Owner income$95K

Owner income$95KHow Much Does A Bartending School Owner Make At $1138M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$95K  Net margin45%-79%

Net margin45%-79% Revenue for target pay$210K

Revenue for target pay$210K Business difficultyMedium

Business difficultyMedium

You’re trying to see whether a bartending school can pay you, not just keep the lights on This researched US model uses tuition, occupancy, staffing, lease costs, marketing, and reserves, with $1138M first-year revenue, $515K first-year EBITDA, and a $95K School Director salary as planning inputs, not guaranteed pay

Owner income$95KNet margin45%-79%Revenue for target pay$210KBusiness difficultyMediumWant to test your bartending school owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Bartending School model?

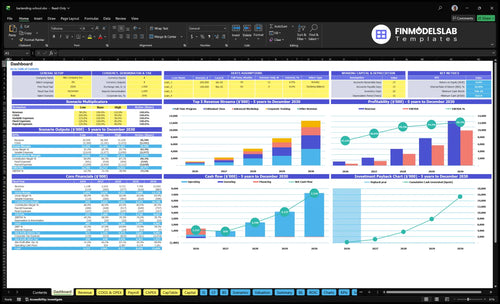

The screenshot shows a planning model, not a promise: dashboard, tuition assumptions, enrollment and occupancy, class schedule, payroll, fixed costs, variable costs, capex, marketing, scenarios, cash flow, and owner income. Open the Bartending School Financial Model Template to test local pricing and class fill rates.

Owner-income model highlights

- Owner take-home modeled

- Revenue: $1,138M to $12,620M

- EBITDA: $515K to $9,927M

- Occupancy: 45% to 90%

- Cash floor, Month 2: $824K

- Payback in 8 months

How does an owner-operated bartending school scale?

Bartending School scales best when the owner keeps teaching or directing classes early, because the $95K School Director cost stays inside owner pay instead of becoming a new hire. Here’s the tradeoff: growth needs more instructors, admissions capacity, and placement support, with payroll rising from 1 lead instructor at $75K to 3 FTEs by Year 5, while occupancy moves from 45% to 90% and billable days from 22 to 26. That works only if demand fills more cohorts, private lessons, and corporate training.

Owner-led cash flow

- Keep $95K in owner pay.

- Use one lead instructor at $75K.

- Protect early cash with direct teaching.

- Fill cohorts before adding staff.

Scale pressure points

- Grow to 3 FTEs by Year 5.

- Raise occupancy from 45% to 90%.

- Increase billable days from 22 to 26.

- Balance quality control with labor leverage.

How much does a bartending school owner take home?

A Bartending School owner’s modeled take-home starts at $95K/year if they also act as School Director, or about $7,917/month; see How To Launch A Bartending School? for the setup path. Profit distributions are separate: modeled EBITDA is $515K in Year 1 and $9927M in Year 5 before taxes, debt service, depreciation, reserves, and reinvestment.

Owner Pay

- $95K modeled School Director salary

- $7,917 monthly salary equivalent

- Applies only if owner fills role

- Distributions are not guaranteed salary

Profit Limits

- $515K Year 1 modeled EBITDA

- $9927M Year 5 modeled EBITDA

- Retain cash for growth and reserves

- Costs include payroll, lease, supplies, marketing

What profit margin can a bartending school make?

A Bartending School can post a very high model margin, with EBITDA margin rising from 453% in Year 1 to 787% in Year 5. See How Increase Bartending School Profits? for the main profit levers. The key pressure point is seat fill, because Year 1 variable training costs are 200% of revenue and fixed lease plus operating costs run $89K a month.

Margin drivers

- Occupancy lifts margin.

- Pricing improves Year 5 economics.

- Billable days matter most.

- Fill seats before hiring more instructors.

Cost stack

- Year 1 variable costs hit 200%.

- 65% is beverage supplies.

- 35% is course materials.

- 80% is digital marketing, plus 20% placement commissions.

Want the six drivers of bartending school income?

1

$1.1M-$12.6MPaid Enrollment

More paid students push revenue from Year 1 to Year 5, so owner take-home rises fastest when admissions keeps seats full.

2

$2.8K-$5.5KTuition Mix

Shifting mix toward full-time and corporate classes lifts revenue per student and adds margin faster than volume alone.

3

45%-90%Class Utilization

Higher occupancy turns empty seats into cash, and every point of fill matters in a fixed-room school.

4

$250K-$582KInstructor Leverage

Payroll grows as the school scales, so keeping student growth ahead of instructor staffing protects EBITDA.

