Owner income$0-$5.4k

Owner income$0-$5.4kHow Much Does a Baby Store Owner Make? $0–$65k Early

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0-$5.4k  Net margin-106% to 67%

Net margin-106% to 67% Revenue for target pay≈$256k

Revenue for target pay≈$256k Business difficultyHard

Business difficultyHard

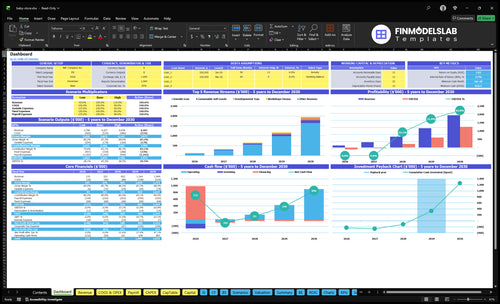

A baby store owner can plan for little or no profit distribution in the first two years in this model, because EBITDA is -$117k in Year 1 and -$33k in Year 2 If the owner also works as the store manager, the model includes a $65,000 annual manager role, but that is labor pay, not profit By Year 3, the store reaches $216k EBITDA, and mature-year upside rises to $604k in Year 4 and $1244M in Year 5 before taxes, debt service, capex reinvestment, and inventory reserves These are researched planning assumptions, not guaranteed baby store owner salary

Owner income$0-$5.4kNet margin-106% to 67%Revenue for target pay≈$256kBusiness difficultyHardWant to test your baby store owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it should be read beside the model's month 25 breakeven, $610k minimum cash, and month 43 payback.

Want to check owner income in the Baby Store financial model?

The Baby Store Financial Model Template shows revenue, margin, costs, reserves, and owner take-home. Open the model to see the planning logic.

Owner-income model highlights

- Owner pay: salary, distributions

- EBITDA: -$117k to $1.244M

- Lease $4,500; overhead $5,650

- Inventory $30k; build-out $136k

How much revenue does a baby store need to pay the owner?

If you want to pay the owner, start with the payout target, not a generic sales goal. In the Baby Store model, the business needs about $256k in annual revenue to cover fixed overhead and modeled payroll, and about $337k if you add a $65k owner draw. That estimate still excludes personal taxes, debt service, and inventory buffer growth, so lower rent or the owner doing more of the management work can bring the hurdle down.

Pay target math

- Start with owner pay first.

- $256k covers overhead and payroll.

- $337k adds a $65k draw.

- Use revenue to fund the pay plan.

What this leaves out

- Personal taxes are not included.

- Debt service is not included.

- Inventory buffer expansion is not included.

- Lower rent reduces the revenue floor.

How much can a baby store owner pay themselves?

A Baby Store owner can pay themselves $65,000 per year, or about $5,417 per month, if they personally fill the store manager role; profit distributions should be $0 in Year 1 and Year 2 because EBITDA is negative. By Year 3, the model shows $216,000 EBITDA before taxes, debt service, capex, and reserves, so owner draws depend on cash left after those needs; stronger repeat customers and ecommerce can increase draw capacity, as tracked in What Is The Current Customer Satisfaction Level For Baby Store?.

Owner Pay Range

- Pay salary first: $65,000/year

- Monthly salary equals about $5,417

- Year 1 distributions: $0

- Year 2 distributions: $0

Profit Draw Rules

- Year 3 EBITDA: $216,000

- Fund taxes before owner draws

- Cover debt, capex, and reserves

- Use repeat sales to raise draws

What affects baby store profit margin?

Baby Store profit margin is mostly driven by product mix, markdowns, shrink, rent, payroll, and inventory turnover; the model shifts from 35% durable gear in Year 1 to 25% in Year 5, while soft goods rise from 30% to 40%. For startup math, see What Is The Estimated Cost To Open And Launch Your Baby Store Business?—and remember that margin percentages are planning assumptions, not cash in the bank.

Margin drivers

- 35% to 25% durable gear mix shift

- 30% to 40% soft goods mix shift

- 120% to 100% wholesale product cost

- Markdowns, shrink, rent, payroll, turnover

Cost pressure

- 30% to 20% instructor fees

- 40% to 30% marketing

- 10% processing stays flat

- Slow size runs can drain cash fast

Want to see what drives baby store owner income?

1

$173-$202Sales

Bigger baskets, plus conversion rising from 4.5% to 10.5%, lift monthly sales and help reach Month 25 breakeven.

2

88%-90%Gross Margin

A mix tilt toward softer goods and a 12% to 10% wholesale cost line keeps more cash from each sale.

3

30%-45%Repeat Buyers

Repeat customers, registries, and ecommerce orders add revenue with less new-traffic spend.

4

$65KPayroll

The manager salary anchors payroll, and added staffing can swallow owner pay fast.

