Owner income$180K + upside

Owner income$180K + upsideHow Much Auditing Firm Owners Make: $180K Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180K + upside  Net margin20.7% to 68.4%

Net margin20.7% to 68.4% Revenue for target pay$1.71M to $16.5M

Revenue for target pay$1.71M to $16.5M Business difficultyHard

Business difficultyHard

An auditing firm owner in this model earns a $180,000 Lead CPA / Partner salary, plus potential distributions from firm profit Based on the researched assumptions, EBITDA rises from $353K in Year 1 to $1128M in Year 5, but not all EBITDA is owner cash The quick math implies revenue of about $171M in Year 1 and $1650M in Year 5 after payroll, marketing, fixed overhead, and variable project costs Treat these as planning assumptions, not guaranteed salary, tax results, or distributions

Owner income$180K + upsideNet margin20.7% to 68.4%Revenue for target pay$1.71M to $16.5MBusiness difficultyHardWant to test your audit firm owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, labor, overhead, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

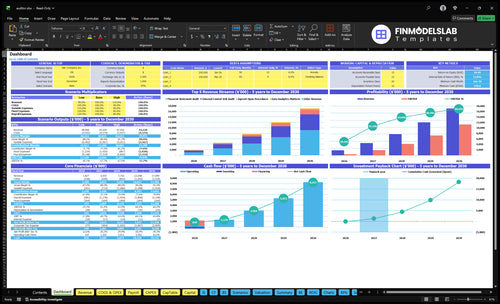

Want to check owner income in the Auditing Firm model?

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the Auditing Firm Financial Model Template to test them.

Owner-income model highlights

- Owner take-home output

- Revenue and EBITDA charts

- Month 6 breakeven test

What is a good profit margin for an auditing firm?

If you’re asking what a good profit margin looks like for an Auditing Firm, the model points to very high margins: 87% gross margin in Year 1 and 91% in Year 5, with 76% to 83% contribution margin. If you’re sizing launch costs, see What Is The Estimated Cost To Open And Launch An Auditing Firm? so you can judge margin against the upfront spend.

Margin levels

- 87% gross margin in Year 1

- 91% gross margin in Year 5

- 76% to 83% contribution margin

- 207% Year 1 EBITDA margin

Cash reality

- Realized rates drive the margin

- Scope control protects write-downs

- Staff leverage raises profit fast

- Owner cash is lower after reserves

How much revenue does an audit firm need to pay the owner?

An Auditing Firm needs about $1.24M in annual revenue to cover its Year 1 fixed stack, because $944K of payroll, overhead, and marketing divided by a 76% contribution margin equals about $1.24M. At the modeled $1.71M of Year 1 revenue, EBITDA comes out near $353K before reserves and taxes. If you want owner pay above the $180K partner salary already inside payroll, add the extra draw and divide by 76%.

Fixed-cost break-even

- 24% variable and project costs

- 76% contribution margin left

- $590K payroll in Year 1

- $204K overhead plus $150K marketing

Owner pay math

- $180K partner salary is inside payroll

- $944K fixed stack needs coverage

- $1.24M revenue covers that stack

- $1.71M modeled revenue leaves $353K EBITDA

Can a solo audit firm owner make more than a staffed audit firm owner?

Yes, a solo owner can keep more of each collected dollar, but a staffed Auditing Firm can make more total profit once demand pushes past one person’s capacity. In the staffed model, the firm starts with 6 FTEs and about $590K payroll in Year 1, then reaches 17 FTEs and $166M payroll in Year 5, with revenue support rising from about $171M to $1650M. The catch is simple: solo works best when client load and review risk stay small; staffed wins when audit complexity and billable hours need a bigger bench.

Solo owner

- Keeps more per collected dollar.

- Hits capacity faster.

- Review quality gets harder alone.

- Best for simpler audits.

Staffed firm

- Starts with 6 FTEs.

- Year 1 payroll is $590K.

- Year 5 reaches 17 FTEs and $166M payroll.

- More staff supports more revenue capacity.

Want to see what drives audit firm owner income?

1

10%-45%Engagement Mix

Growing analytics work from 10% to 45% shifts revenue toward scalable services and lifts owner income without a full jump in sales effort.

2

$160-$240/hrHourly Rate

At $160-$240 an hour, each pricing step up drops straight to take-home if collected rates stay close to billed rates.

3

$590K-$1.66MPayroll Load

Payroll growth buys more billable capacity, but only if the team stays utilized and partner time stays focused on client work.

4

76%-83%Contribution Margin

With a 76%-83% contribution margin, small project cost leaks can cut profit fast, while tight delivery keeps more cash for the owner.

5

$204KOverhead Control

$204K of fixed overhead sets the break-even floor, so rent, insurance, tech, and compliance spend decide how fast profit starts.

