Owner income$350k to $4.17M

Owner income$350k to $4.17MBird Netting Installation Owner Income: $350K Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$350k to $4.17M  Net margin32.6% to 67.9%

Net margin32.6% to 67.9% Revenue for target pay$1.07M to $6.14M

Revenue for target pay$1.07M to $6.14M Business difficultyHard

Business difficultyHard

You’re modeling owner take-home for a US pest control contractor that installs bird exclusion netting on commercial buildings, warehouses, canopies, loading docks, and parking structures In the provided five-year model, revenue grows from $1074M in Year 1 to $6136M in Year 5, with EBITDA rising from $350K to $4167M before taxes, debt service, reserves, and owner-specific distributions

Owner income$350k to $4.17MNet margin32.6% to 67.9%Revenue for target pay$1.07M to $6.14MBusiness difficultyHardWant to test your owner income target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Bird Netting Installation Service model?

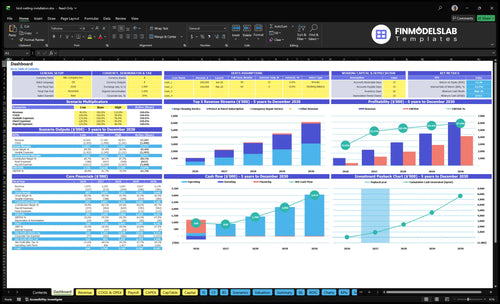

The Bird Netting Installation Service Financial Model Template dashboard shows revenue, EBITDA, breakeven, payback, cash, and owner-income capacity. Open the model.

Owner-income model highlights

- Owner take-home capacity

- Revenue and EBITDA

- Assumptions and scenarios

How much revenue does a bird netting business need to pay the owner?

For a Bird Netting Installation Service, revenue has to cover the cost stack first, so owner pay comes last. In this model, the business reaches Month 5 breakeven and supports about $350K EBITDA (earnings before interest, taxes, depreciation, and amortization) before taxes and owner draws after $325K payroll, $1,314K fixed overhead, $45K marketing, 100% materials, and 60% fuel and vehicle maintenance. The clean rule is simple: pay the owner only after reserves and working capital are funded.

What revenue has to cover

- $325K payroll first

- $1,314K fixed overhead

- $45K marketing spend

- 100% materials and 60% vehicle costs

When owner pay is safe

- Breakeven lands in Month 5

- EBITDA reaches about $350K

- Subtract debt service before draws

- Owner pay is a planning goal

What costs affect bird netting installation profit?

For Bird Netting Installation Service, profit gets squeezed first by installation materials and netting supplies, which can equal 100% of Year 1 revenue and still sit at 80% by Year 5; see How Increase Bird Netting Installation Service Profits?. Fuel and vehicle maintenance can run at 60% and ease to 40%, while payroll climbs from $325K to $740K. Fixed overhead is $1.314M per year, marketing rises from $45K to $140K, and commercial liability insurance adds $1,200 per month.

Main cost stack

- Materials: up to 100% of Year 1 revenue

- Netting supplies: still 80% by Year 5

- Fuel and maintenance: 60% to 40%

- Payroll: $325K to $740K

Profit leaks

- Fixed overhead: $1.314M yearly

- Marketing: $45K to $140K

- Insurance: $1,200 per month

- Callbacks, lift time, travel gaps cut take-home

How does a bird netting installation business scale?

Bird Netting Installation Service scales when bigger commercial jobs raise revenue per account and keep crews booked, but the tradeoff is heavier payroll, vehicles, lifts, insurance, and cash timing. Here’s the quick math: modeled revenue rises from $1,074M to $6,136M, lead installation technicians move from 2 to 6, and sales staff from 1 to 3. EBITDA grows from $350K to $4,167M, but minimum cash need reaches $673K and payback takes 13 months.