5

8.0%-5.5%Student Acquisition

Lower lead cost keeps more of each tuition dollar when digital marketing and placement spend take a bigger share.

6

$8.9K/moFacility Control

Tight control of lease, utilities, and supplies stops fixed overhead from eating profit when enrollment is soft.

Bartending School Core Six Income Drivers

Paid Student Enrollment Volume

Paid Student Enrollment Volume

Paid seats, not inquiries, drive tuition cash. The key inputs are monthly paid students, occupancy rate, students per class, refunds, and completed cohorts. If occupancy moves from 45% in Year 1 to 90% in Year 5, tuition revenue rises faster than fixed lease and admin costs, so EBITDA improves once overhead is covered.

The risk is weak lead conversion. A class only adds income if the seat is paid and the student finishes. Track each program separately: full-time seats, advanced workshop seats, corporate training buyers, and enthusiast attendees.

- Paid seats by month

- Net refunds after dropouts

- Occupancy rate by cohort

- Completed cohorts by program

Track Fill, Then Cash

Use a simple formula: paid seats ÷ total seats. That tells you real demand, while inquiries and followers do not. Watch it by cohort and month so you can see which classes are filling, which are stalling, and where tuition cash is actually coming from.

If paid seats lag, fixed costs still run. If paid seats rise, the same lease, software, and admin base gets spread over more tuition dollars, which lifts owner pay and makes the school easier to run from cash flow.

1

Tuition Pricing And Program Mix

Tuition Mix and Pricing

Average tuition matters here because higher-value programs raise revenue per student without a matching jump in delivery cost. The price ladder is wide: $350 to $450 for an enthusiast class, $1,200 to $1,650 for an advanced workshop, $2,800 to $3,500 for the full-time program, and $4,500 to $5,500 for corporate training. One $5,500 corporate sale can equal about 12 to 16 enthusiast seats.

The key inputs are program mix, discount rate, private training revenue, and completion outcomes. If the school sells more full-time and corporate seats, gross margin usually improves because fixed costs get spread over higher tuition. The risk is simple: pricing above local demand or job proof can slow enrollments and push owner cash flow down fast.

Track Mix Before You Raise Price

Watch average tuition per paid student by program, not just total enrollments. Here’s the quick math: if discounting rises, net tuition falls even when seat count holds. Track how many students buy each offer, how many finish, and how many lead to job placements, since completion outcomes support price power and repeat demand.

Test price changes in small steps. Raise the highest-value offers first, then compare revenue per seat, refund rate, and filled capacity against the prior month. If a higher price lowers conversions but not completions, the business may still earn more; if it cuts fill rate, owner pay drops because fixed overhead stays the same.

2

Class Utilization And Schedule Efficiency

Class Utilization

Class utilization is how many seats and billable class days you actually fill. For a bartending school, the win is simple: a cohort at 90% occupancy earns far more than one at 45%, while the same rent and admin cost stay in place. Moving billable days from 22 to 26 a month raises revenue capacity and can lift EBITDA by spreading fixed costs over more paid students.

Track seat fill rate, class capacity, evening and weekend use, billable days, and instructor hours per cohort. The risk is adding schedules before demand, which creates empty seats and weak cash flow. Full classes improve owner pay faster than more rooms or more cohorts, because profit rises when fixed costs get absorbed, not when calendars look busy.

Fill the calendar, not the room

Stack workshops around full-time programs, and book corporate training in off-peak hours. That lets you use the same space and instructor time more often without adding new fixed cost. Measure each cohort by paid seats, not inquiries, and compare weekday versus evening and weekend fill.

Set a minimum fill target before opening another class. If a time slot stays weak, cut it or combine it. The best schedule is the one that turns more billable days into paid seats and keeps instructor hours per cohort productive.

- Track seat fill by cohort

- Split weekday and weekend demand

- Cut low-fill time slots fast

- Use off-peak corporate training

3

Instructor Staffing Leverage

Instructor Staffing Leverage

When the owner teaches early cohorts, cash stays tighter because there’s no extra salary burn. Scaling changes that fast: staffing includes a Lead Mixology Instructor at $75K, a School Director at $95K, and headcount growth from 10 FTE in Year 1 to 30 FTE in Year 5. If paid seats do not rise ahead of payroll, owner take-home income gets squeezed.

Track Payback Before You Hire

Measure instructor cost per paid student, utilization, class ratings, and repeat enrollment by cohort. The quick math is plain: base leadership pay alone is $170K a year before contract help. Keep teaching owner-led until seat fill holds, then add staff only when enrollment demand stays ahead of payroll. Quality drift is the main risk once contract or full-time instructors start carrying classes.