6

$539KCash Runway

$539K of minimum cash and Month 6 breakeven mean collections and owner draws need to stay tight early on.

Auditing Firm Core Six Income Drivers

Engagement Volume And Client Mix

Client Mix Drives Audit Capacity

More recurring audit and assurance work can lift owner income because it fills staff time with steadier billing and less sales churn. In the model, financial statement audits rise from 80% to 92%, Sarbanes-Oxley Act internal-control work from 30% to 50%, agreed-upon procedures from 25% to 35%, and data analytics work from 10% to 45%. Engagements run from 15 to 70 hours, so mix changes both revenue and capacity.

Here’s the tradeoff: complex work can support higher fees, but it also increases review time and liability. If staffing does not keep pace, the added work can slow delivery and delay owner pay. Stronger mix supports EBITDA (earnings before interest, taxes, depreciation, and amortization) only when the team can absorb the extra documentation and quality control.

Track Hours, Mix, and Review Load

Measure mix by engagement type, billable hours, and turnaround time. The key inputs are client count, average hours per job, billed rate, rework, and review time. A simple forecast should show how a shift toward more recurring work changes collected revenue, labor cost, and cash timing before the partner draws money.

- Track hours by engagement type.

- Watch review time per file.

- Price complex work for risk.

- Limit scope creep fast.

- Match staffing to recurring work.

1

Average Fee And Realization Rate

Average Fee and Realization Rate

Average fee is the rate you bill, and realization rate is what you actually collect after write-downs. For this firm, source hourly rates are $180 to $200 for financial statement audits, $220 to $240 for internal-control work, $170 to $190 for agreed-upon procedures, and $160 to $180 for data analytics work.

The inputs are service mix, billable hours, scope changes, and billed-versus-collected revenue. A 10% write-down on 100 hours at $200 per hour cuts revenue by $2,000. That loss hits contribution dollars before fixed costs are covered, so it can delay owner pay even when the schedule is full.

Protect Realized Revenue

Track realization by engagement type, manager, and client. Use a simple formula: realized revenue = billable hours × standard rate × realization rate. If the rate is slipping, the fix is usually scope control, not more volume. One line to watch: fees billed minus fees written down.

Require change orders before extra work starts, review pre-bills before invoices go out, and bill fast on completed work. That keeps cash moving and protects margin. If write-downs keep rising, the firm is giving away time that should fund overhead and owner distributions.

2

Staff Leverage And Utilization

Staff Leverage And Utilization

Utilization means the share of available staff hours that bill to clients. In this model, trained staff let the owner review more work instead of doing all fieldwork, so the same partner can support more audit volume. That matters because staffing grows from 6 FTEs in Year 1 to 17 FTEs in Year 5, while payroll rises from $590K to $166M.

Owner income improves only when billable hours and realization cover that payroll load. Senior auditors at $110K and junior auditors at $70K can raise output, but audit work has strict quality-control limits. If review time, documentation, and training lag, leverage turns into rework, and the owner keeps paying salary before distributions grow.

Improve Utilization Before Adding Headcount

Track utilization by role, not just firm-wide. Use three inputs: billable hours, review hours, and nonbillable training. If juniors are busy but the partner is buried in review, leverage is fake; cash still gets tied up in payroll before distributions. Here’s the quick math: more hours help only when the work is reviewable, documented, and collectible.

Build staffing plans around engagement mix, then test whether each added FTE lowers owner fieldwork. If onboarding or review standards slip, quality risk rises fast and margin can fall even while revenue grows. Keep one rule: no headcount step-up until training, templates, and review capacity are in place.

3

Labor Gross Margin

Labor Gross Margin

Labor gross margin is the spread left after direct delivery costs and variable costs. Here’s the quick math: direct costs fall from 24% of revenue in Year 1 (13% COGS plus 11% variable costs) to 17% in Year 5 (9% plus 8%), so contribution margin improves from 76% to 83%. That cash funds overhead, reserves, and owner pay.

The risk is labor leakage. Overtime, contractor help, rework, and training time can turn a priced engagement into low-margin work even when billings look fine. Payroll is separate and material at $590K to $166M, so the owner’s take-home income depends on keeping delivery hours inside the fee.

Track direct labor by engagement

Measure billed hours, overtime, contractor hours, rework, and training time on every job. Then compare direct labor dollars to fee dollars so you can see which engagements land near the 76% to 83% contribution range and which ones quietly destroy margin.

- Fee per engagement

- Direct labor hours

- Overtime and contractor use

- Rework and training time

Use scope control and change orders before work starts, not after overruns hit. If a job needs extra review or outside help, reprice it fast. One clean rule: when direct labor slips, gross profit falls first, and owner distributions follow.

