Owner income$145k

Owner income$145kHow Much an Avalanche Forecasting Service Owner Makes by Year 2

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145k  Net margin-1.6% to 63.8%

Net margin-1.6% to 63.8% Revenue for target pay$426k

Revenue for target pay$426k Business difficultyHard

Business difficultyHard

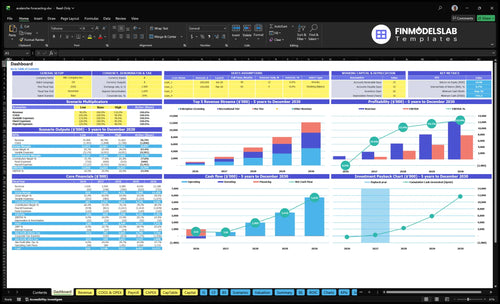

Using the researched assumptions, the model carries a $145,000 CEO salary as owner pay before taxes Year 1 revenue is $1026M, but EBITDA is -$16,000, so a profit distribution is not supported without outside cash By Year 2, revenue reaches $2456M and EBITDA reaches $835,000, creating room for reserves, reinvestment, debt service, or added owner distributions These are planning assumptions, not guaranteed earnings

Owner income$145kNet margin-1.6% to 63.8%Revenue for target pay$426kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Need the model behind the math for Avalanche Forecasting Service?

The Avalanche Forecasting Service Financial Model Template shows revenue, EBITDA, cash, payback, and owner-pay outputs, so you can check the math fast.

Owner-income model highlights

- Owner-pay output shown

- Revenue and EBITDA tracked

- Scenarios test key drivers

Can an avalanche forecasting service support a full-time owner?

Yes, Avalanche Forecasting Service can fund a full-time owner in the supplied model: it pays a $145,000 CEO salary in Year 1, but still posts -$16,000 EBITDA, so the safer full-time point is Year 2. For the operating metrics behind this call, see What Are The Five KPIs For Avalanche Forecasting Service?; the model reaches break-even in Month 7, payback in Month 22, and $2.456M in Year 2 revenue with $835,000 EBITDA.

Owner Income

- Year 1 CEO salary: $145,000

- Year 1 EBITDA: -$16,000

- Safer threshold: Year 2

- Year 2 EBITDA: $835,000

Risk Checks

- Watch subscriber conversion closely

- Secure institutional contracts early

- Set a cash reserve policy

- Define owner operating workload

What avalanche forecasting business costs most affect profit margin?

If you’re sizing the unit economics in What Are The Five KPIs For Avalanche Forecasting Service?, the biggest margin hit is forecaster and technical payroll, then weather data, payment fees, and cloud infrastructure. Here’s the quick math: $500,000 payroll in Year 1, plus 9% data fees and 10% payment costs, leaves little room until recurring revenue gets bigger.

Big fixed costs

- Forecaster and technical payroll hit first.

- $500,000 payroll in Year 1.

- $150,000 marketing in Year 1.

- Owner pay tightens if staffing rises early.

Recurring cost drag

- 9% data fees on Year 1 revenue.

- 10% payment costs on Year 1 revenue.

- $1,200 insurance per month.

- $2,000 travel and field testing per month.

Should the owner stay solo or hire forecasters?

For Avalanche Forecasting Service, staying solo protects cash, but it also caps coverage, review depth, and contract capacity. The source model is not solo: it starts Year 1 with a CEO, senior data scientist, developer, and lead meteorologist, with payroll at $500,000 and rising to $1.445M by Year 5. Hiring only makes sense when subscriber revenue and contract revenue cover payroll plus reserves without weakening forecast standards.

Stay Solo

- Protects cash early.

- Limits terrain coverage.

- Reduces review depth.

- Caps contract capacity.

Hire Forecasters

- Expands route coverage.

- Supports enterprise work.

- Adds payroll and training.

- Raises liability exposure.

Want to see the six owner-income levers?

1

$1.0MPaid Subscribers

This recurring base drives most take-home because Year 1 revenue is $1.026M, and the model reaches breakeven in Month 7.

2

$51K-$1.22MInstitutional Contracts

Enterprise licensing adds high-margin revenue as mix grows from 5% to 10%, so each win lifts cash with limited extra labor.

3

7moForecast Season

A longer usable season means more paid forecasts and stronger reserve build, and the business already needs seven months to clear breakeven.

4

1.5xAssessment Pricing

Higher assessment fees lift average revenue per user and help offset CAC falling from $25 to $18 as the customer base scales.

5

$500KStaffing Efficiency

Year 1 payroll is $500K, so adding headcount before demand supports it cuts margin and slows owner cash.

6

81%Cost Control

Cloud, insurance, and field spend can erode cash fast, so keeping direct costs near 19% protects the 81% gross margin.

