Owner income$60k/yr

Owner income$60k/yrHow Much Boutique Gift Shop Owners Make at $308k Year 1 Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$60k/yr  Net margin19%

Net margin19% Revenue for target pay$258k/yr

Revenue for target pay$258k/yr Business difficultyHard

Business difficultyHard

Under the researched assumptions, a boutique gift shop owner has a modeled $60,000 annual owner-manager salary plus potential profit if the store hits plan In Year 1, the model produces about $308,000 in sales, an 86% gross margin after product cost, and about $106,000 in operating profit before taxes, debt, and extra inventory reserves That profit is not the same as spendable cash, because launch costs, stock buying, slow inventory, and working capital can hold back distributions The practical answer is: owner income can be meaningful, but only if traffic, conversion, margin, and payroll stay disciplined

Owner income$60k/yrNet margin19%Revenue for target pay$258k/yrBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

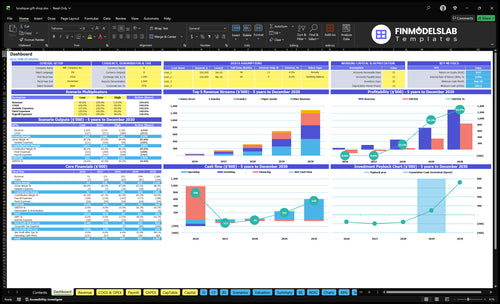

How do you check owner income in the Boutique Gift Shop model?

This screenshot shows revenue, margin, costs, and owner income assumptions in the Boutique Gift Shop Financial Model Template; open it.

Owner-income model highlights

- Owner pay capacity

- Monthly sales; $308k Year 1

- Gross profit and operating profit

- Cash needs and reserves

- Launch capex $573k

- Initial inventory $15k

- Fixed overhead $4,475

- Staffing ramps through Year 5

- Assumptions drive scenarios

What gross margin does a boutique gift shop need?

For a Boutique Gift Shop, gross margin is a sensitivity, not a fixed rule; the model assumes 14% cost of goods in Year 1, so product gross margin is 86%. After 3% payment processing and 2% packaging, contribution margin is 81%, and every 1-point margin loss on $308k revenue cuts about $3,100 a year of owner income. For startup-cost context, see How Much Does It Cost To Open A Boutique Gift Shop?.

Core math

- 14% COGS means 86% gross margin.

- 3% processing lowers cash kept.

- 2% packaging lowers cash kept.

- 81% funds owner pay.

Margin risks

- Year 1 mix: 30% ceramics.

- Year 1 mix: 25% jewelry.

- Year 1 mix: 20% paper goods.

- Year 1 mix: 25% home decor.

How much revenue does a gift shop need to pay the owner?

Boutique Gift Shop needs about $14,800 in monthly revenue just to cover a $5,000 owner salary, $2,500 associate payroll, and $4,475 fixed overhead at an 81% contribution margin. If you want $8,000 of owner cash before taxes and reserves, the target rises to about $18,500 a month. Here’s the quick math: ($5,000 + $2,500 + $4,475) ÷ 0.81.

Pay floor

- $5,000 owner salary

- $2,500 associate payroll

- $4,475 fixed overhead

- $14,800 revenue floor

Cash target

- $8,000 owner cash goal

- $18,500 monthly revenue target

- 81% contribution margin

- $257k modeled Year 1 sales

Can you make a living owning a boutique gift shop?

Yes, a Boutique Gift Shop can support a living under this model, but not by default; Year 1 includes a $60k owner-manager salary plus about $106k operating profit before taxes, debt, and reserves. For the operating lens, track What Is The Most Important Indicator Of Success For Your Boutique Gift Shop? because traffic, conversion, and basket size decide whether cash reaches the owner.

Profit math

- $257k monthly sales base

- 81% contribution margin

- $11,975 fixed cost line

- About $88k monthly operating profit

Owner risks

- $573k launch capex

- Inventory cash delays distributions

- Rent and payroll tighten cash

- Grow repeat buyers, workshops, online, gifting

Want to see what really moves owner pay?

1

405/wkFoot Traffic

Higher weekly traffic lifts owner pay fast, and at 405 visitors a week it is the cleanest growth lever; if store visits slip, every other driver has less room to work.

2

8.0%Conversion

More buyers from the same visitors push cash flow up, and 8.0% conversion turns traffic into about 32 orders a week; weak displays or service can cut that fast.

3

86%Gross Margin

Better vendor buying keeps the 86% product gross margin high, and every point lost comes straight out of owner take-home; markdowns and slow stock are the risk.

4

$61Average Ticket

A bigger basket raises revenue without needing more visitors, and the Year 1 average ticket is about $61.02; add-on gifts help, but discounting can erase the gain.

5

$7.5K/moPayroll

Keeping payroll near $7.5K a month protects take-home, but adding staff too early can eat the sales lift before it shows up in profit.

6

$4.5KOccupancy

The $4,475 fixed overhead base, led by $3,500 rent, sets the floor for owner pay, so higher occupancy costs need stronger traffic or margin to cover them.

