Bridge Loan Financing Startup Costs For A $20M Year 1 Lending Plan

Key Takeaways

- Legal setup needs one-time and recurring compliance budgets.

- Year 1 funding need is $195M, not CAPEX.

- Tech costs mix implementation, SaaS, and servicing planning.

- Payroll starts before launch, with salaries near $370K.

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates the upfront capitalized startup assets only for a bridge loan financing service, including office buildout, equipment, software setup, security, website, and contingency.

Excludes non-CAPEX This calculator covers only capitalized startup assets and setup work. It excludes licensing fees, legal retainers, payroll runway, working capital, loan principal, warehouse lines, private notes, reserves, deposits, inventory, debt service, and other operating costs.

Where are CAPEX and funding shown?

This screenshot shows the Bridge Loan Financing Service Financial Model Template CAPEX tab. It should split startup costs, launch timing, working capital, lending capital, revenue timing, servicing costs, and depreciation or amortization. Open it and test assumptions before raising capital.

Screenshot highlights

- CAPEX and startup costs

- Revenue timing and servicing

- Funding draw assumptions

- $200M Year 1 check

- $35k monthly costs

- $370k salaries yearly

- Gross and liability interest

How Do You Plan Funding For A Bridge Loan Financing Service?

Plan funding for a Bridge Loan Financing Service around origination volume, spread, and draw timing, not just total capital raised. Here’s the quick math: Year 1 loan interest on $50M residential bridge at 105%, $80M commercial bridge at 110%, $40M fix-and-flip at 120%, $20M SME acquisition at 130%, and $10M transactional fund at 140% totals about $228.5M before credit costs and operating expenses. Against $195M of interest-bearing liabilities and about $13.75M of modeled interest cost, plus $11M of other earning assets producing about $38,900, the funding plan only works if runway stays tight and capital is in place before loan draws peak.

Origination mix

- $50M residential bridge at 105%

- $80M commercial bridge at 110%

- $40M fix-and-flip at 120%

- $20M SME acquisition and $10M fund

Funding controls

- Match funding to draw schedules

- Hold $195M liability capacity

- Model about $13.75M interest cost

- Keep other earning assets at $11M

How Much Money Do You Need To Start A Bridge Loan Company?

You need two layers to start a Bridge Loan Financing Service: cash to operate, plus lending capital or credit capacity to originate loans; for the researched Year 1 model, that means planning around $200M in originations, not treating loan principal as startup expense. For the business-plan logic, see How To Write A Business Plan For Bridge Loan Financing Service?; here’s the quick math: Residential Bridge $50M, Commercial Bridge $80M, Fix and Flip $40M, SME Acquisition $20M, and Transactional Fund $10M. Your real constraint is liquidity, draw timing, covenant headroom, and cash runway before loans repay.

Funding Need

- Plan around $195M Year 1 liabilities

- Use $100M warehouse lines

- Add $50M private notes

- Include $30M family office debt

Operating Base

- Reserve $35,000 monthly fixed costs

- Budget $420,000 annual fixed overhead

- Fund at least $370,000 leadership payroll

- Separate startup cash from loan principal

What Hidden Costs Come With Starting A Bridge Loan Financing Service?

The hidden costs in a Bridge Loan Financing Service are the operating items that hit before loans generate steady income: payroll runway, legal revisions, borrower due diligence, appraisal review, title and lien checks, insurance, servicing setup, audit and accounting, tax support, cybersecurity, and interest carry. For the model, use $2,500 a month for data and credit reporting, $4,500 for loan origination software SaaS, and $5,000 for professional liability insurance; see How To Write A Business Plan For Bridge Loan Financing Service? for the planning structure. Keep loan loss reserves and funding reserves as liquidity items, not CAPEX, because they protect cash but do not build the platform.

Monthly overhead

- $2,500 data and credit reporting

- $4,500 loan software SaaS

- $5,000 liability insurance

- 25 Year 1 servicing fee input

Cash risks

- 100 Year 1 broker commission input

- Budget legal revisions early

- Plan bad debt reserves separately

- Cover interest carry before scale

Calculate Fuding Needs

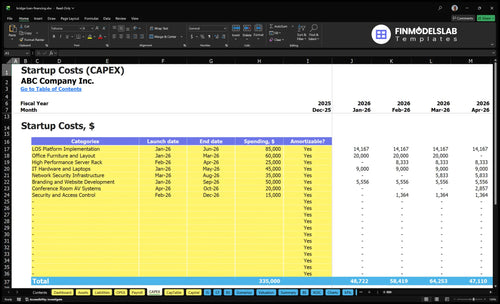

Startup cost summary

Startup cost summary for a bridge loan lender, covering setup assets and the non-CAPEX cash reserve needed to open.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Loan Origination Software Implementation | $85,000 | LOS build and configuration | Yes |