Avalanche Forecasting Service Core Six Income Drivers

Paid Subscriber Base

Paid Subscriber Base

Your take-home rises when the paid base grows faster than churn. Income here comes from subscriber count × conversion rate × renewal rate × monthly price. With the Year 1 mix, the weighted price is $28.50/month (75% recreational at $12, 20% pro at $35, 5% enterprise at $250).

CAC is $25 in Year 1 and improves to $18 by Year 5, so payback depends on trust, forecast quality, regional coverage, and clear legal positioning. If renewals weaken, recurring revenue turns into seasonal churn, and owner cash flow gets squeezed even when new sign-ups look fine.

Protect Renewal and CAC

Track trial-to-paid conversion, monthly renewal, and CAC by tier. Compare the $25 Year 1 CAC with first-year gross profit, then only scale spend where renewal stays strong. Keep region coverage, forecast cadence, and legal terms tight so the paid base compounds instead of resetting every season.

- Measure renewal by plan.

- Cut spend on weak regions.

- Publish forecast update timing.

- Spell out liability limits.

1

Institutional Contract Revenue

Institutional Retainers

Institutional contracts add steadier cash than individual subscriptions. In Year 1, 5% of customers are enterprise accounts at $250 per month, rising to 10% at $300 per month by Year 5. That mix can lift owner take-home because sales time is concentrated, but only if scope, response times, and liability terms stay tight.

Here’s the quick math: revenue depends on account count, retainer price, renewal rate, and service scope. The hidden risk is local avalanche exposure and support load; if one contract demands constant custom work, margin can shrink fast even when top-line revenue looks stable.

Track Scope Before You Scale

Price each contract around what you can deliver: forecast access, response timing, and any custom briefings. Track monthly retainer, hours per account, renewal rate, and support tickets. If one account needs more than its fee covers, raise price or narrow the scope.

- Separate guide, muni, and event terms.

- Cap turnaround times in writing.

- Review liability language before signing.

- Test local coverage before renewal.

2

Forecast Season Length

Forecast Season Length

Forecast season length is the number of operating days that can generate subscriptions, renewals, custom assessments, and contract work. When the season is longer, revenue has more days to build; when it is thin, demand falls but $10,000 per month in fixed overhead still runs. That gap hits owner pay fast, because fewer active days mean less cash to cover staff, tools, and profit draw.

The model should not assume a uniform winter. It should let users edit season length by region and year, since climate variability, regional snowpack, storm cycles, and thin seasons can change demand. The stated source revenue rises from $1026M in Year 1 to $2456M in Year 2, so even small changes in operating days can move take-home income a lot.

Track Days, Not Just Sales

Measure season length in operating days, then tie it to active subscribers, renewal rate, and custom assessment volume. Here’s the quick math: more days usually means more billing cycles, but if demand collapses in a short season, monthly revenue can still miss fixed costs. One weak month can erase a good stretch if you do not forecast by region.

- Track days open by region.

- Model renewals by month.

- Stress test thin-season demand.

- Keep fixed overhead at $10,000.

- Edit season length in the calculator.

What this estimate hides: storm timing, early melt, and local snowpack can shift revenue even if subscriber count looks stable. If a region loses 20 to 30 operating days, owner income can fall because subscription sales, add-on assessments, and contract value all shrink while overhead stays put.

3

Custom Assessment Pricing

Custom Assessment Pricing

Premium work like trip-specific avalanche assessments, terrain briefings, snowpack reviews, training, and corporate safety consulting can raise revenue per client when trust is high and capacity is tight. The key math is simple: monthly custom revenue = assessment fee × monthly volume. If the fee does not cover expert time, the owner is just selling more work, not more profit.

This driver only helps take-home pay when pricing also covers delivery labor, review workflow, insurance load, and documentation. The main risk is vague scope, which can trigger rework and liability. One unclear assessment can wipe out the margin from several clean jobs, so scope and sign-off matter as much as the price.

Price the scope, not the trip

Track fee per assessment, monthly volume, and hours per delivery on every custom job. If the work takes more review time or field follow-up than planned, raise the fee or narrow the scope. The owner keeps more cash only when each job pays for expert labor, insurance, and documentation before overhead hits.

- Log scope, hours, and rework.

- Quote separate fees for consulting.

- Require written client sign-off.

- Track margin by job type.

Use monthly volume as the control point. A few high-trust corporate or guide-client jobs can beat many small requests, but only if pricing stays above labor cost. If the broader business still carries $10,000 per month of fixed overhead, custom work needs enough margin to help cover that burden, not just generate busy work.

4

Forecaster Staffing Efficiency

Forecaster Staffing Efficiency

Staffing is the main capacity gate. Payroll starts at $500,000 in Year 1 and rises to $1,445M by Year 5, with roles like CEO, senior data scientist, full stack developer, lead meteorologist, and customer success manager. Owner income improves only when each hire adds enough forecast volume, contract work, or retention to cover salary and keep cash from tightening.

