Owner income$128K–$40.3M

Owner income$128K–$40.3MHow Much AAC Supply Owners Can Make: $128K Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$128K–$40.3M  Net margin10.9%–80.5%

Net margin10.9%–80.5% Revenue for target pay$1.17M

Revenue for target pay$1.17M Business difficultyHard

Business difficultyHard

You’re estimating owner income from an autoclaved aerated concrete supply business, not a fixed employee salary This model shows $117M to $4998M in annual revenue and $128K to $4025M in EBITDA across Year 1 to Year 5, before taxes, debt structure, reserves, and owner distributions

Owner income$128K–$40.3MNet margin10.9%–80.5%Revenue for target pay$1.17MBusiness difficultyHardWant to test your AAC owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

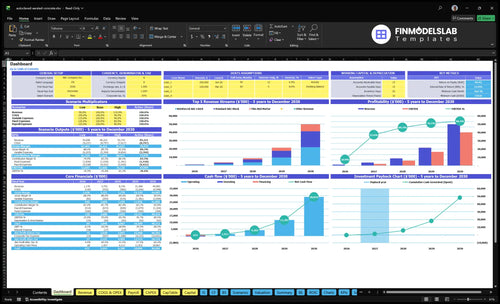

How do you check owner income in the Autoclaved Aerated Concrete Supply financial model?

The dashboard in the Autoclaved Aerated Concrete Supply Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions; open the model.

Owner-income model highlights

- Owner take-home scenarios

- $117M to $4,998M

- Month 4 breakeven

- $533K minimum cash

How sensitive is AAC block supply gross margin to freight and inventory cost?

Yes—freight and inventory are the biggest margin swings in Autoclaved Aerated Concrete Supply. With procurement at 120% of revenue and freight at 70%, there is very little room before fixed overhead and payroll; a 1-point freight miss on $117M revenue cuts about $117K of Year 1 EBITDA capacity, and the same miss on $4,998M revenue cuts about $4,998K in Year 5. For startup cost context, see How Much To Start Autoclaved Aerated Concrete Supply Business?

Freight hits fast

- 1-point miss = $117K loss

- 1-point miss = $4,998K loss

- Unrecovered delivery time cuts take-home

- Freight creep compounds fast

Inventory leaks cash

- Damaged stock lowers gross margin

- Slow-moving block sizes tie up cash

- Discounting to clear stock hurts margin

- Extra inventory raises owner take-home risk

How does scaling an AAC supply business affect owner income?

For Autoclaved Aerated Concrete Supply, scaling can raise owner income, but only if working capital and payroll stay ahead of growth. Here’s the quick math: revenue climbs from $117M in Year 1 to $4,998M in Year 5, while staff grows from 7 FTE to 17 FTE.

Income can rise

- Revenue grows 42.7x by Year 5

- Sales and support rise 2 to 6 FTE

- Warehouse staff rise 3 to 8 FTE

- Owner keeps margin control early

Cash can break the model

- More volume needs more cash

- Payroll must not outrun revenue

- Dispatch and yard labor get added

- Managed ops need tighter cash controls

How much revenue does an AAC supply business need to pay the owner?

If you want $100K in pre-tax owner pay from an Autoclaved Aerated Concrete Supply business, use the model’s own margin, not a universal revenue rule. With $117M of Year 1 revenue and $128K of EBITDA, the business makes about $0.00109 of EBITDA per $1 of sales, so $100K of owner capacity needs roughly $91.7M in revenue before reserves and debt. The quick math is simple: fixed overhead is $255K a month, so freight recovery and order volume matter as much as price.

Owner pay math

- $117M revenue, $128K EBITDA

- 0.109% EBITDA margin

- $91.7M revenue for $100K pay

- Before reserves and debt service

What drives it

- $255K monthly overhead

- Payroll is a material cost

- Freight recovery changes margin fast

- Order volume matters as much as price

What drives AAC supplier owner income?

1

$1.2M-$50.0MSales Volume

Revenue rises from $1.17M in Year 1 to $49.98M in Year 5, so project wins and repeat supply orders drive most owner income.

2

81%-84%Gross Margin

With procurement at 12% to 10% and freight at 7% to 6.2%, the margin pool stays near 81% to 84%, so small price moves matter.

3

$25.5K/moOverhead

Fixed costs hit every month, so lean warehouse, staff, marketing, and testing spend protect cash and lift take-home.

4

7-17 FTEOwner Role

Headcount grows from 7 to 17 FTE, so the owner has to stay on pricing, key accounts, and cash instead of day-to-day work.

5

7%-6.2%Freight Recovery

Delivery costs take 7.0% to 6.2% of revenue, and better routing or chargeback turns that leak into profit.

6

$533KInventory Turns

The model needs $533K minimum cash at month 6, so slow stock turns trap cash and raise funding risk.

