Owner income-$121k to $267k

Owner income-$121k to $267kHow Much Auto Diagnostic Service Owners Make: $47k–$267k

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$121k to $267k  Net margin78%

Net margin78% Revenue for target pay$27k/mo

Revenue for target pay$27k/mo Business difficultyHard

Business difficultyHard

Key Takeaways

- Only billed diagnostics count toward revenue.

- Ticket mix drives income more than volume alone.

- Owner labor masks true replacement cost early.

- Rework and unpaid time eat paid capacity.

Owner income-$121k to $267kNet margin78%Revenue for target pay$27k/moBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed and this is not salary, tax, or owner distribution advice.

Want to check owner income in Auto Diagnostic Service?

Open the Auto Diagnostic Service Financial Model Template for revenue, EBITDA, runway, break-even, payback, and owner pay.

Owner-income model highlights

- Assumptions tab drives inputs

- Mix, hours, price, CAC

- Marketing, payroll, fixed costs

- COGS, variable expenses, capex

- Owner pay scenarios included

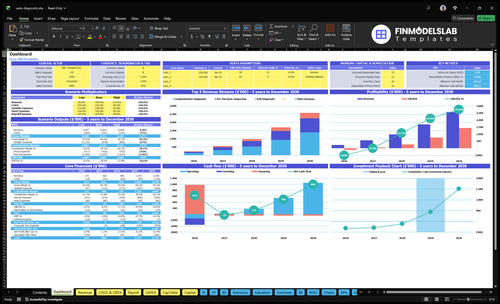

- EBITDA: -$121k to $1.443M

- Base, lean, high cases

What costs affect auto diagnostic service profit the most?

For an Auto Diagnostic Service, payroll is the biggest profit swing: it starts at $165k in Year 1 and rises to $430k by Year 5. If you want the launch math, see What Is The Estimated Cost To Launch Your Auto Diagnostic Service Business? Marketing matters too, but it is smaller than labor, at 10% of revenue in Year 1 and 7% by Year 5, with budget moving from $25k to $110k.

Biggest margin drag

- Payroll dominates cost growth.

- Year 1: $165k.

- Year 5: $430k.

- Unpaid rework hurts margin fast.

Other cost pressure

- Marketing falls from 10% to 7%.

- Budget rises from $25k to $110k.

- Software and data drop from 5% to 3%.

- Tools and training ease from 3%/4% to 2%/3%.

How much revenue does an auto diagnostic service need to pay the owner?

For Auto Diagnostic Service, the quick answer is about $267k per month, or $3.208M per year, to cover Year 1 fixed overhead and payroll at a 78% contribution margin. If the owner wants $100k in pre-tax pay, plan on about $128k more revenue, assuming the same margin. This is before any debt service, extra reserves, or other owner draws.

Break-even load

- $71k fixed overhead monthly

- $165k payroll annually

- 78% contribution margin used

- $3.208M yearly break-even revenue

Owner pay add-on

- $100k pre-tax owner pay target

- Revenue rises by about $128k

- Assumes the 78% margin holds

- Debt service lifts the target further

How much can an auto diagnostic service owner make?

An Auto Diagnostic Service owner can make either an operator wage or business profit, and those are not the same. In the staffed model, EBITDA moves from -$121k in Year 1 to $1.443M in Year 5; track the drivers here: What Is The Current Growth Trend Of Your Auto Diagnostic Service Business?.

Owner income split

- Year 1 EBITDA: -$121k

- Year 2 EBITDA: $47k

- Year 3 EBITDA: $267k

- Year 4 EBITDA: $764k

Main pay drivers

- Year 5 EBITDA: $1.443M

- Owner-operator labor value: $85k

- Depends on paid appointments

- Watch utilization and rework

Want the six income drivers?

1

Month 18Billable Volume

More paid diagnostics push the shop to breakeven by Month 18; if jobs are thin, fixed payroll and rent stay heavy.

2

$231Ticket Mix

Year 1 blended ticket is about $231, so more pre-purchase and B2B work lifts revenue per visit without adding bays.

3

$165KTechnician Load

Year 1 payroll is about $165K, so billed hours per tech decide how much labor turns into owner income.

4

$150Acquisition Flow

Year 1 CAC is $150, so cheaper referrals and repeat calls protect cash as ad spend scales.

5

22%Cost Load

Year 1 variable cost load is about 22%, and keeping software, tools, training, and ads tight protects margin.

6

1.5-3.0hUnpaid Time

Every unpaid comeback can burn 1.5-3.0 billed hours, so tighter checks and scope control stop margin leakage.