4

Facility, Insurance, Licensing, And Supplies

Facility Cost Pressure

$89K a month in fixed operating costs sets the breakeven floor before tuition even starts to matter. The $65K lease does most of the damage, and utilities, insurance, software, cleaning, and memberships keep cash burn high when classes are not full.

The $2.205M buildout for the simulated bar, glassware, POS training systems, furniture, AV, signage, and refrigeration only works if seats fill fast. If utilization stays weak, 65% supply costs and 35% materials can squeeze owner pay; if those ratios improve to 50% and 20%, more tuition turns into profit.

Track Fixed Cost Per Seat

Measure paid seats, not leads, against monthly facility cost. Here’s the quick math: every filled class spreads the $89K load across more tuition dollars, which lifts cash flow and makes an owner draw more realistic. Full classes pay the lease; empty ones don’t.

- Track occupancy by cohort.

- Watch supply cost per student.

- Delay extra buildout until demand proves out.

- Review breakage and replacement weekly.

Keep the room lean until utilization is stable. If the school buys too much equipment, décor, or training stock too early, the payback slows and fixed cost pressure stays high even when the brand looks polished.

5

Marketing Cost And Lead Conversion

Paid Enrollment Conversion

This driver is not about leads; it is about turning paid enrollments. In Year 1, 80% of revenue depends on digital marketing and lead generation, then that falls to 55% by Year 5 as referrals and local search do more work. Owner income improves when cost per enrollment stays low, lead-to-enrollment rate rises, and paid traffic stops buying low-intent leads.

The key inputs are paid leads, tuition collected, enrollment conversion, and placement commissions, which stay at 20%. Here’s the quick math: if more leads are low intent, you pay more to fill the same seat, so contribution margin shrinks and cash gets tight. Strong employer partnerships and placement reputation matter because they support conversions and future referrals.

Track Enrollment, Not Clicks

Measure cost per enrollment by channel, not just cost per lead. Split digital spend from referrals, local search, and employer referrals, then track which source produces a paid seat at the best margin. If one channel fills seats but brings weak-fit students, it can lift revenue and still hurt owner pay through refunds, lower placement quality, and more support time.

Watch these weekly:

- Lead-to-enrollment rate

- Cost per paid seat

- Local search visibility

- Referral share

- Employer partnership count

- Placement reputation risk

6

Compare lean, base, and high bartending school income cases

Owner income scenarios

Owner income rises as occupancy, billable days, and pricing improve. Reserves, taxes, debt service, and reinvestment still cut what the owner can take home.

| Scenario | Low CaseRamp | Base CaseEfficient | High CaseMature |

|---|---|---|---|

| Launch model | Low Case shows the launch ramp when income is still building. | Base Case shows the modeled steady path once demand and staffing are in balance. | High Case shows the stronger earnings path when the school runs near full capacity. |

| Typical setup | Year 1 ramp with 45.0% occupancy, 22 billable days, $1.138M revenue, $515k EBITDA, and $250k payroll. | Year 3 steady state with 75.0% occupancy, 24 billable days, $4.712M revenue, $3.311M EBITDA, and $422k payroll. | Year 5 mature run rate with 90.0% occupancy, 26 billable days, $12.620M revenue, $9.927M EBITDA, and $582k payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $265kRamp case | $2.9MEfficient case | $9.3MMature case |

| Best fit | Use this to test launch risk and early cash needs. | Use this for the most likely planning case and budget set. | Use this to test upside if enrollment stays full and pricing holds. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Bartending School Porter's Five Forces Analysis

- Bartending School BCG Matrix

- Bartending School Business Model Canvas

- What Are The 5 KPI Metrics For Bartending School Business?

- Bartending School Business Plan Template in Pre-Written Word

- How Increase Bartending School Profits?

- What Are Bartending School Operating Costs?

- Bartending School Startup Costs: $824K Opening Cash Plan

- Bartending School Financial Model Template in Excel

- How To Open A Bartending School In 8–16 Weeks With First Cohort

- How To Write A Business Plan For Bartending School?

- Bartending School Marketing Mix

- Bartending School Marketing Plan

- Bartending School Business Proposal

- Bartending School PESTEL Analysis

- Bartending School Pitch Deck Example Editable PPTX

- Bartending School Business SWOT Analysis

- Bartending School Value Proposition Canvas

Frequently Asked Questions

A modeled owner can plan around a $95K School Director salary if they fill that role Business EBITDA is separate: $515K in Year 1 on $1138M revenue, rising to $9927M by Year 5 on $12620M revenue Actual take-home depends on reserves, debt service, taxes, reinvestment, and whether profits are distributed