Owner income$115k

Owner income$115kHow Much Can a Battery Jump Start Service Owner Make? $115k Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$115k  Net margin80.5%

Net margin80.5% Revenue for target pay$143k

Revenue for target pay$143k Business difficultyHard

Business difficultyHard

You’re planning owner pay before the service has steady call volume, so separate payroll from profit This five-year model shows $115,000 annual CEO pay, Year 1 revenue of $517,000, and breakeven in Month 13 It excludes personal taxes, debt service, market guarantees, and automatic owner distributions

Owner income$115kNet margin80.5%Revenue for target pay$143kBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the financial model?

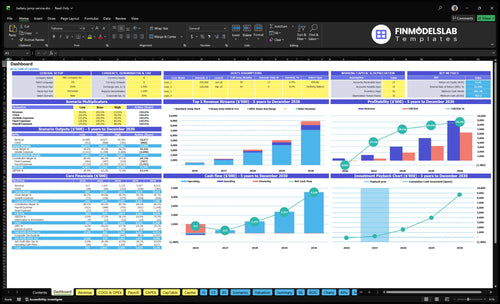

The Battery Jump Start Service Financial Model Template shows dashboard, income outputs, assumptions, call volume, pricing, costs, overhead, payroll, capex, scenarios, cash flow, breakeven, payback, and owner income charts—open it to see Year 1 to Year 5 revenue from $517,000 to $8915 million, EBITDA from -$83,000 to $6270 million, Month 13 breakeven, Month 21 payback, and $767,000 minimum cash need in Month 12.

Owner-income model highlights

- Owner take-home shown

- Revenue and EBITDA tracked

- Cash need and payback

Should I scale a battery jump start service beyond owner-operated calls?

If you stay owner-operated, the Battery Jump Start Service keeps margin tight, but it caps call volume and response hours. Hiring drivers can widen coverage, yet it adds payroll, dispatch supervision, quality control, insurance exposure, and utilization risk. Here’s the quick math: modeled payroll rises from $365,000 in Year 1 to $960,000 in Year 5 while revenue grows from $517,000 to $8.915 million, so judge hiring by take-home after reserves, not gross call count.

Owner-operated

- Protects margin.

- Caps response hours.

- Limits call volume.

- Fits low-overhead ops.

Hiring drivers

- Expands service coverage.

- Adds payroll and supervision.

- Raises insurance exposure.

- Needs reserve-backed payback.

Which battery jump start service costs reduce owner take-home most?

Payroll cuts owner take-home the most, because Year 1 payroll is $365,000, while the modeled direct percentage costs also bite hard: 120% digital marketing, 30% payment processing, 25% platform infrastructure, and 20% technician referral bonuses. If you’re mapping this out, see How Do I Write A Business Plan For Battery Jump Start Service? and separate direct job costs from fixed overhead and owner reserves. Fixed overhead is $6,450 a month, and capex is $117,000, so those hit cash too, but payroll and direct costs hit take-home first.

Biggest cost drains

- Payroll is the largest step cost.

- Digital marketing is 120% direct cost.

- Payment processing adds 30%.

- Platform infrastructure adds 25%.

Cash hits to isolate

- Referral bonuses add 20%.

- Fixed overhead is $6,450 per month.

- Capex totals $117,000.

- Keep owner reserves separate.

What revenue is needed for battery jump start owner pay?

For Battery Jump Start Service, the owner-pay target is $115,000, with $77,400 in fixed overhead. Here’s the quick math: closing the $83,000 EBITDA gap needs about $103,000 more revenue at the stated 80.5% contribution rate, and the model reaches breakeven in Month 13. Keep target pay separate from distributions, reinvestment, debt service, and a cash cushion.

Owner pay math

- $115,000 modeled CEO pay

- $77,400 fixed overhead

- $83,000 EBITDA gap

- About $103,000 more revenue

Cash guardrails

- Breakeven lands in Month 13

- Use pay target only for salary

- Keep debt service separate

- Hold a cash cushion

Want the six drivers that move owner income?

1

5K-75KCall Volume

More completed jumps spread the $77.4K fixed base and the $115K owner payroll, and EBITDA rises from -$83K to $6.27M as volume scales.

2

$85-$95Average Ticket

Moving the standard jump from $85 to $95 lifts cash on every call with little extra fixed cost.

3

19.5%-14.8%Dispatch Efficiency

Faster routing and cleaner dispatch keep the blended variable load down, so more of each dollar stays after the job.

4

12.0%-7.5%Acquisition Cost

Marketing falls from 12.0% to 7.5% of revenue, so cheaper bookings protect cash as volume grows.

5

7.5%-7.3%Fee Load

Processing, platform, and tech payout costs stay near each call, so small fee cuts lift margin fast.

