Owner incomeY1 $0; Y2 $104K; Y3 $916K

Owner incomeY1 $0; Y2 $104K; Y3 $916KHow Much Biometric Security Systems Owners Can Make: $0–$916K

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 $0; Y2 $104K; Y3 $916K  Net margin66.5% to 70.5%

Net margin66.5% to 70.5% Revenue for target pay~$313K

Revenue for target pay~$313K Business difficultyHard

Business difficultyHard

A biometric security systems owner can make little or no sustainable take-home in the first year if payroll and marketing are built ahead of revenue Using the researched assumptions, Year 1 revenue is about $680K, but direct costs, payroll, marketing, and fixed overhead create an estimated operating loss of about $281K By Year 2, revenue rises to about $156M and operating profit is about $104K before reserves, taxes, and distributions By Year 3, revenue is about $30M and operating profit reaches about $916K, assuming the sales pipeline, installation capacity, and maintenance attach rate hold

Owner incomeY1 $0; Y2 $104K; Y3 $916KNet margin66.5% to 70.5%Revenue for target pay~$313KBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, taxes, debt, and reinvestment.

Want to see owner income in the Biometric Security Systems model?

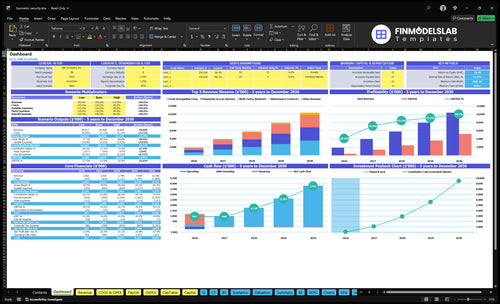

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Biometric Security Systems Financial Model Template; charts run from about $680K in Year 1 to about $30M in Year 3. Open the model.

Owner-income model highlights

- Owner take-home is clear

- Revenue build drives profit

- Scenarios test cash flow

How much revenue does a biometric security business need to pay the owner?

Biometric Security Systems needs about $11.0M in revenue before owner distributions if Year 1 fixed load is $7.328M and contribution margin is 66.5%. If the owner also wants an extra $150K before taxes and reserves, the revenue target rises to about $13.3M. Revenue alone won’t pay the owner if hardware discounts, technician utilization, or callbacks cut margin.

Core revenue load

- $500K known payroll

- $120K marketing

- $1.128M fixed overhead

- $7.328M total fixed load

Owner pay pressure

- 66.5% contribution margin

- $11.0M break-even revenue

- $150K extra owner target

- $13.3M revenue with that target

How much can a biometric security systems owner make?

A Biometric Security Systems owner can make $0 in sustainable Year 1 distributions, about $104K operating profit in Year 2, and about $916K operating profit in Year 3 in this researched model. Owner pay is driven by profit and cash, not sales alone, which is why What Is The Main Goal Of Biometric Security Systems? matters when pricing installs, service contracts, and support.

Owner Take-Home

- Year 1: about $0 sustainable distribution

- Year 2: about $104K operating profit

- Year 3: about $916K operating profit

- $95K GM salary can become owner pay

Quick Math

- $680K Year 1 revenue is not enough

- Direct costs equal about 33.5% of revenue

- Known payroll is $500K plus $120K marketing

- Fixed overhead is about $1.128M

Can a biometric security systems business support a full-time owner income?

Yes, but not in Year 1. For Biometric Security Systems, Year 1 is about negative $281K operating profit after direct costs, known payroll, marketing, and overhead, so there’s no clean owner draw; Year 2 can only support a modest distribution if reserves, debt service, and working capital stay tight. By Year 3, the base case shows about $916K operating profit before distributions and taxes, which can support full-time owner income.

Income timing

- Year 1: no clean distribution

- -$281K operating profit

- Direct costs plus payroll hurt cash

- Marketing and overhead stay fixed

Model trade-offs

- Year 2: modest draw only

- Control reserves and debt service

- Year 3: about $916K profit

- Owner-operator limits installs; staffed models lift capacity but raise break-even risk

Want the six drivers that move owner income most?

1

12/moMonthly Installs

More installs spread the fixed load and turn the 150 Year 1 customer base into cash faster.

2

$125-$175Install Value

Higher billed hours at $125 to $175 an hour raise revenue per project and lift gross profit.

3

67%Hardware Margin

Lower hardware and material cost lifts contribution margin on every system sold.

4

2.5-4.5hTech Productivity

More billable hours per active customer improve labor yield and protect margin from callbacks.

5

25%Recurring Revenue

Maintenance contracts add repeat revenue and smooth cash flow between installs.

6

$655KOverhead Load

Overhead sets break-even, so fixed costs hit take-home hard until volume catches up.

