Bank Drive-Thru Construction Startup Costs: $421K Cash Need

Key Takeaways

- Licensing and bonding prove bid capacity to lenders.

- Vehicle and tool spend belongs in startup CAPEX.

- Design systems cut bid errors and billing issues.

- Working capital covers payroll before customer cash arrives.

Estimate Startup Costs with Calculator

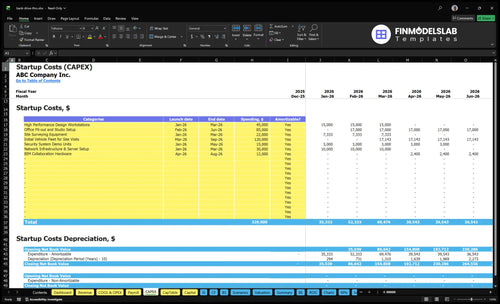

Startup CAPEX Calculator

Estimates capitalized startup assets only for a bank drive-thru construction business; base CAPEX sums to 329000 before contingency.

What's excluded This calculator includes only capitalized startup assets. It excludes inventory, payroll runway, deposits, debt service, working capital, bid costs, client project materials, insurance premiums, bonding deposits, operating losses, and other non-CAPEX funding needs.

What does this Bank Drive-Thru Construction screenshot show?

The financial model tab shows CAPEX. Review the financial model; it's planning only. Breakeven is Month 8; payback 21 months.

Key financial model highlights

- $329k startup CAPEX categories

- Launch timing; revenue ramp

- Depreciation, amortization

- $421k cash need, Month 8

- $1.508M revenue; -$49k EBITDA

- Debt service, retainage, payroll runway

How much money do you need to start a bank drive-thru construction company?

You need $421,000 minimum cash to start a Bank Drive-Thru Construction company, made up of $329,000 CAPEX, pre-opening costs, and working capital through Month 8; see the related owner economics in How Much Does Drive-Thru Construction Owner Make?. This funding is for the contractor launch, not the bank client’s drive-thru construction budget.

Startup Cash Need

- $329,000 CAPEX

- $421,000 minimum cash by Month 8

- $22,150 monthly fixed expenses

- Working capital covers early payroll pressure

Payback Math

- $1.508 million Year 1 revenue

- -$49,000 Year 1 EBITDA

- $635,000 Year 1 salaries

- Breakeven Month 8; payback 21 months

What hidden costs can strain working capital for bank drive-thru construction contractors?

Bank Drive-Thru Construction can strain working capital fast because bid prep, engineering reviews, permit support, travel, fuel, inspections, deposits, and retainage all hit before full payment. See How Increase Bank Drive-Thru Construction Profits? for why specialty work needs tighter cash control. The Month 8 minimum cash need is $421,000, so even reimbursable client costs can still leave a timing gap.

In Year 1, project site travel and logistics can run at 50% of revenue, subcontractor labor pass-through at 120%, and materials at 80%, while payroll, punch-list work, and insurance audit adjustments still come due before collections.

Cash drains

- Bid prep and engineering reviews

- Permit support and inspections

- Travel and fuel costs

- Subcontractor and material deposits

Timing gaps

- Payroll before collections

- Punch-list work at the end

- Retainage delays cash

- Insurance audits can adjust costs

How do you fund a bank drive-thru construction startup?

Fund Bank Drive-Thru Construction with a lender-ready stack built around $329,000 in CAPEX, startup costs, working capital, and debt service. Here’s the quick math: Year 1 revenue is $1.508 million, EBITDA is -$49,000, breakeven lands in Month 8, and payback is 21 months with 761% IRR and 811% ROE. Keep the cash request tied to vehicles, design systems, insurance, marketing, and mobilization, not client construction budgets.

What the lender funds

- $329,000 CAPEX base

- Startup expenses and working capital

- Debt service runway

- Vehicles and mobilization

How the cash moves

- Bill by project milestones

- Use retainage in the model

- Match revenue timing to payroll

- Plan for Month 8 breakeven

Calculate Fuding Needs

Startup cost summary

This table shows startup CAPEX and excluded launch cash needs for a bank drive-thru construction business.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Office Fit-out and Studio Setup | $85,000 | Build-out scope and workspace finish level | Yes |

| Initial Vehicle Fleet for Site Visits | $120,000 | Fleet count and vehicle spec for site work | Yes |

| Design Workstations and Surveying Equipment | $67,000 | Workstation count and field equipment quality | Yes |

| Project Management and Collaboration Systems | $42,000 | Server, BIM, and collaboration setup depth | Yes |

| Security System Demo Units | $15,000 | Demo unit count and security package scope | Yes |

| Operating Reserve | $421,000 | Month 8 operating cash and payroll runway | No |

Bank Drive-Thru Construction Core Five Startup Costs

Licensing and Bonding Startup Expense

License first

If you're building bank drive-thru facilities, licensing and bonding are gatekeepers, not paperwork. Separate state contractor licensing, business formation, and local registrations from project permits for one site. Bid, performance, and payment bonds can decide whether you can bid, win, and keep cash moving on commercial bank work.