Growth drivers

- Larger commercial jobs lift revenue

- More crew output keeps calendars full

- Warehouse work adds volume

- Loading dock jobs improve density

Cash risks

- Payroll rises with each crew

- Vehicles and lifts add fixed cost

- Slow payments squeeze cash

- Poor scheduling hurts utilization

Want the six main income drivers?

1

$1.1M-$6.1MProject Volume

More completed installs push revenue from $1.074M to $6.136M and raise EBITDA from $350K to $4.167M.

2

84%-88%Gross Margin

Direct costs ease as materials drop from 10% to 8% and vehicle costs from 6% to 4%, so more sales stay in EBITDA.

3

$850-$2.6KAvg Contract

Higher-ticket jobs from $850 to $950 for the subscription and $2.2K to $2.6K for deep cleaning lift revenue per sale.

4

CAC $390-$450Lead Flow

Marketing budget grows from $45K to $140K, and CAC still needs to fall from $450 to $390 to keep new jobs profitable.

5

2-6 FTECrew Productivity

Lead technician staffing rises from 2.0 to 6.0 FTE, so each crew must keep output high to protect margin.

6

$11K/moOverhead Discipline

Fixed costs total about $10.95K a month, or $131K a year, so overhead creep hits take-home fast.

Bird Netting Installation Service Core Six Income Drivers

Average Contract Value

Average Contract Value

Average contract value (ACV) is the average dollars each account brings in across the subscription, deep clean, and emergency repair mix. For this model, pricing of $850 to $950 per month for service, $2,200 to $2,600 for deep cleaning, and $1,200 to $1,400 for emergency repair can lift revenue fast, but only if scope is priced correctly. Bigger buildings and tougher access can raise sales, yet they also raise labor, equipment, safety, and callback risk.

One clean job at $950/month can be better than a bigger one with thin margin. If pricing misses material takeoff, lift access, crew hours, or the target margin, the owner may grow revenue and still pay themselves less. The real win is higher ACV with controlled direct cost, not just a higher quote.

Price by scope, not by guesswork

Build every quote from the same inputs: material takeoff, access needs, crew hours, and margin target. That keeps ACV tied to job size and stops underbidding on larger buildings, commercial sites, and hard-to-reach work where costs can jump fast.

- Track monthly, deep clean, repair mix

- Price lift access and safety exposure

- Flag callbacks before they erase margin

- Compare quote price to crew hours

What this estimate hides: a higher ACV only helps owner income if direct job cost stays in line. If a $2,600 deep clean needs extra equipment or repeat visits, the gross margin can fall below a smaller recurring account that runs clean and low-touch.

1

Project Volume And Utilization

Project Volume and Utilization

Owner income rises when crews spend more days on qualified installs and fewer on estimates, travel, weather delays, access problems, and idle gaps. Here’s the quick math: modeled marketing spend climbs from $45K to $140K, CAC improves from $450 to $390, and revenue grows from $1,074M to $6,136M. That only works if sales turns into scheduled work.

This driver includes leads, close rate, estimate time, crew capacity, site access, and sales cycle length. One clean rule: more booked work only helps if crews can actually finish it. Unlimited demand is a bad assumption; property access, facility schedules, and weather can cap monthly volume, so utilization is what turns pipeline into owner pay.

Measure booked work, not just leads

Track qualified jobs per crew day, estimate-to-close rate, and the share of days lost to travel or access delays. If crews are underbooked, the business pays for payroll, vehicles, and time without creating billable output. That lowers cash available for the owner, even when revenue looks busy on paper.

Build the schedule around access windows and facility rules, then price and staff for the real job count. Watch CAC against the $450 to $390 range and test whether more spend actually lifts booked installs. If marketing rises to $140K but crew slots are full, the extra spend just buys backlog, not faster owner income.

- Track jobs sold per month.

- Measure crew days used.

- Log delay causes daily.

- Match marketing to capacity.