Biometric Security Systems Core Six Income Drivers

Installation Volume And Sales Pipeline

Completed Installs Drive Income

Income here comes from completed, profitable installs, not leads or quotes. If Year 1 marketing is $120K at $800 CAC, that implies about 150 acquired customers, but site surveys, proposals, close rate, and install capacity decide how many become revenue. If jobs slip, technicians sit underused while $500K in Year 1 payroll and $1,128K fixed overhead still run.

Measure the Funnel to Protect Profit

Track qualified leads, proposal close rate, install backlog, completed jobs, and gross profit per install. Here’s the quick math: leads only matter when they turn into installs that cover labor and overhead. If scheduling is weak, revenue slows, cash gets tight, and owner pay gets squeezed even with a full pipeline.

- Count surveys booked each week.

- Track quotes sent and won.

- Watch backlog by install date.

- Review gross profit per job.

1

Average Project Value And Customer Mix

Average Project Value And Customer Mix

Average project value moves up when the mix shifts toward higher-spec biometric access control jobs. In Year 1, the rate card is $125 for fingerprint access, $150 for facial recognition entry, $175 for multi-factor biometric, and $95 for maintenance work, so a heavier mix of multi-door commercial sites and integrated controllers can lift revenue per customer and gross profit.

The key inputs are quoted hours, device count, doors per site, and service attach rate. Year 1 mix is 45% fingerprint, 30% facial recognition, 15% multi-factor, and 25% maintenance contracts. If the mix stays low-spec, owner income stays tied to smaller jobs; if it shifts up, each closed deal supports more profit and better cash flow for pay draws.

Raise project value with mix control

Track each quote by job type, hours sold vs. hours used, and doors per site. That shows whether you are selling one-door fingerprint installs or larger commercial systems that justify higher pricing. One bigger site can matter more than several small ones.

Watch the maintenance attach rate and push it on every install, because recurring work at $95 per hour smooths cash flow. If facial recognition and multi-factor jobs are closing slowly, test pricing, scope, and device count before discounting, since lower ticket jobs can raise workload without lifting owner pay.

- Track mix by project type

- Price by site complexity

- Sell maintenance on every install

- Compare quoted hours to actual hours

2

Hardware Margin And Vendor Purchasing

Hardware Margin And Vendor Purchasing

Hardware cost is a direct drag on gross profit. In Year 1, biometric hardware components equal 18% of revenue, then improve to 16% in Year 3 and 15% in Year 5. That gap matters because every point saved at purchase shows up before labor, fuel, callbacks, payroll, and overhead cut into owner pay.

Here’s the quick math: better vendor terms, volume discounts, and markup discipline lift gross margin, but hardware margin is still not take-home income. Poor device selection can add warranty claims, return visits, and support load, which can wipe out the savings fast. Track hardware cost percentage, warranty claims, discount tiers, and gross profit by device type.

Buy Smarter, Protect Margin

Set a buying rule for each device type and stick to it. Compare vendor quotes, then test whether the extra discount beats the added risk from weak specs or higher failure rates. If a cheaper unit creates more callbacks, it is not cheaper. The owner wins when procurement lowers cost without adding service work.

- Track cost by device type.

- Log warranty claims by vendor.

- Review discount tier changes monthly.

- Check gross profit after callbacks.

Use purchase data to price jobs, not gut feel. If one biometric line consistently lands below target margin, raise markup or drop it. If another line has fewer returns and stronger volume pricing, push more of that mix. That discipline protects cash flow and leaves more profit available for owner draw after operating costs.

3

Technician Labor Productivity

Technician Labor Productivity

Labor productivity is what keeps a biometric install profitable after the sale closes. In Year 1, subcontractor labor is 8% of revenue, then 7% in Year 3 and 6% in Year 5; if hours run over, that payroll comes out of gross profit and lowers the owner’s draw.

Known technician payroll is $165K in Year 1 for 3 installation technicians. A fingerprint system needs 12 hours, facial recognition needs 16 hours, and multi-factor biometric work needs 24 hours. Cabling, door hardware, integrations, travel time, and rework can erase quoted margin fast.

Track Hours, Not Just Installs

Watch billable utilization, hours quoted versus hours used, callbacks, and installs completed per technician. The goal is simple: finish jobs inside the quoted labor window and keep tech time on revenue work, not on fixes.

- Compare quoted hours to actual hours.

- Split new work from rework.

- Flag travel-heavy jobs early.

- Review productivity by system type.

If a 12-hour job turns into 16 hours, the extra 4 hours cuts gross margin on that sale. Higher utilization protects cash flow, keeps payroll covered, and leaves more income for the owner after overhead.