5

$5.65KOverhead

Lease, utilities, insurance, software, and cleaning run every month and delay breakeven.

6

10%-12%Inventory Turns

Faster sell-through protects the wholesale cost line and keeps markdowns from eating cash.

Baby Store Core Six Income Drivers

Monthly Sales and Average Order Value

Monthly Sales and Order Value

Monthly sales and average order value set the revenue base before margin and fixed costs decide owner pay. In this model, daily visitors move from 60 to 120 on Year 1 days and up to 240 on Year 5 Saturdays, while conversion is modeled from 45% to 105% and units per order from 12 to 16.

Basket size matters because durable gear runs $350 to $390, soft goods $35 to $39, toys $28 to $32, and classes $45 to $53. Traffic without conversion does not pay the owner. Higher order density helps absorb rent and payroll, but weak baskets can still leave cash tight even when foot traffic looks strong.

Track Conversion, Not Just Traffic

Measure visitors, conversion, units per order, and average basket every day. If visitors rise but orders do not, sales quality is slipping and fixed costs stay heavy. Here’s the quick math: more orders at the same basket size spread rent and labor across more revenue, which improves the owner’s take-home after gross margin.

Watch category mix by ticket size. Durable gear lifts revenue fast, while soft goods, toys, and classes can raise visit frequency and repeat buying. The risk is simple: high traffic with low conversion adds cost but not profit, so the owner should forecast sales from actual order count, not just store visits.

1

Product Mix and Gross Margin

Product Mix and Gross Margin

If the store shifts sales toward higher-repeat soft goods, more of each dollar turns into gross profit. In this model, durable gear falls from 35% of sales mix to 25%, consumable soft goods rise from 30% to 40%, developmental toys stay at 25%, and workshops stay at 10%.

That matters for owner pay because gross margin after wholesale product cost and instructor fees is modeled at 850% in Year 1 and 880% in Year 5. Gear can lift ticket size, but soft goods can bring repeat trips; price cuts and markdowns can wipe out the expected margin and shrink draw capacity.

Track Mix by Margin, Not Just Sales

Measure sales mix, average order value, markdown dollars, and gross profit by category each month. Use the mix to see whether gear is just adding revenue or actually improving take-home income.

- Track mix by category dollars.

- Watch wholesale cost and fees.

- Flag markdowns fast.

- Test soft-goods repeat buys.

If gear or toys need discounting to move, the mix may still look busy while profit falls. Keep full-price sell-through on strong items, and protect soft-goods margins where repeat trips can support steadier cash flow.

2

Inventory Costs and Markdown Discipline

Inventory Cash Trap

Inventory is cash sitting on a shelf. With $30k in starting stock and breakeven at Month 25, overbuying seasonal items or slow-moving sizes can trap cash, trigger clearance sales, and cut the owner’s draw even if accounting profit still looks fine.

Returns, shrink, and markdowns hit hard in baby retail. If owner draws happen before replenishment, stockouts can follow, and that means lost sales plus weaker repeat trips.

Track Turns and Markdowns

Use sell-through (how fast stock sells), markdown rate, returns, shrink, and reorder timing to estimate the cash hit. The model’s $610k minimum cash need leaves little room for slow stock, so faster turnover matters more than holding depth on weak items.

- Watch sell-through by size.

- Mark down before stock ages.

- Hold draws until reorders land.

- Cut buys on weak styles.

If wholesale product cost runs from 120% to 100% of sales, cash gets tight fast. The owner should use weekly inventory counts and a clear clearance rule so excess stock does not steal working capital or force last-minute discounting.

3

Rent and Overhead

Fixed Rent and Overhead

This is the bill stack the store pays before owner pay: $4,500 lease, $400 utilities, $200 insurance, $150 ecommerce, $100 software, and $300 maintenance and cleaning. Total fixed overhead is $5,650/month, or $67,800/year before wages. That sets the monthly sales floor. If traffic softens, the lease still comes due.

A better location can lift walk-in traffic, but only if sales cover the fixed base fast enough. Using the model’s stated sensitivity, every extra $1,000 in fixed cost needs about $1,250 in sales to keep owner income flat. One clean rule: high rent is fine only when it buys enough order volume.

Keep the Monthly Floor Low

Track monthly rent, utilities, and software together, then compare them with gross profit and cash on hand. The key inputs are lease size, traffic, conversion, and average order value, because those decide whether fixed overhead is covered before owner draw. Here’s the quick math: $5,650 of fixed overhead has to be earned back every month before wages and owner pay.

- Watch sales per square foot.

- Stress-test slow months early.

- Negotiate lease terms before signing.

4

Payroll and Owner Role

Payroll and Owner Pay

Payroll decides whether profit is real owner income or just unpaid labor. In Year 1, the model includes 1.0 manager FTE at $65k, 1.5 sales associate FTE at $32k each, and 0.5 ecommerce coordinator FTE at $48k. That is about $137k in annual base payroll before the $25k part-time workshop instructor role.