6

$115KOwner Labor

Keeping the CEO at 1.0 FTE with a $115K salary and using hired help only when needed stops labor from eating margin.

Battery Jump Start Service Core Six Income Drivers

Completed Call Volume

Completed Call Volume

Completed paid calls set the revenue ceiling. Year 1 assumes 5,000 jump starts, or about 417 per month, rising to 75,000, or 6,250 per month, by Year 5. That count must exclude inquiries, cancellations, no-shows, and unpaid club leads. If completion rate slips, owner income falls even when inbound demand looks busy.

Here’s the quick math: more completed calls raise revenue, but only if response capacity, dispatch quality, and cost per call stay under control. The owner is paid on finished jobs, so the key inputs are completed calls, completion rate, technician availability, and the cost to serve each call.

Track completed calls, not just leads

Measure completed-call rate, completed calls per shift, and revenue per route hour. Split volume by source: direct customers, local search, paid search, fleets, insurance dispatch, motor-club dispatch, repeat demand, and referrals. Each channel should be judged on net revenue after lead cost or discounts, not gross inquiries.

- Count paid completions only.

- Track cancellations and no-shows.

- Watch calls per shift.

- Watch cost per completed call.

If response times stretch or tech capacity is thin, volume can rise while take-home pay falls. That’s the part owners miss.

1

Average Ticket And Pricing

Average Ticket

Average ticket is the blended price per completed jump start after standard fees, after-hours premiums, heavy-duty fees, mileage, urgency, and channel mix. Year 1 pricing is $85 standard, $35 after-hours, and $125 heavy-duty; the model’s Year 1 revenue per standard call is $10340. If the mix shifts to lower-fee jobs, owner pay falls even when calls stay flat.

Price by Job Type

Measure realized price by job type and channel, not just the quote. Track dispatch fees, discounts, and the share of after-hours and long-mileage calls. By Year 5, pricing rises to $95, $45, and $140, but one universal price can still compress net revenue in competitive zones. Price the job you drive, not the lead you hoped to close.

2

Response Area And Route Efficiency

Route Radius and Call Density

Response area changes how many paid jump starts one tech can finish in a shift. Dense zones usually lift calls per shift and cut fuel, drive time, and vehicle wear, so owner income improves faster than revenue alone. A wider radius can add jobs, but if travel blocks the next call, revenue per route hour falls and profit shrinks.

This driver depends on completed-call rate, dispatch speed, and how far apart jobs sit. Year 1 volume is modeled at 5,000 calls a year, or about 417 per month, so the service area has to support those calls without long dead miles. Bigger coverage is not automatically better if it lowers margin.

Track Route Hours, Not Just Leads

Measure each shift by calls per route hour, drive time between calls, and completed-call rate. Then compare dense ZIP codes with wider zones on net profit, not just top-line revenue. If a zone adds calls but slows the next dispatch, it is hurting take-home pay.

- Track revenue per route hour.

- Cut low-density service zones.

- Group jobs by nearby ZIP codes.

- Review fuel and wear monthly.

Use the numbers to set service boundaries and staffing. The goal is simple: keep the tech moving between paid calls, because idle drive time turns a busy day into weak margin.

3

Customer Acquisition And Dispatch Mix

Customer Mix And Lead Cost

For a battery jump start service, customer acquisition cost goes straight against take-home. In Year 1, digital marketing and customer acquisition equals 120% of revenue, so gross call volume can rise while owner profit still stays thin or negative. By Year 5, that falls to 75%, which is better, but the mix still decides whether each completed call adds cash or just buys traffic.

Track net revenue by source: direct customers, local search, paid search, fleet relationships, insurance dispatch, motor-club dispatch, repeat demand, and referrals. The key inputs are lead cost, discounted pricing, completed paid calls, and repeat rate. Gross calls are not enough; if a channel brings cheap volume but weak net revenue, it can drag down the owner’s ability to pay themselves.

Measure Net Revenue Per Source

Build a simple channel scorecard: completed calls, lead cost, discount, and net revenue per booked job. That tells you which sources actually fund payroll, fuel, software, and owner draw. For example, a paid search lead that books often can still lose money if the lead cost and promo price eat the margin.

- Separate paid, direct, and referral leads.

- Count only completed paid calls.

- Compare net revenue after discounts.

- Watch repeat and referral share monthly.

Push budget toward channels with the best net return, not the highest call count. If one source needs heavy discounting, cap spend fast. What matters is cash left after lead cost, because that is what protects owner pay and working capital.

4

Direct Operating Cost Per Call

Direct Cost per Call

If direct operating cost per jump start call runs at 195% of revenue in Year 1, each job loses money before fixed overhead. That means gross margin = -95% on a variable-cost basis, and even Year 5 at 148% is still -48%, so owner pay stays under pressure until the cost stack comes down.

