Owner income$90K to $4.13M

Owner income$90K to $4.13MHow Much Does A Branding Agency Owner Make? $90K–$413M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$90K to $4.13M  Net margin20%

Net margin20% Revenue for target pay$130K per $100K

Revenue for target pay$130K per $100K Business difficultyHard

Business difficultyHard

You’re planning owner pay before the agency has steady project flow, so separate revenue, gross margin, EBITDA, reserves, and owner take-home This five-year US branding agency model shows EBITDA rising from $90K in Year 1 to $413M in Year 5, before taxes, debt payments, and owner distribution policy

Owner income$90K to $4.13MNet margin20%Revenue for target pay$130K per $100KBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay for a branding agency.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

Want to see the full income forecast?

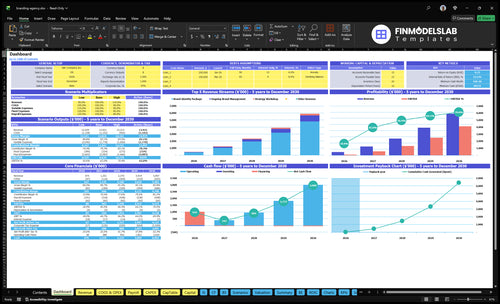

The screenshot shows revenue, EBITDA, Month 6 breakeven, 12-month payback, and $848K minimum cash in Month 2; open the Branding Agency Financial Model Template to test owner income assumptions.

Owner-income model highlights

- Owner pay scenario tests

- Revenue, margin, staffing

- Pricing, CAC, reserves

How much can a small branding agency owner make?

A small Branding Agency owner can make about $90K in Year 1 EBITDA, rising to $563K in Year 2 and $4.133M by Year 5 in the provided model; for owner-level success tracking, start with What Is The Most Critical Measure Of Success For Your Branding Agency?. That’s not the same as take-home pay, because taxes, cash reserves, debt, and whether the owner also fills a paid production role all change the final check.

Owner Earnings

- Year 1 EBITDA: $90K

- Year 2 EBITDA: $563K

- Year 5 EBITDA: $4.133M

- Best lens: owner role, not salary averages

Cost Drivers

- Year 1 payroll: $165K

- Year 1 overhead: $648K

- Marketing budget: $20K

- Year 5 payroll: $460K

Does scaling a branding agency increase owner income?

Yes — a Branding Agency can lift owner income, but only when pipeline, pricing, and utilization rise faster than payroll and management drag. In the model, payroll grows from $165K in Year 1 to $460K in Year 5, EBITDA grows from $90K to $4133M, breakeven lands in Month 6, payback is 12 months, and minimum cash need peaks at $848K in Month 2.

Income upside

- Pipeline must keep filling.

- Pricing has to hold up.

- Utilization must stay high.

- Hiring adds design and PM capacity.

Main risks

- Lower utilization cuts margin fast.

- Slower closes delay cash payback.

- Owner time shifts to management.

- Month 2 cash need hits $848K.

Are branding agencies profitable?

The Branding Agency model can be profitable, but only if delivery labor stays tight and utilization stays high. The model shows gross margin after freelance contractor fees and media or font licenses rising from 900% in Year 1 to 928% in Year 5, while EBITDA rises from $90K to $4.133M as scale absorbs $648K of fixed overhead and payroll growth from $165K to $460K; before you hire, check What Is The Estimated Cost To Open And Launch Your Branding Agency?.

Profit drivers

- 900% to 928% gross margin

- 770% to 828% contribution

- $90K to $4.133M EBITDA

- Scale absorbs $648K overhead

Profit drains

- Freelance contractor fees hit margin

- Media or font licenses add cost

- Payroll grows from $165K to $460K

- Strategist, design, admin, sales, travel

What moves branding agency owner income most?

1

$5.25K-$8.17KProject Value

The identity package jumps from $5,250 in Year 1 to $8,170 in Year 5, so every sale brings in more owner cash; watch scope creep because it can erase the lift.

2

25%-65%Retainers

Ongoing brand management grows from 25% to 65% of mix, and that recurring work steadies cash while reducing the need to keep selling new one-off projects.

3

$1.2K-$1.0KPipeline CAC

Customer acquisition cost falls from $1,200 to $1,000, so the same marketing spend should buy more qualified leads and more booked work.

4

0.5-1.0FTELabor Mix

The team adds senior, junior, and support labor over time, and the mix between those roles decides how much revenue turns into take-home profit.