Estimate the gate

This cost covers license class, design-build scope, and surety setup, not field permits. Estimate it from state class, project size, owner requirements, balance sheet strength, and subcontractor bond needs. One line item can open or close bank work, because sureties judge capacity, not just fees.

- Class and scope drive approval.

- Bigger projects raise bond tests.

- Weak balance sheets slow underwriting.

Bonding and cash

Treat bonding readiness as a working-capital issue. If you need $421,000 in Month 8 and carry $22,150 of fixed monthly expense, a surety will look hard at liquidity, payables, and how fast you fund payroll before collections. Strong bonding helps lender confidence; weak bonding can trap growth.

Keep it separate

Do not mix this with a single bank site permit budget. Licensing, registrations, and bonds are pre-project startup costs; permits sit with each job. For bank clients, tight compliance setup, clean subcontractor bond checks, and proof of coverage can be the difference between a signed contract and a stalled award.

Vehicles, Tools, and Jobsite Equipment Startup Expense

CAPEX Starter Kit

If you need crews on the road and on site, treat durable gear as CAPEX, not overhead. Start with $120,000 for the vehicle fleet and $22,000 for site surveying equipment, then add trailers, compact tools, concrete tools, lane layout tools, ladders, barricades, PPE, and jobsite storage only if the scope and geography require it.

Budget Inputs

Here’s the quick math: count units, get quotes, then price by crew size and service radius. One truck-heavy crew needs less than a multi-site team. Add in surveying gear, trailers, and field tools only when they are used every week. One line matters most: buy for utilization, not for pride.

- Use units × unit price

- Get dealer and supplier quotes

- Match gear to crew count

Keep It Lean

Lease versus buy should follow project volume, not habit. If subcontractors handle most field work, keep owned equipment light. Include $15,000 demo units only when they support sales, testing, or integration demos. Do not count client-owned drive-thru systems as startup assets unless the contractor stocks them.

- Lease when utilization is uneven

- Skip idle demo gear

- Exclude client-owned systems

Scope Controls

Refine this line item by crew size, geographic coverage, and subcontractor-led scope. A tight territory and heavy subcontracting can cut owned tools fast, while wider travel and self-performed work push up fleet, storage, and field gear. Keep the asset list tied to actual project delivery, not to the full build in theory.

Design, Estimating, and Project Management Systems Startup Expense

Design Stack

Your estimating and project controls need enough power to price lanes, canopies, electrical scopes, security coordination, technology integration, schedules, change orders, and job costing without file lag. Budget $45,000 for design workstations, $30,000 for network and server setup, $12,000 for BIM hardware, and $1,800 per month for CAD and BIM subscriptions. Clean files mean cleaner bids.

Cost Build

Estimate this with counts and quotes: workstation count × unit price, server and network quotes, BIM device count × cost, and subscription months. At $1,800 monthly, software totals $21,600 per year. Capitalize hardware and setup; expense recurring software. Keep this separate from permits and jobsite tools so startup cash stays readable.

Run Lean

Use estimating templates, takeoff tools, project management software, CRM, and cost-code setup from day one. Standard templates cut misses on scope-heavy bank jobs, and cost codes make change orders and billing cleaner. The main waste is poor setup, not the software bill, so assign one owner and lock file rules before the first bid.

Bid Quality

Better systems pay off in fewer bid errors and faster billing because the team can price scope changes, track field updates, and post job costs in one place. For this business, the stack is not overhead fluff; it is the control layer that protects margin on specialized drive-through work.

Insurance and Risk Management Startup Expense

What it covers

Keep insurance separate from bonding and CAPEX. For drive-thru bank work, the base package usually includes general liability, workers’ compensation, commercial auto, umbrella coverage, and professional liability at $3,200 per month if you design plans. Builder’s risk is coordinated for site damage during construction, not booked as equipment.

How to estimate

Estimate this cost from policy quotes, project scope, and coverage limits. Use months of coverage, payroll, subcontractor volume, revenue, and vehicle count to size the premium. Commercial auto matters here because vehicle CAPEX is $120,000. Bank clients may require proof of coverage before contract award, so insurance can affect bid eligibility fast.