Owner-led work can save cash, but it leaves weak coverage and redundancy. If hiring starts before revenue density and quality control are ready, payroll can outrun subscriptions and cut the owner’s draw. One clean rule: don’t add headcount unless the added capacity is billable.

Track Hire Payback First

Measure revenue per staff hour, contract load, and renewal rate before adding headcount. A hire should improve coverage, response time, or enterprise delivery enough to pay for itself. Here, revenue density means revenue per staff hour or per client.

- Track revenue per forecaster.

- Test contract capacity by region.

- Watch quality-control pass rates.

- Delay hires until payback is clear.

If quality control slips, more staff just adds payroll without lifting take-home pay. Keep the team lean until repeatable review steps and clear handoffs are in place.

5

Insurance, Data, Software, and Field Cost Control

Insurance, Data, Software, and Field Cost Control

This driver covers $1,200 in monthly insurance, $800 in software, $2,000 in travel and field testing, plus 9% Year 1 cloud/data fees and 10% Year 1 payment costs. The model says gross margin improves from 810% in Year 1 to 860% in Year 5 as percentage costs fall, so more gross profit can flow to owner pay if service quality stays tight.

The cash warning is the real issue. Minimum cash drops to $543,000 in Month 8 before the model fully stabilizes, so early payouts can hurt the business even when revenue looks strong. In this setup, cost control protects margin without cutting safety standards, but reserves have to carry the business through the ramp.

Track the Cost Stack

Measure each cost bucket on its own: insurance, software, field travel, cloud/data, and payment fees. The inputs that matter are monthly fixed spend, percentage fees, and cash runway. If field testing rises faster than subscriber cash comes in, owner draw should wait.

- $1,200 insurance monthly

- $800 software monthly

- $2,000 field testing monthly

- 9% Year 1 cloud/data fees

- 10% Year 1 payment costs

- $543,000 cash low in Month 8

Cut waste, not verification. Trim unused software seats, compress travel routes, and watch payment fees, but keep the field checks that protect forecast quality and liability control. One clean rule: if a cost does not improve safety, accuracy, or collection speed, cap it hard.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income changes fast here because revenue mix, payroll growth, and marketing spend move together. Early profit can be thin, but the Year 5 case can support much stronger pay if staffing stays controlled.

| Scenario | Low CaseLaunch pay | Base CaseReserve pay | High CaseUpside pay |

|---|---|---|---|

| Launch model | The low case is a launch-year salary path with no dependable profit distributions. | The base case is a regional operator path with salary plus reserve-backed distributions. | The high case is a scale path with the strongest owner-pay capacity. |

| Typical setup | Year 1 reaches $1.026M revenue with about $500k payroll, $150k marketing, and a small loss, so the owner mainly takes modeled salary. | Year 2 reaches $2.456M revenue with about $690k payroll, $250k marketing, and $835k EBITDA, so owner pay starts after reserves. | Year 5 reaches $12.188M revenue with about $1.445M payroll, $700k marketing, and $7.783M EBITDA, but staffing and liability complexity are highest. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $145k salary onlyLow pay | Salary plus reservesBase pay | Highest pay capacityHigh pay |

| Best fit | Use this to stress-test a cash-tight opening year with no support for owner distributions. | Use this as the main planning case for a stable operating year after reserves are set. | Use this to test upside if enterprise licensing and staffing scale cleanly. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or required distributions.

Related Products

- Avalanche Forecasting Service Porter's Five Forces Analysis

- Avalanche Forecasting Service BCG Matrix

- Avalanche Forecasting Service Business Model Canvas

- What Are The Five KPIs For Avalanche Forecasting Service?

- Avalanche Forecasting Service Business Plan Template in Pre-Written Word

- How Increase Avalanche Forecasting Service Profits?

- What Are Operating Costs For Avalanche Forecasting Service?

- Avalanche Forecasting Service Startup Costs: $315k CAPEX, $543k Cash

- Avalanche Forecasting Service Financial Model Template in Excel

- How to Open an Avalanche Forecasting Service in 3 to 6 Months

- How Do You Write An Avalanche Forecasting Service Business Plan?

- Avalanche Forecasting Service Marketing Mix

- Avalanche Forecasting Service Marketing Plan

- Avalanche Forecasting Service Business Proposal

- Avalanche Forecasting Service PESTEL Analysis

- Avalanche Forecasting Service Pitch Deck Example Editable PPTX

- Avalanche Forecasting Service Business SWOT Analysis

- Avalanche Forecasting Service Value Proposition Canvas

Frequently Asked Questions

The supplied model includes a $145,000 CEO salary before taxes Year 1 EBITDA is -$16,000 on $1026M revenue, so profit distributions are not supported by operations alone By Year 2, EBITDA reaches $835,000 on $2456M revenue, giving room for reserves, reinvestment, debt service, or added owner take-home