2

Gross Margin After Direct Job Costs

Direct Job Margin

When a job burns extra netting, hardware, lift time, or labor, gross margin after direct job costs drops before overhead is even counted. This model assumes installation materials and netting supplies at 100% of revenue in Year 1, improving to 80% by Year 5; fuel and vehicle maintenance starts at 60% and improves to 40%.

The key inputs are takeoff accuracy, waste, labor hours, travel, lift time, and rework. A missed measurement or extra truck roll can turn a profitable service call into thin or negative EBITDA, which cuts the owner’s draw even if sales stay steady.

Protect Job Margin Fast

Price each site from a real takeoff, not a rough guess. Track estimated vs actual material use, crew hours, lift days, fuel, maintenance, and callbacks by job. If access is hard or rework risk is high, add margin at quote time, because the cost shows up on the first service call.

- Match takeoff to actual usage.

- Log waste and rework by job.

- Count extra truck rolls fast.

One clean job can fund owner pay; one bad install can erase it. Watch the direct-cost rate weekly, and push any site with poor access, long travel, or repeat fixes into a higher price tier before the crew starts.

3

Crew Productivity And Owner Role

Crew Productivity and Owner Role

Owner time is the hidden profit driver here. If the owner installs, estimates, sells, or supervises crews, cash can stay tighter in Year 1, but sales time, scheduling control, and job capacity drop. The model starts at $325K payroll with 1 general manager, 2 lead installation technicians, 1 sales rep, and 1 admin coordinator; by Year 5 payroll reaches $740K as technicians rise to 6 and sales staff to 3.

One more technician is not free. The added payroll, or $415K more than Year 1, has to be paid before owner draw. Hands-on work can protect early cash, but if the owner stays in the field too long, quoting slows, crews wait, and revenue growth can stall even when demand is there.

Protect Owner Time and Crew Output

Track where the owner’s hours go: installs, estimates, sales calls, crew supervision, and subcontractor management. The driver improves when the owner shifts from production to closing work and scheduling control, because that keeps the crew busy and reduces idle days. What gets measured gets managed.

Use a simple weekly dashboard: estimates sent, jobs sold, crew days worked, and hours spent in the field. If the owner is still doing most installs, set a target to hand off the repeatable work first, then keep only the jobs that need pricing judgment or client control.

- Track owner hours by task

- Watch crew days sold vs. worked

- Compare payroll to output monthly

4

Commercial Lead Flow And Sales Mix

Commercial Lead Mix

When leads come from property managers, facility teams, pest control partners, roofing contractors, and general contractors, the owner can sell larger jobs that turn into repeat subscription accounts plus profitable add-ons. The model states 1000% of customers stay on subscription, while deep cleaning attach rate drops from 400% to 200% and emergency repair rises from 50% to 150%. One-off work can lift sales, but it can also weaken recurring income and squeeze owner pay.

What this driver includes is lead source, close rate, CAC (customer acquisition cost), estimate time, and project quality. If estimate time runs long or project quality slips, the owner pays more in labor and callbacks before the job turns into monthly cash flow. Better-fit leads improve take-home income only when the work is priced to cover access, materials, and rework risk.

Track Lead Quality

Measure close rate by source, CAC, and how many sold jobs become subscription versus add-on work. Keep the mix simple: subscription, deep cleaning, and emergency repair. If a source sends more emergency repairs than monthly accounts, revenue may rise, but profit can still stay thin because dispatch, scheduling, and callback risk go up.

- Track close rate by source.

- Track CAC and estimate hours.

- Track subscription share monthly.

- Track callback rate by crew.

- Track project quality after install.

Also watch estimate time. Faster quotes help cash flow, but only if they still screen for fit. The best leads are the ones that close into long-running accounts with low rework and steady monthly billing, because that supports owner draw without forcing the same selling effort every month.