| Office Furniture and Layout | $60,000 | Office fit-out and workspace build | Yes |

| IT Hardware and Laptops | $45,000 | Workstations and secure devices | Yes |

| Network Security Infrastructure | $35,000 | Secure network and access control | Yes |

| Branding and Website Development | $50,000 | Launch site and brand build | Yes |

| Operating Reserve | $47,582 | Month 12 cash floor from fixed costs and ramp losses | No |

Bridge Loan Financing Service Core Five Startup Costs

Licensing And Legal Setup Startup Expense

Licensing Scope

Costs move with state footprint, borrower type, collateral type, and loan purpose. Budget separate line items for entity formation, lender licensing research, state applications, compliance manuals, loan agreements, borrower disclosures, privacy policies, servicing language, regulatory filings, counsel review, and document version control. Application fees and counsel fees sit outside recurring retainers.

Startup Budget

Model one-time legal setup separately from recurring compliance. Use $8,000/month for the legal retainer and $3,000/month for compliance monitoring starting in Month 1. Add a reserve for document revisions, re-filings, and counsel redlines so launch cash doesn’t get understated.

Control the Spend

Lock the licensing map before final drafts, then reuse controlled templates across loans that share the same footprint. Keep version control on every agreement and disclosure, with one owner for updates. The common mistake is bundling setup and monitoring into one budget line, which hides cash needs and makes month-one spend hard to track.

Cost Driver

A multi-state lender with business-purpose loans and different collateral types will spend more than a narrow, single-state platform. The clean model is setup cost, monthly compliance, and revision contingency. Treat regulatory filings, outside counsel, and document changes as separate cash outlays so the legal budget stays readable.

Loan Capital And Liquidity Startup Expense

Total Need

This is total funding need, not CAPEX or a normal startup expense. It covers cash equity, investor funds, warehouse setup, private notes, family office debt, institutional credit, mezzanine capital, minimum liquidity, interest reserves, concentration limits, and pipeline capacity. For a bridge lender, the balance sheet is the product, so this belongs outside the CAPEX calculator.

Build The Stack

Use funding sources, advance rates, and loan volume to size the stack. The researched Year 1 target is $195M, anchored by $100M warehouse lines at 65%, $50M private notes at 80%, $30M family office debt at 75%, $10M institutional credit at 55%, and $500,000 mezzanine capital at 90%. Keep application fees and counsel fees separate.

- Borrowing base and advance rate

- Reserve months and interest carry

- Borrower concentration caps

- Monthly origination pipeline

Protect Liquidity

$195M of funding against $200M of Year 1 loan volume leaves little slack. Cut risk by staging capital to match closings, not forecasts, and by tracking minimum liquidity, interest reserves, and concentration limits every month. The mistake is counting undrawn capacity as if it were cash.

Keep It Separate

Put funding need in its own model line, then stress test draw timing and repayment lag. If the pipeline slows or a few borrowers cluster too hard, liquidity gets tight fast. That is why this spend needs committed capital, clear reserves, and monthly monitoring from day one.

Technology And Underwriting Systems Startup Expense

Recurring tech stack

Technology spend splits into recurring SaaS and one-time setup. The base recurring stack is $4,500/month for loan origination software plus $2,500/month for data and credit reporting, or $84,000/year before seats and add-ons. That covers customer relationship management (CRM), borrower portal, e-signature, servicing, and underwriting tools; implementation, cybersecurity setup, and document retention sit outside this run rate.

What to budget

Price the system from user seats, implementation fees, and the number of modules. Ask for quotes on setup, underwriting templates, portal and e-signature, servicing, credit and background tools, and valuation data. Then add servicing and collection fees tied to the 25-loan Year 1 assumption. Keep one-time build costs separate from monthly SaaS.

- Count active users, not headcount.

- Quote setup separately.

- Model servicing fees monthly.

Keep it lean

Start lean: buy only the modules you need to close and service the first loans. The usual waste is paying for extra seats, full automation, or duplicate data feeds before volume exists. Phase the rollout so implementation, training, and process cleanup happen once. That keeps the budget tight without weakening controls, borrower experience, or underwriting quality.