5

30-38hUtilization

Brand identity delivery rises from 30 to 38 billable hours, so tighter scheduling and cleaner scope control keep the team from losing margin.

6

$5.4K/moCash Discipline

Fixed overhead runs about $5.4K a month, but the cash low point hits $848K in Month 2, so reserve control matters even when revenue is growing.

Branding Agency Core Six Income Drivers

Average Project Value

Average Project Value

When project fees move up, revenue rises per client without adding the same number of clients. An identity package at 30 hours × $175 = $5,250 in Year 1 and 38 hours × $215 = $8,170 in Year 5 adds $2,920, or about 56%, per deal. Strategy workshops run 12 hours at $2,400 to $3,120, so pricing has to cover strategist time, design time, sales time, and revisions.

Price by scope, not just output

Track average fee by project type, then compare it with delivery hours and revision load. If low-scope logo work can’t cover payroll and pre-sales time, it pulls down gross margin and leaves less for owner pay. Set pricing around scope, client type, positioning, and delivery cost, and use a floor price before you quote.

- Measure fee per project.

- Track hours by service.

- Reject underpriced logo-only work.

- Test workshop pricing first.

1

Qualified Sales Pipeline

Qualified Sales Pipeline

When discovery calls and proposals dry up, owner income drops fast because there’s less work sold into the schedule. In Year 1, a $20K marketing budget and $1,200 CAC imply about 17 acquired clients ($20,000 / $1,200), while Year 5’s $95K budget and $1,000 CAC imply about 95 clients. The real issue is fit: weak leads waste selling time and still leave delivery gaps.

This driver includes lead quality, discovery calls, proposal volume, close rate, and how many deals turn into retainers. More qualified leads improve utilization (paid time as a share of available time), reduce idle weeks, and support steadier cash flow. Low-fit leads can look busy, but if they don’t cover strategist time, design time, and revisions, they drag profit and make owner pay less reliable.

Qualify Before You Quote

Track qualified leads by source, then watch discovery-to-proposal and proposal-to-close rates each week. Count only prospects with enough budget, a decision maker, and a scope that can cover delivery cost. If marketing spend rises from $20K to $95K but CAC stays near $1,000–$1,200, the win comes from better fit, not just more volume.

Set a hard gate before proposals go out: budget, scope, and retainer potential. If a channel brings calls but not signed work, cut it fast. Here’s the quick math: more qualified wins mean fewer project gaps, better payroll absorption, and more cash left for overhead and the owner draw. One clean rule helps: no fit, no proposal.

2

Billable Capacity And Utilization

Billable Capacity And Utilization

Utilization is the share of available team time spent on paid client work. Here, billable hours rise from 30 to 38 for identity packages and from 15 to 23 for ongoing management, while workshops stay at 12. That can lift revenue per staff hour and improve payroll absorption, but only if review time and revisions stay controlled.

The owner feels this in take-home pay through gross profit and cash flow. Billable hours ÷ available hours is the key test. Higher utilization helps when the team stays sharp, but overbooking can slow delivery, hurt quality, and reduce referrals and repeat work, which cuts future sales.

Keep billable time clean

Track billable hours by service line, not just total utilization. Separate paid work, internal admin, client revisions, and review time so the team can see where hours leak out. If identity packages move toward 38 hours, the scope, approvals, and handoffs need to be set before pricing changes.

Protect margin by capping revision rounds and checking capacity weekly. Ongoing management is more sensitive because it rises from 15 to 23 hours, so retainers need clear turnaround rules. That keeps delivery stable, improves payroll coverage, and helps the owner pay themselves from steadier profit.

3

Delivery Labor Mix

Delivery Labor Mix

Delivery labor mix is the split between freelancers, employees, owner time, and license costs that gets the work out the door. In Year 1, contractor fees take 80% of revenue and premium stock media and font licenses take 20%; by Year 5, those fall to 60% and 12%, while employee payroll rises from $165K to $460K. That mix decides how much revenue is left for overhead and owner pay.

The owner’s take-home improves when the mix matches real booked work, not hoped-for work. Owner-delivered labor can lift early margin, but it also caps sales, strategy, and management time. The big risk is hiring ahead of signed work, because payroll starts first and cash flow feels it fast.

Hire Only Against Signed Work

Track delivery labor as a share of revenue, then compare it with the planned shift from 80% to 60% for contractor fees, 20% to 12% for licenses, and $165K to $460K for payroll. Build forecasts from signed projects, billable hours, and utilization, not pipeline hope. One clean rule: do not add payroll until the work is booked.