Autoclaved Aerated Concrete Supply Core Six Income Drivers

Qualified Demand And Monthly Sales Volume

Qualified Demand Drives Sales Volume

Qualified demand is the count of contractor, builder, and commercial project visitors who are likely to place real orders. In the model, Monday visitors rise from 120 in Year 1 to 400 in Year 5, conversion improves from 20% to 40%, and units per order grow from 450 to 650. That lifts revenue capacity, but only if freight, inventory, and payroll stay tight.

Here’s the quick math: 120 × 20% = 24 orders, then 24 × 450 units; by Year 5, 400 × 40% = 160 orders, then 160 × 650 units. The model shows revenue moving from $117M to $4,998M, but take-home income still depends on gross margin and delivery cost control.

Track Conversion and Order Size

Measure visitor volume, conversion rate, and units per order every month by customer type. Contractor and commercial repeat orders matter most, since they raise sales capacity without rebuilding demand from zero. If conversion stays near 20%, more traffic alone won’t fix profit.

Use a simple test: follow quote-to-order rate, average units per order, and margin after freight on every deal. Match inventory buys to real orders, not just visits. If freight, stock, or payroll rise faster than qualified demand, owner pay gets squeezed even when revenue looks strong.

- Track monthly qualified visitors

- Track quote-to-order conversion

- Track units per order

- Track margin after freight

1

Gross Margin And Pricing Power

Gross Margin And Pricing Power

Gross margin is the money left after procurement cost, and it drives how much cash can reach payroll, overhead, and owner pay. In Year 1, the disclosed mix is 700% standard block, 150% reinforced lintel, and 150% thin bed mortar, with prices of $850, $4,500, and $1,800. If job pricing is off, the owner can sell more and still earn less.

Owner income does not sit on a fixed margin. Procurement cost is modeled to improve from 120% in Year 1 to 100% in Year 5, but discounts, mix, and purchase terms can still move profit per order up or down. One weak discount can wipe out the gain from a better buy price, so price accuracy matters on every quote.

Protect Margin Per Order

Track price realization, which is the cash you actually collect after discounts, against buy cost for each product. If selling price rises faster than procurement cost, owner draw can grow; if buy cost rises first, margin shrinks before fixed costs even change. The clean rule is simple: protect margin before chasing volume.

- Track quoted price by product

- Track discounts by customer

- Track purchase cost by product

- Track mix in each order

- Track gross profit per order

Flag any order where margin falls below plan. That is where cash gets squeezed first, and where pricing discipline has the fastest impact on take-home income.

2

Freight, Delivery, And Handling Economics

Freight Recovery and Delivery Margin

Freight recovery can make or break a sale. In this model, freight and logistics run 70% of revenue in Year 1 and 62% in Year 5, so delivery cost is a major part of margin, not a small add-on. Route planning, unloading time, breakage, jobsite delays, and delivery pricing all feed into net profit and the owner’s take-home pay.

Here’s the quick math: a 1-point freight variance on Year 3 revenue of $873M equals about $873K. That means a sale can look strong on gross revenue and still hurt cash flow if delivery is underpriced or slow. Track margin after delivery, not just gross sales, or owner pay gets squeezed even when orders are growing.

Measure Delivery Cost Per Order

Build each quote from the bottom up: delivery price, unloading time, breakage, and jobsite delay risk. The owner should watch freight recovery percentage by project, then compare it to the model’s 70% Year 1 and 62% Year 5 freight load. If the realized rate slips, profit drops before payroll or owner draw gets paid.

Use a simple control set: route miles, stop count, failed unloads, damaged units, and extra wait time. One clean line matters: if delivery eats the margin, the sale is not profitable. Price by job conditions, document access limits, and test whether faster unloading or tighter routing lowers cost enough to protect cash for supplier payments and owner income.

3

Inventory Turnover And Working Capital

Inventory Turnover And Working Capital

Inventory turnover is how fast blocks, lintels, mortar, and replacement stock sell and get replaced. When slow items, damaged stock, or the wrong sizes sit too long, cash gets trapped and owner pay gets delayed. In this model, breakeven lands in Month 4, but cash still bottoms at $533K in Month 6, so paper profit does not equal spendable cash.

The key inputs are on-hand units, product mix, spoilage, supplier terms, and repeat customer life. Here, repeat customer lifetime grows from 12 to 36 months, which helps planning but raises service expectations. Owner income should come after inventory replenishment, supplier payments, and delivery capacity reserves, or the business can look healthy and still miss cash needs.

Track Turns, Not Just Sales

Measure turns by SKU and watch days on hand for each core item. If stock is not tied to a booked job, it is cash you cannot pay yourself. Keep reorder points linked to project starts, then check damage, aging, and slow movers weekly so cash stays available for the next buy.

- Track aging stock by SKU

- Flag damaged units fast

- Match buys to booked orders

4

Fixed Overhead And Operating Cost Control

Fixed Overhead Break-Even

Fixed overhead is the cash floor. Here, monthly fixed expenses are disclosed at $255K, including warehouse lease $12K, insurance $25K, software $12K, marketing $5K, utilities $18K, and testing $3K. These costs sit outside procurement COGS and freight, so they still hit cash every month even if orders slow.

