checklist and compare estimate vs. actual hours by job type. Track every scope change tied to client changes, hidden access issues, added drops, or schedule compression; that tells you when to add contingency or issue a change order before labor turns into lost gross margin. This is income protection, not a sales trick.

4

Overhead Control

Recurring Overhead Load

If the shop runs profitable jobs but carries $104K a month in fixed overhead, owner take-home still gets squeezed. That is $1.248M a year before taxes, reserves, and draws. In this model, overhead includes $45K rent, $12K insurance, $28K auto leases, plus software, utilities, and professional fees.

The key inputs are fixed overhead, marketing, and what stays outside job cost. Marketing starts at $15K in Year 1 and rises to $40K by Year 5, so the owner needs enough gross profit each month to cover that burn before paying themselves. If overhead rises faster than billable hours, cash tightens fast.

Control Monthly Burn

Track each overhead bucket monthly: rent, insurance, vehicles, software, utilities, fees, and marketing. One clean rule: direct labor and materials belong in job cost; overhead belongs below gross profit. That keeps bids honest and shows the real cash needed to fund owner pay.

- Monthly fixed burn by bucket

- Marketing by year

- Reserve target kept separate

- Gross profit coverage for draws

If a project looks profitable on paper but does not lift gross profit above $104K monthly, the draw comes out of cash, not profit. That is why overhead control should sit in the forecast, not in the estimator's head.

5

Owner Role And Crew Leverage

Owner Role and Crew Leverage

If the owner sells, estimates, manages, installs, and checks quality, income stays tied to one person’s time. An owner-operator model saves cash, but it caps capacity; a managed crew model can scale revenue, but only when backlog keeps labor busy and field quality stays tight.

Here’s the quick math: Year 1 payroll is $380K, so idle labor, travel time, blocked ceilings, and callbacks can cut owner pay fast. The owner earns more when pricing covers rework risk and scheduled hours turn into accepted work.

Track Role Time and Crew Utilization

Track who is doing what: selling, estimating, managing, installing, and quality checks. If the owner is still on the tools, watch utilization and rework rate together; one weak job can erase margin from several good ones. The key inputs are backlog, billable hours, labor cost, and callback rate.

Only add crew when work is booked, scoped, and priced for rework risk. If backlog drops, cut labor before cash flow turns negative; if quality slips, revenue can rise while take-home income falls.

6

Compare lean, base, and managed AV wiring owner-income scenarios

Owner income scenarios

Owner pay swings with utilization, staffing, and project mix. Early months are cash tight, then income improves as the crew fills capacity and cash pressure eases.

| Scenario | Low CaseCash tight | Base CaseModeled cash flow | High CaseScale upside |

|---|---|---|---|

| Launch model | This is the lean ramp case, where Year 1 is still loss-making and owner pay stays tight. | This is the modeled base case, where the business turns positive but owner pay still depends on taxes and reserves. | This is the stronger earnings case, where the shop runs at scale and owner pay can rise after cash reserves are funded. |

| Typical setup | Year 1 revenue is $661K, gross margin is about 44%, EBITDA is -$103K, and the owner may need to cover the $85K operations role. | Year 2 revenue is $1.475M, EBITDA is $274K, and the crew is large enough to support steady install, retrofit, and certification work. | By Year 5, revenue reaches $4.767M, EBITDA is $2.132M, minimum cash is $618K, breakeven is Month 9, and payback takes 30 months. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Near zero to modest payLean ramp | Mid six figures before taxesBase case | Upper six figures to low seven figuresHigh upside |

| Best fit | Use this to stress-test the first year if sales are slow or the owner has to work in the business. | Use this as the working case for budgeting, lenders, and partner talks once the business clears the first-year ramp. | Use this to test upside if staffing holds, job flow stays dense, and cash discipline stays tight. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Audio Visual Wiring Installation Porter's Five Forces Analysis

- Audio Visual Wiring Installation BCG Matrix

- Audio Visual Wiring Installation Business Model Canvas

- What Are The 5 KPIs For Audio Visual Wiring Installation Business?

- Audio Visual Wiring Installation Business Plan Template in Pre-Written Word

- How Increase Audio Visual Wiring Installation Profits?

- What Are Operating Costs For Audio Visual Wiring Installation?

- Audio Visual Wiring Installation Startup Costs: $618K Cash Plan

- Audio Visual Wiring Financial Model Template in Excel

- How To Start An Audio Visual Wiring Installation Business In 6–12 Weeks

- How To Write Audio Visual Wiring Installation Business Plan?

- Audio Visual Wiring Installation Marketing Mix

- Audio Visual Wiring Installation Marketing Plan

- Audio Visual Wiring Installation Business Proposal

- Audio Visual Wiring Installation PESTEL Analysis

- Audio Visual Wiring Installation Pitch Deck Example Editable PPTX

- Audio Visual Wiring Installation Business SWOT Analysis

- Audio Visual Wiring Installation Value Proposition Canvas

Frequently Asked Questions

In this model, Year 1 owner distributions are likely limited because revenue is $661K and EBITDA is -$103K If the owner fills the operations manager role, $85K can be viewed as labor compensation By Year 2, $1475M revenue produces $274K EBITDA before taxes, reserves, debt service, and owner distributions