- Map hours by role each month.

- Cap hires to backlog.

- Review margin before headcount.

- Protect owner time for sales.

If the owner stays buried in delivery, project volume and retainer growth stall, and the business can look busy while pay stays thin. The best mix keeps production covered, preserves cash, and still leaves time for pricing, selling, and managing quality.

4

Retainer Revenue

Recurring Branding Retainers

When project revenue swings, retainers smooth cash flow between rebrands. Real retainer work includes brand management, creative direction, messaging support, and campaign alignment. At 15 hours × $150 = $2,250 per ongoing account in Year 1 and 23 hours × $190 = $4,370 in Year 5, one client can cover more payroll and owner pay if scope stays tight. Over-servicing turns recurring revenue into a discount.

Price the Hours, Not the Promise

Track active accounts, sold hours, actual hours, and renewal rate each month. If actual time runs above the scoped hours, raise the fee or cut deliverables. Don’t call it subscription revenue unless the project pipeline can refill gaps; a project-based core with thin retainers still leaves cash flow lumpy.

- Measure hours sold vs. hours used.

- Set a monthly renewal target.

- Bill overages before margin leaks.

5

Overhead And Cash Reserves

Overhead and Cash Reserves

$54K per month in fixed overhead, plus rent, utilities, software, professional services, insurance, supplies, and sales tools, means cash gets used before the owner gets paid. That is $648K a year just to stay open. One line: EBITDA can look fine, but cash still leaves the business first.

The reserve plan matters because minimum cash need hits $848K in Month 2, and the annual marketing budget rises from $20K to $95K. That extra $75K supports growth, but it lowers near-term take-home income until collections and margin catch up.

Track Cash Before Draws

Measure cash runway against fixed overhead, not just profit. $848K equals about 15.7 months of the current $54K monthly base, so owner pay should stay tight until the reserve floor is safe. The key is simple: cover overhead first, then pay the owner.

- Track monthly fixed cost burn.

- Set a reserve floor before draws.

- Review marketing spend against cash.

For this model, the risk is taking distributions too early while overhead stays heavy. Keep owner draws tied to cash after the reserve target, and only raise pay when recurring revenue can absorb the fixed cost load.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income grows as the agency moves from founder-led delivery to a fuller team and more recurring work. The model breaks even in Month 6, pays back in 12 months, and needs $848K minimum cash.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is a lean owner-income path built on Year 1 scale and modest EBITDA. | This is the modeled path where owner income scales with a balanced service mix and stronger EBITDA. | This is the stronger earnings path where recurring work and pricing power push owner income higher. |

| Typical setup | The founder stays hands-on, work skews to brand identity projects, and the team stays light with limited recurring management. | Year 2 to Year 3 adds more recurring brand management, higher rates, and enough support staff to keep delivery moving. | Year 4 to Year 5 runs with a fuller team, more ongoing brand management, and higher hourly rates across most work. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $90KLow Case | $563K - $1.34MBase Case | $2.51M - $4.13MHigh Case |

| Best fit | Use this to test early ramp, slower closes, and a smaller client mix. | Use this as the core planning case for steady growth and repeat clients. | Use this to stress-test upside if recurring revenue and pricing hold as the team fills out. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; taxes, reserves, debt service, and owner draws are excluded.

Related Products

- Branding Agency Porter's Five Forces Analysis

- Branding Agency BCG Matrix

- Branding Agency Business Model Canvas

- 7 Financial KPIs to Scale Your Branding Agency

- Branding Agency Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Branding Agency Profitability

- How to Run a Branding Agency: Essential Monthly Operating Costs

- Branding Agency Startup Costs: $475k CAPEX, $848k Cash

- Branding Agency Financial Model Template in Excel

- How To Open A Branding Agency In 4 To 10 Weeks With First Clients

- How to Write a Branding Agency Business Plan in 7 Steps

- Branding Agency Marketing Mix

- Branding Agency Marketing Plan

- Branding Agency Business Proposal

- Branding Agency PESTEL Analysis

- Branding Agency Pitch Deck Example Editable PPTX

- Branding Agency Business SWOT Analysis

- Branding Agency Value Proposition Canvas

Frequently Asked Questions

Under these assumptions, the pre-tax profit pool is $90K in Year 1, $563K in Year 2, and $413M in Year 5 That is EBITDA, not guaranteed take-home Owner pay depends on whether the founder fills the $120K Lead Brand Strategist role, how much cash is reserved, and what taxes or debt apply