If the owner runs the store full-time without pay, reported profit will overstate sustainable income. Weekend coverage and ecommerce support can lift sales, but they also push breakeven higher. The real question is simple: does the added labor create enough gross profit to cover the wage bill and still leave room for owner pay?

Track Labor Against Sales

Measure labor in two buckets: fixed management pay and variable coverage. Track sales per labor dollar, weekend revenue lift, ecommerce orders per coordinator hour, and whether the $25k workshop role brings in paid traffic. If added shifts raise orders but not margin, the store may look profitable while the owner still cannot draw cash.

- Count FTE by role

- Track pay by role

- Test weekend sales lift

- Set owner draw target

Owner-filled management can preserve cash early, but the model should still price that work. One clean rule: unpaid owner labor is not free. If you do not charge the business for your time, you are reading profit, not true take-home income.

5

Repeat Customers, Registries, and Ecommerce

Repeat Buyers and Registry Demand

When parents come back for gifts, diapers, clothes, and gear, the store earns more from each customer it already paid to attract. Here, repeat customers rise from 30% of new customers in Year 1 to 45% in Year 5, and lifetime climbs from 6 to 10 months at 1 order per month. That means stronger revenue per acquired customer and less dependence on walk-in traffic.

The input set is simple: new customers, repeat rate, months kept, orders per month, and average order value. Registry-style gift demand, pickup orders, replenishment trips, and local trust all help keep that flow going. The risk is clear: if ecommerce volume stays thin, the $48k coordinator plus $150 monthly platform fee can eat profit before sales catch up.

Measure Repeat Revenue, Not Just Traffic

Track repeat orders by cohort, not just total sales. A clean test is: how many first-time buyers place a second order within 6 months, and how many registry buyers return after the event? Use those counts to forecast whether ecommerce labor can pay for itself before adding hours or promotions. If repeat share lags, owner pay gets squeezed fast.

- Track repeat rate by month

- Watch 6 to 10 month lifetime

- Separate gifts, pickup, replenishment

- Compare orders to $48k labor

- Keep platform cost at $150 monthly

6

Compare lean, base, and strong baby store owner income scenarios

Owner income scenarios

Owner pay shifts with traffic, conversion, staffing, and the cash needed to survive the Month 25 breakeven point and $610k minimum cash trough.

| Scenario | Low CaseCash burn | Base CaseBreakeven build | High CaseUpside draw |

|---|---|---|---|

| Launch model | This is the launch-year case, where negative EBITDA leaves no safe owner draw. | This is the modeled mid-case, where owner pay starts to open up but still depends on reserves. | This is the stronger earnings path, where scale and cash flow support a larger owner draw. |

| Typical setup | Year 1 traffic and a 4.5% visitor-to-buyer conversion support modest volume, but about $125k payroll and $5,650 monthly fixed overhead keep cash tight. | Year 3 traffic, a 7.5% conversion rate, 2.5 retail FTE, 1.0 e-commerce FTE, and 0.5 workshop instructor FTE lift EBITDA to $216k. | Year 5 traffic, a 10.5% conversion rate, 3.5 retail FTE, 1.0 e-commerce FTE, and 1.0 workshop instructor FTE push EBITDA to $1.244M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No safe drawCash burn | Reserve-limited drawBreakeven build | Higher draw capacityUpside draw |

| Best fit | Use this to stress test launch-year cash needs and the weakest income path. | Use this as the main planning case for owner pay while the business clears breakeven and rebuilds cash. | Use this to test upside owner pay after taxes, debt service, inventory, and reinvestment. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Baby Store Porter's Five Forces Analysis

- Baby Store BCG Matrix

- Baby Store Business Model Canvas

- Tracking 7 Core Financial KPIs for Your Baby Store

- Baby Store Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Baby Store Profitability

- How Much Does It Cost To Run A Baby Store Monthly?

- Baby Store Startup Costs: $106K Fixed Assets Plus $30K Inventory

- Baby Store Financial Model Template in Excel

- How to Open a Baby Store in 3 to 6 Months With First-Sales Readiness

- How to Write a Baby Store Business Plan in 7 Steps

- Baby Store Marketing Mix

- Baby Store Marketing Plan

- Baby Store Business Proposal

- Baby Store PESTEL Analysis

- Baby Store Pitch Deck Example Editable PPTX

- Baby Store Business SWOT Analysis

- Baby Store Value Proposition Canvas

Frequently Asked Questions

In this model, profit distributions are weak early because EBITDA is -$117k in Year 1 and -$33k in Year 2 If the owner fills the manager role, the model includes $65k of labor pay By Year 3, EBITDA reaches $216k before taxes, debt service, reserves, and reinvestment