That means owner income starts only after sales cover both variable costs and this fixed base. If gross profit slips below $255K/month, there is no room for owner pay. Lean facility planning matters because excess space or overhead pushes break-even up and delays take-home cash.

Keep Overhead Below Gross Profit

Track monthly fixed spend against gross profit, not just revenue. Use a simple test: fixed overhead ÷ monthly gross profit. If the gap is thin, cut space, delay hires, and challenge every recurring fee before it becomes permanent. The key inputs are sales volume, gross margin after freight, and the full fixed-cost run rate.

Review lease, insurance, software, utilities, and testing together each month. One extra $10K in fixed cost can wipe out a big share of owner draw when revenue is uneven, so keep the facility and admin setup lean until repeat orders are steady.

5

Owner Role, Staffing, And Management Leverage

Owner Time vs Payroll Leverage

A hands-on owner can keep payroll light, but that usually caps sales and dispatch capacity. In Year 1, the model starts with 1 general manager, 2 sales and technical support, 3 warehouse staff, and 1 administrative assistant. If the owner is covering too many jobs, revenue can stall even when demand is there.

By Year 5, staffing reaches 17 FTE (full-time equivalents), so the key test is simple: added staff must raise gross profit faster than wages. If not, payroll eats the owner’s draw. One clean rule: more headcount only helps when it buys more quote volume, faster delivery, and fewer missed orders.

Track Gross Profit Per Head

Measure gross profit per employee, owner hours spent on selling, and dispatch time per order. Those three numbers show whether staffing is freeing the owner or just adding cost. If a role does not lift order flow, reduce rework, or speed deliveries, it is not supporting owner income.

Test staffing against capacity, not hope. For this business, the useful inputs are inquiry volume, conversion rate, orders per rep, warehouse throughput, and payroll by role. Keep the owner in the high-value work: pricing, key accounts, and problem jobs. Use staff to protect margins and cash flow, not just to fill a schedule.

6

Compare low, base, and high AAC owner income scenarios

Owner income scenarios

Owner income moves with traffic, conversion, freight recovery, and staffing. The model scales from $1.17M revenue and $128k EBITDA in Year 1 to $49.98M and $40.25M in Year 5.

| Scenario | Low CaseDemand risk | Base CaseWorking capital | High CaseStaffing complexity |

|---|---|---|---|

| Launch model | This is the lower-earnings path if orders run light and freight costs stay hard to pass through. | This is the modeled path if volume, mix, and pricing follow plan. | This is the stronger-earnings path if volume, mix, and pricing all beat plan. |

| Typical setup | Year 1 traffic stays near the low conversion case, the mix skews to standard block, and fixed overhead plus payroll absorb most gross profit. | Revenue rises from $1.17M in Year 1 to $3.75M in Year 2, while EBITDA moves from $128k to $2.09M as better mix and freight recovery offset staffing growth. | By Year 5, revenue reaches $49.98M and EBITDA reaches $40.25M as higher conversion, larger orders, and a richer mix spread fixed costs across more shipments. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $128kFreight exposure | $128k - $2.1MModeled base | $2.1M - $40.3MUpside scale |

| Best fit | Use this to stress-test early demand, freight pass-through, and cash draw before scale. | Use this as the working case for budgets, hiring, and lender talks. | Use this to test ceiling cases, warehouse strain, and staff needs at faster growth. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Autoclaved Aerated Concrete Supply Porter's Five Forces Analysis

- Autoclaved Aerated Concrete Supply BCG Matrix

- Autoclaved Aerated Concrete Supply Business Model Canvas

- What Are The 5 KPIs For Autoclaved Aerated Concrete Supply Business?

- Autoclaved Aerated Concrete Supply Business Plan Template in Pre-Written Word

- How Increase Autoclaved Aerated Concrete Supply Profits?

- What Are Operating Costs For Autoclaved Aerated Concrete Supply?

- AAC Block Supplier Startup Costs: $420K CAPEX Plus $533K Cash

- Autoclaved Aerated Concrete Supply Financial Model Template in Excel

- How To Open An AAC Block Supply Business In 8–16 Weeks

- How To Write A Business Plan For Autoclaved Aerated Concrete Supply?

- Autoclaved Aerated Concrete Supply Marketing Mix

- Autoclaved Aerated Concrete Supply Marketing Plan

- Autoclaved Aerated Concrete Supply Business Proposal

- Autoclaved Aerated Concrete Supply PESTEL Analysis

- Autoclaved Aerated Concrete Supply Pitch Deck Example Editable PPTX

- Autoclaved Aerated Concrete Supply Business SWOT Analysis

- Autoclaved Aerated Concrete Supply Value Proposition Canvas

Frequently Asked Questions

The researched model shows $128K EBITDA in Year 1 on $117M revenue, rising to $4025M EBITDA on $4998M revenue by Year 5 That is business profit capacity before taxes, debt structure, reserves, and distributions Owner take-home should be lower when cash is needed for inventory, trucks, payroll, or payables