Boutique Gift Shop Core Six Income Drivers

Foot traffic and conversion

Foot Traffic to Buyers

Foot traffic only turns into owner income when visitors buy. With 405 weekly visitors and 8% conversion, the shop gets about 32 new buyers a week. At a $61.02 average ticket, that is about $1,977 a week, or roughly $8.6k a month before repeat sales. That is still below the $11,975 monthly cost hurdle, so conversion matters more than raw browsing.

This driver includes location, window displays, local events, tourism, reviews, and repeat customers. A shop can pay premium rent for window shoppers and still miss profit if conversion stays low. More qualified visits and better conversion raise transactions, which lifts cash for payroll, inventory, and owner pay.

Track Conversion Weekly

Track weekly visitors, conversion rate, and average ticket together. Here’s the quick math: traffic × conversion × ticket. If traffic holds at 405, every 1-point lift in conversion adds about 4 extra buyers a week, or about $247 weekly at a $61.02 ticket. That helps cover fixed costs faster, but only if the buyers are qualified.

Test window displays, event tie-ins, and review prompts, then watch whether conversion rises without hurting ticket size. If rent is high, require a clear conversion plan before signing. Browsers are fine only when enough of them become buyers.

1

Average order value

Average order value

Average order value is the dollars per sale, and here it is driven by 12 units per basket and a $5.085 weighted unit price. At that mix, Year 1 AOV is about $61.02. That matters because more dollars per ticket raise revenue without needing more foot traffic, so each buyer does more work toward rent, payroll, and owner pay.

The upside is real: a $5 lift across 5,054 annual orders adds about $25k in revenue before margin effects. The risk is pushing bundles so hard that conversion slows. Cards with gifts, candles, wrapping, seasonal bundles, premium home decor, and impulse paper goods should raise the basket, not make checkout harder.

Lift basket size

Track units per order, AOV, and markdowns by category every week. If add-on items raise basket size but discounting eats the gain, owner cash does not improve. Test small bundle rules at checkout, like a card plus gift or wrapping plus candle, and keep the offer easy to say yes to.

Use the basket mix to protect gross profit first. If each order adds one more small item at full price, the shop gets more revenue from the same traffic and more room for owner pay. If bundles slow conversion, cut them back fast and keep the best-selling add-ons on display.

2

Gross margin and vendor buying

Gross Margin and Vendor Buying

Gross margin is the cash left after product cost, freight, discounts, returns, markdowns, damaged goods, and shrinkage. In Year 1, the model uses 14% cost of goods, improving to 12% by Year 5, so small buying gains matter. On $308k sales, a 1-point margin swing moves profit by about $31k, which directly affects rent, payroll, reserves, and owner pay.

The mix matters too: Year 1 skews to ceramics 30%, jewelry 25%, paper goods 20%, and home decor 25%. If one category needs heavier markdowns or breaks more often, blended margin falls fast. Here’s the quick math: better vendor terms and less shrinkage lift gross profit before any extra traffic shows up.

Measure the Buy, Not Just the Sale

Track margin by category and by vendor, then compare landed cost to sell-through. Landed cost means wholesale price plus freight, less discounts, and after returns and damage. Keep a weekly view of buy price, markdown rate, damaged goods, and shrinkage so you can see which items fund owner draw and which ones drain cash.

Use vendor terms to protect cash and buy deeper only where sell-through is strong. One clean rule helps: if a category needs repeated markdowns, cut reorders before it cuts profit. Track the mix of ceramics, jewelry, paper goods, and home decor so the best-margin items carry more of the rent and payroll burden.

- Measure landed cost each buy.

- Review markdowns by category weekly.

- Watch damage and shrinkage separately.

- Reorder only fast-moving SKUs.

3

Rent and operating expenses

Rent and overhead

Rent and operating expenses set the monthly profit floor before the owner can take more cash home. This shop’s fixed overhead is $4,475/month, including $3,500 rent, $350 utilities, $150 insurance, $120 POS and software, $80 website, $200 cleaning, and $75 security monitoring.

With payroll, the Year 1 fixed monthly burden is $11,975. The model’s disclosed break-even target is about $148k/month at 81% contribution, so a lease that needs more sales than the location can produce will squeeze owner pay fast. Lower overhead helps profit and owner draw dollar for dollar.

Track fixed cost before signing

Measure occupancy cost, then test the lease. Start with rent plus every recurring bill tied to the store: utilities, insurance, software, website, cleaning, security, and payroll. If the monthly total rises faster than traffic or basket size, the owner draw gets crowded out.

Use a simple check: fixed costs ÷ monthly sales. If the ratio is too high, renegotiate rent, trim services, or delay extra staffing. One clean rule: every dollar saved in overhead adds a dollar to cash flow before tax.