This cost includes payment fees, platform fees, job-linked marketing, technician bonuses, fuel, mileage, booster pack wear, payment disputes, and roadside safety supplies. Keep those separate from fixed overhead like insurance, software, office admin, and owner pay, or you’ll miss where the cash is leaking.

Track the Cost Stack

Build cost per completed call from real job data: completed calls, average ticket, fee rates, miles driven, bonus per dispatch, and replacement rate for booster packs and supplies. Use completed calls, not leads or cancellations, because only paid jobs fund margin and owner draw.

- Measure cost per call weekly

- Separate job cost from overhead

- Track disputes by technician

- Watch fuel and mileage by zone

At 5,000 calls a year, even a $1 leak per job burns $5,000 of annual profit. That’s why small fixes matter: tighter routing, lower payment fees, fewer disputes, and fewer bonus dollars per call all flow straight into cash flow and take-home income.

5

Owner Role And Staffing

Owner-Led Staffing

If you run jump starts yourself, you keep the labor margin in-house, but you cap hours, response coverage, and your own time. That matters because the model scales from 40 FTE in Year 1 to 160 FTE in Year 5, so owner income rises only if added staff actually convert into paid calls, not just payroll.

Hiring technicians lifts capacity, but it also adds payroll, training, supervision, insurance, scheduling, and idle -time risk. The key test is reserve-adjusted take-home, not gross revenue. If a truck or tech is paid to wait, margin drops fast, and the owner pays for that slack.

Measure Labor by Utilization

Track completed calls per shift, drive time, idle hours, and labor cost per completed job. In this kind of roadside work, more headcount only helps when each technician stays busy enough to cover wages and overhead. One clean rule: if utilization falls, owner pay falls.

- Measure calls per technician shift

- Watch idle time and dispatch gaps

- Link pay to completed jobs

- Review reserve-adjusted profit weekly

6

Compare lean, base, and high-case owner-income scenarios

Owner income scenarios

Owner income moves with call volume, after-hours demand, and staffing. Higher utilization lifts EBITDA fast, but payroll, marketing, and support costs can absorb much of the gain.

| Scenario | Low CaseDownside case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | Lower earnings path built on Year 1 demand and startup-funded owner pay. | Modeled middle case with stronger volume and profit funding owner pay. | Stronger upside path with high volume and the largest staffing base. |

| Typical setup | Uses Year 1 assumptions: 5,000 standard calls, 1,200 after-hours surcharges, 400 heavy-duty fees, $517k revenue, -$83k EBITDA, and $115k modeled owner payroll. | Uses Year 3 assumptions: 28,000 standard calls, 7,000 after-hours surcharges, 2,500 heavy-duty fees, $3.125m revenue, $1.815m EBITDA, and expanded support staffing. | Uses Year 5 assumptions: 75,000 standard calls, 18,000 after-hours surcharges, 7,000 heavy-duty fees, $8.915m revenue, $6.270m EBITDA, and $960k payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $115,000 modeled payStartup pay | Profit-funded owner payCore income | High-profit owner payUpside income |

| Best fit | Use this to stress-test the launch year and cash needs. | Use this for a scaled but still controlled dispatch model. | Use this to test what pay can look like if dispatch and technician capacity scale cleanly. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Battery Jump Start Service Porter's Five Forces Analysis

- Battery Jump Start Service BCG Matrix

- Battery Jump Start Service Business Model Canvas

- What Are The 5 Core KPIs For Battery Jump Start Service?

- Battery Jump Start Service Business Plan Template in Pre-Written Word

- How Increase Battery Jump Start Service Profits?

- What Are Operating Costs For Battery Jump Start Service?

- Battery Jump Start Service Startup Costs: $117k CAPEX And $767k Cash

- Battery Jump Start Service Financial Model Template in Excel

- How To Start A Battery Jump Start Service In 2 To 6 Weeks

- How Do I Write A Business Plan For Battery Jump Start Service?

- Battery Jump Start Service Marketing Mix

- Battery Jump Start Service Marketing Plan

- Battery Jump Start Service Business Proposal

- Battery Jump Start Service PESTEL Analysis

- Battery Jump Start Service Pitch Deck Example Editable PPTX

- Battery Jump Start Service Business SWOT Analysis

- Battery Jump Start Service Value Proposition Canvas

Frequently Asked Questions

The model shows $517,000 in Year 1 revenue and $8915 million by Year 5 under its call-volume assumptions Owner payroll is modeled at $115,000 per year, but Year 1 EBITDA is negative $83,000, so distributions are not supported early Breakeven appears in Month 13, before taxes, debt service, and reserves