- Get quotes by coverage type

- Match limits to contracts

- Separate site damage coverage

How to control it

Lower cost by right-sizing limits, keeping clean loss history, and reviewing auto and workers’ comp exposure before renewal. Don’t bundle bonds into insurance math. The big risk is audit drift: carriers can adjust premiums after payroll, subcontractor volume, and revenue change, so update your forecast every quarter. Simple rule: if headcount moves, reprice coverage.

Banking contract gate

For this business, insurance is a contract gate, not a back-office fee. If you offer design services, professional liability supports scope risk, while general liability and workers’ compensation cover jobsite exposure. Lenders and bank clients often want current certificates before kickoff, so missing coverage can delay mobilization even when the project is won.

Working Capital and Mobilization Startup Expense

Cash Floor

Working capital is required funding, not a cushion. For this model, the minimum cash need is $421,000 in Month 8 to cover payroll before collections, subcontractor and material deposits, mobilization, inspections, travel, fuel, retainage, the money owners hold back until closeout, and punch-list work.

What It Funds

Here’s the quick math: Year 1 salaries of $635,000 run about $52,917 a month, plus $22,150 in fixed monthly expenses and $120,000 in marketing, or $10,000 a month. That is roughly $85,067 a month before project cash needs. Add subcontractor labor at 120%, materials at 80%, travel and logistics at 50%, and sales commissions at 40%.

How To Protect It

Keep a separate cash reserve and invoice fast. The big mistake is assuming progress billing will fund mobilization. It often won’t. Stage starts only when deposits are in hand, track retainage by job, and tie hiring to signed work, not pipeline. One clean rule: if cash is not collected, it is not available.

Bonding And Cash

Surety underwriters and lenders look at the same thing: can the business absorb payroll, deposits, and closeout costs without strain? A strong working-capital reserve supports bid, performance, and payment bond capacity, and it lowers the risk that retainage and punch-list work will trap cash at the wrong time.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Cash needs rise as the model adds owned assets, payroll, and in-house design work. Lean depends more on subcontractors, while Full Launch needs more equipment, vehicles, and control.

| Scenario | Lean LaunchLowest cash risk | Base LaunchBalanced launch | Full LaunchHighest control |

|---|---|---|---|

| Launch model | Uses more subcontractor capacity and fewer owned assets. | Uses a specialty contractor core with some in-house delivery. | Builds in-house design depth and broader delivery control. |

| Typical setup | Fits a smaller geography and a lighter payroll runway. | Balances design support, project management, and retrofit work. | Adds more vehicles, stronger bonding capacity, and a larger payroll runway. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $329,000 - $421,000Lower cash need | Mid-six-figure bandBalanced funding | High-six-figure bandHighest control |

| Best fit | Best when project size is smaller and design stays outside the core team. | Best when bank clients want a steady build partner with some in-house coordination. | Best when larger bank jobs need in-house design services and wider geographic reach. |

Planning note: These ranges are researched planning assumptions from the model, not exact quotes or fixed bids.

Related Products

- Bank Drive-Thru Construction Porter's Five Forces Analysis

- Bank Drive-Thru Construction BCG Matrix

- Bank Drive-Thru Construction Business Model Canvas

- What Are The 5 KPIs For Bank Drive-Thru Construction?

- Bank Drive-Thru Construction Business Plan Template in Pre-Written Word

- How Increase Bank Drive-Thru Construction Profits?

- What Are The Operating Costs Of Bank Drive-Thru Construction?

- Bank Drive-Thru Construction Financial Model Template in Excel

- How Much Bank Drive-Thru Construction Owners Can Make by Year 5

- Start a Bank Drive-Thru Construction Company in 90 to 180 Days

- How Do I Write A Bank Drive-Thru Construction Business Plan?

- Bank Drive-Thru Construction Marketing Mix

- Bank Drive-Thru Construction Marketing Plan

- Bank Drive-Thru Construction Business Proposal

- Bank Drive-Thru Construction PESTEL Analysis

- Bank Drive-Thru Construction Pitch Deck Example Editable PPTX

- Bank Drive-Thru Construction Business SWOT Analysis

- Bank Drive-Thru Construction Value Proposition Canvas

Frequently Asked Questions

The researched model shows a $421,000 minimum cash need by Month 8 That reserve sits on top of normal discipline around billing, collections, and retainage The pressure comes from $329,000 of CAPEX, $635,000 of Year 1 salaries, and $22,150 of monthly fixed overhead before the company reaches breakeven