- Track rent, utilities, and payroll monthly

- Stress-test sales against lease cost

- Review overhead before renewals

- Cut fixed costs before cutting margin

4

Inventory turnover and seasonality

Inventory Turnover and Seasonality

Inventory turnover is how fast stock turns into cash. For this shop, that matters because the launch plan puts $15k of inventory inside $573k of total launch capex, so cash is tied up before the sale happens. If holiday and local gifting seasons lift sales, good. If not, slow ceramics, seasonal decor, and dated paper goods can turn into markdowns that cut gross margin and owner draws.

The owner’s income depends on separating profit from cash flow. A strong month on paper can still leave too little cash for payroll coverage, reserves, or owner pay if reorders happen too early or dead stock builds up. One clean rule: buy for sell-through, not for shelf fill.

Track Sell-Through by Season

Watch weeks of supply, sell-through rate, and aged stock by category. The key inputs are units on hand, units sold, lead time, and markdowns. If ceramics or paper good s sit too long, slow buys before they drain cash. If holiday demand is strong, place orders earlier, but match them to the season so stock clears before it ages.

- Measure stock age weekly.

- Set reorder points from lead time.

- Track markdowns by category.

- Reserve cash for payroll and draws.

What this estimate hides: cash leaves before revenue lands, so the right buying pace can protect owner income even when sales are flat. Faster turnover means less dead stock and more cash available for draws and reserves.

5

Staffing and owner involvement

Staffing and owner involvement

Payroll starts at $90,000 with a $60,000 owner-manager and a $30,000 retail associate. That cost supports coverage, but it also sets the cash hurdle the shop must clear before the owner can pay themselves more. The upside is control: owner-run coverage keeps early profit intact, but it also limits store hours, merchandising, workshops, online orders, and corporate gifting.

Here’s the quick math: adding staff helps only if it lifts sales or frees the owner into higher-value work. A second associate in Year 2 and marketing help in Year 3 raise payroll before demand proves out, so the risk is adding fixed cost too soon. What this hides is simple: labor is not a win on its own unless traffic, conversion, and ticket size rise with it.

Track payroll against sales growth

Measure sales per labor dollar, owner hours on the floor, and revenue from workshops, online orders, and corporate gifting. If extra labor does not raise those lines, it is just overhead. Tie each hire to a target: longer hours, better display work, or more order handling.

- Track hourly sales by shift

- Test coverage before hiring

- Review payroll monthly

- Link hires to new revenue

Use a simple test: if the new role does not create enough gross profit to cover its pay, keep the owner in the role longer. That protects cash flow and keeps more profit available for owner draw. If it does work, the payoff is better service, more sales, and less founder burnout.

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Traffic, ticket size, and repeat buying drive owner income fast in this shop. Year 2 and Year 3 are aggressive because repeat-customer lifetime assumptions compound quickly.

| Scenario | Low CaseDownside case | Base CaseAggressive case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower owner-income path. | This is the modeled owner-income path. | This is the stronger owner-income path. |

| Typical setup | Year 1 traffic converts at 8.0%, supports about $308k revenue, a $61.02 average ticket, about 86% product gross margin, and roughly $90k payroll. | Year 2 traffic converts at 9.5%, supports about $776k revenue, a $70.25 average ticket, about 86.5% product gross margin, and roughly $105k payroll. | Year 3 traffic converts at 11.0%, supports about $1.745M revenue, a $79.42 average ticket, about 87% product gross margin, and roughly $132.5k payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $100k - $110kIncome floor | $450k - $500kCore case | $1.2M - $1.3MAggressive upside |

| Best fit | Use this to stress test a slower launch with lighter traffic and a modest repeat base. | Use this as the main planning case if traffic grows and repeat buying compounds on schedule. | Use this to test upside if repeat customers stay active longer and the shop scales without margin drift. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Boutique Gift Shop Porter's Five Forces Analysis

- Boutique Gift Shop BCG Matrix

- Boutique Gift Shop Business Model Canvas

- 7 Core Financial KPIs for Your Boutique Gift Shop

- Boutique Gift Shop Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Boutique Gift Shop Profitability

- How to Manage the Monthly Running Costs of a Boutique Gift Shop

- How Much Does It Cost To Open A Boutique Gift Shop: $648k Plan

- Boutique Gift Shop Financial Model Template in Excel

- How to Open a Boutique Gift Shop: 3-6 Month Launch Roadmap

- How to Write a Boutique Gift Shop Business Plan in 7 Steps

- Boutique Gift Shop Marketing Mix

- Boutique Gift Shop Marketing Plan

- Boutique Gift Shop Business Proposal

- Boutique Gift Shop PESTEL Analysis

- Boutique Gift Shop Pitch Deck Example Editable PPTX

- Boutique Gift Shop Business SWOT Analysis

- Boutique Gift Shop Value Proposition Canvas

Frequently Asked Questions

Under the researched Year 1 assumptions, the owner has a $60,000 salary line plus about $106,000 of operating profit before taxes, debt, and extra inventory reserves That equals potential cash capacity, not a guaranteed draw The store must hit about $308,000 in sales and hold an 81% contribution margin after product cost, processing, and packaging