4

Operating Costs And Compliance Overhead

Fixed Burn and Compliance Load

This driver is the cash drain between billings and owner pay. With $17K per month in fixed overhead, that is $204K a year before any owner draw. The model also includes $8K rent, $15K professional liability insurance, $25K IT and security, $800 compliance fees, and $3K platform maintenance, so overhead can eat cash fast before scale.

Marketing also rises from $150K to $550K, which pushes breakeven higher. If recurring overhead grows faster than billable hours or realization, distributable cash falls even when engagements are profitable. The owner’s income depends on how quickly revenue covers this burn and leaves room for taxes, reserves, and pay.

Track Burn Before Draw

Measure overhead as a share of collected revenue, not just booked work. Track rent, insurance, IT, compliance, platform maintenance, and marketing each month so you can see which cost is fixed and which can flex with volume. Here’s the quick math: $17K per month of fixed overhead must be covered before profit turns into owner cash.

- Review overhead every month.

- Split fixed and semi-fixed costs.

- Approve marketing by payback.

- Cut tools that save no hours.

- Hold cash for slow collections.

Busy audit periods can look profitable while cash is tight. If overhead stays high before breakeven, the owner may need to keep distributions low until collections, utilization, and realization are stable.

5

Cash Reserves And Owner Distributions

Cash Reserves and Owner Distributions

When audit work is profitable on paper but receivables are still outstanding, the owner can’t safely pull cash. The model shows a $539K minimum cash need at Month 6, with breakeven also in Month 6 and 15 months to pay back launch capex.

This driver depends on billable partner time, collection speed, fixed overhead, and the owner’s draw policy. $350K of launch capex is tied up up front, and slow collections during busy audit periods can delay distributions even when EBITDA looks healthy.

Protect cash before taking draws

Track ending cash, days sales outstanding (DSO, the average days to collect invoices), and work-in-process every month. If collections slip, hold distributions until cash stays above the reserve floor. The clean test is simple: profit does not fund the owner unless cash is actually in the bank.

- Watch partner billable hours.

- Separate management time from billing time.

- Invoice fast after fieldwork ends.

- Chase overdue receivables weekly.

- Forecast draws only after reserves.

Strong collections turn EBITDA into safer owner pay; weak collections turn the same profit into a cash squeeze. In this model, that squeeze is worst before and around breakeven, when the firm is still absorbing startup capex and audit season timing delays.

6

Scenario objective: Compare lean, base, and high audit firm owner income scenarios

Owner income scenarios

Owner income shifts as billable hours, staffing, and project costs scale. The low case reflects an early team, while the high case assumes a fuller bench and more leveraged delivery.

| Scenario | Low CaseEarly scale | Base CaseStaffed growth | High CaseMature leverage |

|---|---|---|---|

| Launch model | The low case shows an early earnings path with a lean team and tight reserves. | The base case models a staffed practice with deeper billable hours and a broader service mix. | The high case assumes a mature leveraged practice with more senior staff and higher billable capacity. |

| Typical setup | Year 1 maps to about $171k revenue and $353k EBITDA, with about $590k payroll, a 207% EBITDA margin, and a $180k partner salary. | Year 3 maps to about $742k revenue and $4.175M EBITDA, with about $1.17M payroll, a 563% EBITDA margin, and stronger project plus variable costs. | Year 5 maps to about $1.65M revenue and $11.28M EBITDA, with about $1.66M payroll and a 684% EBITDA margin in a fully scaled setup. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $353k - $533kLow income band | $4.18M - $4.36MBase income band | $11.28M - $11.46MUpside income band |

| Best fit | Use this to stress-test the business if growth starts slow or staffing stays lean. | Use this as the core planning case for a growing, well-staffed firm. | Use this to test upside if the firm scales fast and keeps delivery highly leveraged. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Auditing Firm Porter's Five Forces Analysis

- Auditing Firm BCG Matrix

- Auditing Firm Business Model Canvas

- 7 Critical KPIs for Scaling an Auditing Firm

- Auditing Firm Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Auditing Firm Profitability and Margin

- Analyzing the Monthly Running Costs for an Auditing Firm

- Auditing Firm Startup Costs: $350K CAPEX And $539K Cash Need

- Auditing Firm Financial Model Template in Excel

- How To Open An Auditing Firm In 60–120 Days

- How to Write an Auditing Firm Business Plan: 7 Steps to Funding

- Auditing Firm Marketing Mix

- Auditing Firm Marketing Plan

- Auditing Firm Business Proposal

- Auditing Firm PESTEL Analysis

- Auditing Firm Pitch Deck Example Editable PPTX

- Auditing Firm Business SWOT Analysis

- Auditing Firm Value Proposition Canvas

Frequently Asked Questions

Owner income is different because it includes business risk and profit In this model, the Lead CPA / Partner salary is $180,000, while EBITDA is $353K in Year 1 and $1128M in Year 5 The owner may receive salary plus distributions, but only after reserves, capex, debt service, collections, and taxes are handled