5

Overhead, Insurance, And Reserves

Lean Fixed Overhead

Owner pay starts after the business covers $1.314M in yearly fixed overhead, or about $109.5K/month. The disclosed lines add to $666K—rent $54K, commercial liability insurance $144K, software $42K, utilities $72K, professional fees $18K, and vehicle leases $336K—so there’s another $648K of overhead in the model.

Insurance is not optional here. It protects work on commercial roofs, lifts, and occupied sites, but if overhead creeps up, operating profit drops before the owner can pay themselves. With startup capex of $257K and minimum cash of $673K, profit should be treated as a buffer until those reserves are funded.

Track Cash Runway

Measure three things every month: fixed overhead run rate, cash reserve, and lease load. The model’s $673K minimum cash means you need enough liquidity to absorb slow collections, weather delays, and equipment downtime. One clean rule: if reserves fall below the floor, owner draws pause.

- Track overhead per month.

- Review insurance at renewal.

- Use cash, not profit guesses.

- Watch vehicle lease utilization.

- Separate capex from take-home.

Set a reserve target before paying bonuses or extra distributions. If the business cannot cover $109.5K/month in fixed overhead plus the cash floor, the owner’s income is exposed even when projects are booked and the profit line looks healthy.

6

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner income rises as the business moves from Year 1 ramp-up to Year 3 stability and Year 5 scale. Materials, vehicle costs, payroll, taxes, debt service, reserves, and reinvestment all cut what reaches the owner.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path tied to Year 1 scale and early ramp-up. | This is the modeled mid-case tied to Year 3 scale and steadier job flow. | This is the stronger earnings path tied to Year 5 scale and fuller crew use. |

| Typical setup | Year 1 revenue is $1.074M with $350K EBITDA, 10.0% materials, 6.0% fuel and vehicle costs, $45K marketing, and $325K payroll, so owner draw stays tight until Month 5 breakeven. | Year 3 revenue is $3.267M with $1.969M EBITDA, 9.0% materials, 5.0% fuel and vehicle costs, $85K marketing, and $510K payroll, which supports a steadier owner draw after reserves. | Year 5 revenue is $6.136M with $4.167M EBITDA, 8.0% materials, 4.0% fuel and vehicle costs, $140K marketing, and $740K payroll, which can support a larger owner draw after reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $350K EBITDALow draw | $1.97M EBITDABase draw | $4.17M EBITDAUpside draw |

| Best fit | Best for owners stress-testing the launch ramp, cash reserve needs, and slower sales conversion. | Best for owners planning to run the model's middle path with room for reserves, taxes, debt service, and reinvestment before draw. | Best for owners testing the upside case where higher volume can support draw after reinvestment and overhead are covered. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Bird Netting Installation Service Porter's Five Forces Analysis

- Bird Netting Installation Service BCG Matrix

- Bird Netting Installation Service Business Model Canvas

- What 5 KPIs Should Bird Netting Installation Service Business Track?

- Bird Netting Installation Service Business Plan Template in Pre-Written Word

- How Increase Bird Netting Installation Service Profits?

- What Are Operating Costs For Bird Netting Installation Service?

- Bird Netting Installation Startup Costs: $673K Funding Plan

- Bird Netting Installation Financial Model Template in Excel

- How To Start A Bird Netting Installation Service In 6–10 Weeks

- How To Write A Business Plan For Bird Netting Installation Service?

- Bird Netting Installation Service Marketing Mix

- Bird Netting Installation Service Marketing Plan

- Bird Netting Installation Service Business Proposal

- Bird Netting Installation Service PESTEL Analysis

- Bird Netting Pitch Deck Example Editable PPTX

- Bird Netting Installation Service Business SWOT Analysis

- Bird Netting Installation Service Value Proposition Canvas

Frequently Asked Questions

The model shows $350K of Year 1 EBITDA and $4167M by Year 5, but that is not guaranteed owner pay EBITDA comes before taxes, debt service, reserves, reinvestment, and owner-specific distributions Revenue grows from $1074M to $6136M, with breakeven modeled in Month 5