4

Recurring Maintenance Revenue

Recurring Maintenance Revenue

Recurring maintenance is the steady service income that comes after the install. In this model, adoption rises from 25% in Year 1 to 55% in Year 3 and 85% in Year 5, with maintenance rates moving from $95 per hour to $101 and $107. That makes revenue less dependent on new hardware jobs and helps owner pay stay steadier.

Here’s the quick math: more contracts mean more billed service hours, but they also bring support labor, response standards, and scheduling discipline. If monthly billable support hours lag or callbacks rise, margin drops fast. The real win is not just revenue; it’s cleaner cash flow and a higher value per customer account.

Measure Attach, Renewal, and Hours

Track attach rate, renewal rate, monthly billable support hours, and margin by contract. Those four inputs show whether maintenance is actually paying for the tech time it consumes. If the company sells lots of instal ls but renewals slip, recurring income looks good on paper and weak in cash.

- Attach maintenance on every install.

- Price by response level.

- Block service time weekly.

- Watch callback-driven labor.

Clean scheduling matters because service work can crowd out new installs. If support promises are tight and staffing is thin, owner draws get squeezed even when contract count is rising.

5

Overhead, Reserves, And Owner Role

Overhead That Cuts Draws

Owner pay starts after the company funds $94K per month in fixed overhead, or $1.128M per year, plus $120K Year 1 marketing and $500K of known payroll. That means operating profit is not the same as cash you can take home. Cash for draws = profit minus reserves, debt service, inventory, warranty work, and reinvestment.

If the owner fills the $95K General Manager role, that can be owner compensation, but the business still has to pay it. So the key question is not “Did we make profit?” It’s “After overhead and working cash needs, what’s left for the owner?”

Track Cash Before You Pay Yourself

Use a simple monthly bridge: operating profit, then subtract debt payments, reserve build, warranty spend, and inventory cash. Here’s the quick check: if overhead alone is $94K a month, owner draws need stable gross profit, not just a good sales month. One clean rule: don’t set draws from revenue.

- Track monthly overhead vs. budget.

- Set a reserve floor before draws.

- Separate owner salary from profit draw.

- Watch warranty and inventory cash needs.

If growth adds installs but cash stays tight, the company can look profitable and still starve the owner. That risk is highest when payroll, marketing, and support costs hit before service cash collects. Fund the business first, then pay the owner.

6

Compare lean, base, and growth owner-income scenarios

Owner income scenarios

Owner income moves with revenue mix, direct labor, and fixed staffing. These cases show how the model shifts from cash-tight launch to stronger scale.

| Scenario | Low CaseLaunch risk | Base CaseSteady case | High CaseScale upside |

|---|---|---|---|

| Launch model | This is the lower earnings path with a tight launch and thin room for owner pay. | This is the modeled middle path with normal execution and modest owner income. | This is the stronger earnings path with higher volume and better owner take. |

| Typical setup | Year 1-style launch with about $680K revenue, about 33.5% direct costs, a roughly $732.8K fixed load, and about -$281K operating profit before owner pay. | Year 2-style run with about $1.56M revenue, about 31.6% direct costs, and about $104K operating profit before reserves and taxes. | Year 3-style scale with about $3.0M revenue, about 29.5% direct costs, and about $916K operating profit as maintenance contracts and billable hours grow. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$281,000Cash reserve watch | $104,000Reserve and taxes | $916,000Growth mode |

| Best fit | Best for a founder who stays hands-on and needs tight cash control. | Best for an operator planning for normal growth with some reserve cushion. | Best for an owner moving toward management while the team handles more installs and support. |

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Biometric Security Systems Porter's Five Forces Analysis

- Biometric Security Systems BCG Matrix

- Biometric Security Systems Business Model Canvas

- 7 Critical KPIs for Biometric Security Systems Growth

- Biometric Security Systems Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Profitability in Biometric Security Systems

- How to Manage Monthly Running Costs for Biometric Security Systems

- Biometric Security Systems Startup Costs: $221K CAPEX Plan

- Biometric Security Systems Financial Model Template in Excel

- How To Start A Biometric Security Systems Business In 8–16 Weeks

- 7 Steps to Write Your Biometric Security Systems Business Plan

- Biometric Security Systems Marketing Mix

- Biometric Security Systems Marketing Plan

- Biometric Security Systems Business Proposal

- Biometric Security Systems PESTEL Analysis

- Biometric Security Systems Pitch Deck Example Editable PPTX

- Biometric Security Systems Business SWOT Analysis

- Biometric Security Systems Value Proposition Canvas

Frequently Asked Questions

A clean owner draw may be $0 in Year 1 under the researched assumptions because about $680K revenue does not cover direct costs, $500K known payroll, $120K marketing, and $1128K fixed overhead Year 2 shows about $104K operating profit, and Year 3 shows about $916K before taxes, reserves, debt, and distributions