Auto Diagnostic Service Core Six Income Drivers

Billable diagnostic volume

Billable Diagnostic Volume

Revenue only comes from completed, billed jobs, not free estimates, unpaid troubleshooting, or courtesy scans. At the benchmark, 27 paid appointments per week at a $231 blended ticket and 78% contribution is the Year 1 break-even point; that’s about $6.2k weekly or $27.0k monthly in billed sales before fixed costs.

The owner wins when paid volume matches technician capacity and stays clean on first visit. Rework eats the gain because labor time gets spent twice. Best-fit work is scheduled check-engine diagnostics, paid inspections, and B2B troubleshooting.

Track Billed Jobs, Not Visits

Track only authorized, completed, and invoiced jobs. Measure weekly booked appointments, billed appointments, average ticket, and comeback rate. If free scans or no-fault-found visits rise, the shop looks busy but cash and owner pay do not.

- Count paid jobs per tech weekly.

- Separate free scans from billed work.

- Flag rework before invoicing.

Protect scope with written approval, standard test plans, and a minimum diagnostic fee. The goal is more billed hours, fewer repeats, and a higher share of work that keeps the 78% contribution intact.

1

Average ticket and service mix

Average Ticket and Service Mix

When the mix shifts from basic code scans to professional diagnostics, each visit earns more. The blended ticket is about $231 in Year 1 from comprehensive diagnostics, pre-purchase inspections, and B2B diagnostics, then rises to about $270 by Year 5. That is $39 more per job, or roughly 17%, before extra labor or rework.

What moves owner income is not just more appointments; it’s more revenue per booked slot with the same technician time. The inputs are paid jobs by type, pricing, mix %, and technician minutes. If basic scans are priced too close to deep troubleshooting, the average ticket stays low and owner pay gets squeezed.

Protect the blended ticket

Track revenue by service line, not just total sales. Split basic code scans, electrical troubleshooting, module testing, advanced inspections, and pre-purchase inspections so you can see where the average ticket is rising or falling.

- Set a minimum fee for every job.

- Quote scope before testing starts.

- Price advanced work separately.

- Watch revenue per booked hour.

If higher-ticket work takes too long, the extra revenue gets eaten by labor and cash flow slows. The clean target is simple: keep the mix moving toward deeper diagnostics so each appointment pays enough to cover technician time and still leave profit for the owner.

2

Technician productivity and owner labor

Owner Labor vs. Technician Scale

Owner-performed diagnostics can boost early cash because you’re not paying someone else to replace the owner. But that can hide the real labor load later. Year 1 staffing already implies $165k in payroll: $85k lead diagnostic technician or manager, $60k diagnostic technician, and $20k half-time admin. If paid work does not stay dense, take-home drops fast.

Track Paid Hours, Not Just People

Watch billable hours, documentation, and first-visit resolution before you hire around the owner. The owner’s labor should be loaded into the model like any paid technician, or profit will look better than it is. One clean rule: if a hired tech cannot match the owner’s diagnostic quality, the new payroll cuts owner income instead of scaling it.

- Billable hours per tech

- First-visit resolution rate

- Documentation completeness

- Owner hours in diagnostics

- Payroll by role

3

Tool and software cost control

Tool and software cost control

Diagnostic gear is both a cost and a sales tool. Year 1 needs $75k in advanced scanners, $60k in lifts and workshop equipment, $20k in perpetual software licenses, and $10k in tools and handheld devices, so the owner has to estimate this from revenue, job mix, and tool usage. If the gear does not increase billed diagnostics or ticket size, it just ties up cash.

Recurring software and data costs run 5% of revenue in Year 1 and 3% in Year 5; maintenance and calibration add 3% then 2%. So recurring tool cost falls from 8% of revenue to 5% as the business scales, and owner pay improves only when the tools support higher-value work, not idle shelves.

Buy for billable use

Track each tool by billed jobs, first-visit fix rate, and time saved per repair. Here’s the quick math: a tool earns its keep only if it helps sell more advanced diagnostics, cuts rework, or raises the average ticket.

- Review software renewals before auto-renewal.

- Schedule calibration instead of delaying it.

- Retire tools with low job usage.

- Buy only for paid diagnostic work.

What this hides: a pricey scanner still hurts income if it does not turn into more billed appointments or better-margin inspections. Use the tool set to support the work mix, not just to look fully equipped.

4

Customer acquisition and referral flow

Paid Lead Flow

Qualified paid demand matters because only booked, paid diagnostics fill technician time. At $25k in Year 1 marketing spend and $150 CAC, the budget supports about 167 paid customers. By Year 5, $110k at $80 CAC supports about 1,375. More referrals, fleets, used-car buyers, and local search leads mean less idle time and better owner take-home pay.

The main inputs are paid leads, booked jobs, show rate, and B2B mix. Moving B2B from 10% to 20% can smooth scheduling because shop and fleet referrals are steadier than one-off walk-ins. The risk is simple: cheap traffic that does not show, accept scope, or pay for troubleshooting raises CAC without lifting profit.

Measure Lead Quality

Track each source by booked rate, paid rate, and CAC. A referral that shows up and approves scope is worth far more than a low-cost click. Here’s the quick math: if CAC falls from $150 to $80, the same budget buys more paid diagnostics before payroll and overhead squeeze margin.

Set a minimum fee, confirm scope before arrival, and steer repair shops, fleets, and used-car buyers into scheduled diagnostics. That keeps technicians on billable work, not free checks, and protects cash flow when demand is uneven.

5

Rework, warranty, and unpaid diagnostic time

Rework and Unpaid Diagnostic Time

Rework, warranty, and no-fault-found jobs can shrink owner pay even when booke d revenue looks fine. Every unpaid hour still uses technician time, and with $165k starting payroll plus $71k of fixed overhead per month, margin falls fast if comebacks and vague estimates keep turning into free work.

The key inputs are paid jobs, comeback rate, warranty hours, no-fault-found rate, and how often the scope is written and approved up front. Fewer repeat visits mean more paid capacity; more repeats mean the same staff must absorb more unbilled labor, which cuts cash available for the owner.

Control the scope before the wrench turns

Track billed hours versus actual technician hours, plus comeback rate and no-fault-found rate. Use test plans, authorization limits, and written scope so extra probing gets approved before it starts. That keeps the job from turning into free labor and protects revenue quality.

One line to remember: unbilled time is still labor cost. If a fault is unresolved, stop and re-quote instead of stacking on more unpaid diagnosis. Tight documentation lowers repeat visits and frees capacity for paid work without adding headcount.

- Count warranty hours each week.

- Split billed and unbilled time.

- Log no-fault-found outcomes.

- Require written scope approval.

- Track comeback rate by technician.

6

Compare lean, base, and high-performance auto diagnostic owner-income scenarios

Owner income scenarios

Owner income swings with paid volume, service mix, and payroll. Early ramp is cash heavy, then earnings improve as Year 2 to Year 3 EBITDA turns positive and the model scales.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the early ramp case, where paid volume stays light and the business still carries launch payroll and overhead. | This is the modeled middle path, where Year 2 to Year 3 earnings turn positive and the owner can start taking a modest draw. | This is the scaled upside case, where the shop runs at much higher volume and owner income can expand fast. |

| Typical setup | Year 1 EBITDA is about -$121k, payroll is about $165k, fixed overhead is about $85.2k, and the owner is still covering day-to-day work and cash gaps before Month 18 breakeven. | EBITDA moves from about $47k in Year 2 to $267k in Year 3 before taxes, debt, and reserves, and the owner shifts from hands-on repair work to running volume and pricing. | EBITDA reaches about $764k in Year 4 and $1.443M in Year 5 as B2B share rises, CAC falls to $95-$80, and the owner acts more like a manager than a technician. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No owner drawLow case | $47k - $267kBase case | $764k - $1.443MHigh case |

| Best fit | Use this to test survival if demand is slow and the owner must cover early losses. | This fits founders who want a realistic operating target once the shop has steady demand. | Use this only for a scaled shop with strong referral flow and tight utilization; it is not the typical outcome. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

Related Products

- Auto Diagnostic Service Porter's Five Forces Analysis

- Auto Diagnostic Service BCG Matrix

- Auto Diagnostic Service Business Model Canvas

- 7 Critical KPIs for Scaling an Auto Diagnostic Service

- Auto Diagnostic Service Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Auto Diagnostic Service Profitability

- Analyzing the Monthly Running Costs for an Auto Diagnostic Service

- Auto Diagnostic Service Startup Costs: $215K CAPEX Plus Cash Reserve

- Auto Diagnostic Service Financial Model Template in Excel

- How To Start An Auto Diagnostic Service In 6 To 12 Weeks

- How to Write an Auto Diagnostic Service Business Plan

- Auto Diagnostic Service Marketing Mix

- Auto Diagnostic Service Marketing Plan

- Auto Diagnostic Service Business Proposal

- Auto Diagnostic Service PESTEL Analysis

- Auto Diagnostic Service Pitch Deck Example Editable PPTX

- Auto Diagnostic Service Business SWOT Analysis

- Auto Diagnostic Service Value Proposition Canvas

Frequently Asked Questions

Early profit can be thin or negative if the shop opens with staff In the model, EBITDA is -$121k in Year 1, turns positive at $47k in Year 2, and reaches $267k in Year 3 That is before taxes, debt, reserves, or owner distributions