- Trim seats before trimming controls.

- Delay nonessential integrations.

- Review renewal pricing early.

Security and retention

Security is part of launch, not a later upgrade. Budget for cybersecurity, secure document storage, backups, and access controls so borrower files and underwriting notes stay protected. The calculator should ask for retention rules, admin permissions, and disaster recovery needs; those choices drive setup cost and can change storage and compliance spend.

Staffing And Pre-Opening Payroll Startup Expense

Base burn

Pre-opening payroll can run fast if you hire before licenses or funded loans. The named salary base is $370,000 a year, or about $30,800 a month, before payroll taxes and benefits. That’s the core burn for a CEO and Managing Director plus Head of Underwriting, so timing matters more than title count.

Staff mix

This bucket covers the launch team: CEO and Managing Director, Head of Underwriting, loan originators, underwriters, processors, servicing support, admin support, recruiting fees, onboarding, training, payroll taxes, benefits, and outsourced CFO or accounting support. Estimate it from headcount × months × salary, then add hiring costs and tax load.

- Map hires to license dates.

- Add taxes and benefits.

- Keep CFO support outsourced.

Hiring gate

If hiring starts before licenses, before first close, or only after committed credit capacity changes the budget a lot. The cleanest check is simple: don’t lock in full payroll until the legal path and funding path are both real. Otherwise you turn a launch expense into extra runway burn.

- License first, if possible.

- First close next.

- Committed credit capacity last.

Cash plan

Separate pre-opening payroll from working capital runway so you don’t double count cash. Use a monthly hiring plan, then add recruiter fees, onboarding, training, payroll taxes, and benefits on top of salary. A slow ramp is cheaper than a full bench sitting idle, and it keeps launch cash tied to actual close dates.

Office Insurance Marketing And Launch Operations Startup Expense

Launch Space

This line covers office rent or a virtual office, secure IT equipment, and launch-ready insurance. The fixed anchors are $12,000 monthly rent and $5,000 monthly professional liability insurance, so the launch budget must separate one-time setup from recurring overhead. Add cyber insurance, website, brand assets, and CRM setup before first borrower contact.

Budget Split

Build a separate launch budget for website, brand assets, borrower acquisition, broker outreach, referral marketing, launch materials, and CRM setup. Use quotes, months of coverage, and device count to price it. Keep this out of the monthly run rate so you can see the true opening cash need beside the $12,000 rent and $5,000 insurance anchors.

- Price each vendor by quote.

- Count only launch months.

- Separate setup from SaaS.

Acquire Leads

Don’t assume borrower acquisition is free. Plan around commercial brokers, real estate investors, business acquisition advisors, and repeat referrals, then track the stated broker commission assumption of 100 in Year 1, stepping down to 80 by Year 5. Pay for channels that close loans, or marketing will outrun funded volume.

- Pay on funded deals.

- Track source in CRM.

- Cut weak channels fast.

Channel Mix

Keep CRM setup tied to source tracking, so you can see which channel produces funded loans, not just leads. That lets you protect margin, since launch spend stays separate from monthly marketing and you only scale the channels that keep bringing repeat business.

Compare 3 Startup Cost Scenarios

Scenario Table

Scaling this lender changes cost fast because each step adds licensing, staff, systems, and capital. Lean stays local, Base fits a regional operator, and Full needs multi-state scale.

| Scenario | Lean LaunchBest for relationship lender | Base LaunchBest for regional operator | Full LaunchBest for institutional platform |

|---|---|---|---|

| Launch model | Stay narrow and local with fewer products and lower capital needs than the base model. | Run a regional lender around the Year 1 model, with about $20M loan volume and $19.5M of interest-bearing liabilities. | Scale toward the Year 5 model, with about $295M loan volume and $323M of interest-bearing liabilities. |

| Typical setup | Use a small team, one office, and a simple loan origination stack. | Keep a dedicated office, standard loan software, and a team sized for $35k monthly fixed costs and $370k in named leadership payroll. | Use a larger office, broader team, deeper compliance, and more capital partners. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | Lower funding bandLower capital needs | Mid funding bandMid capital needs | Higher funding bandHigher capital needs |

| Best fit | Best for owners who want a local, relationship-led lender with a narrow product set and lighter compliance load. | Best for operators building a regional bridge lender with a standard team, office, and control stack. | Best for sponsors building a multi-state platform that needs heavier licensing, more staff, and larger capital lines. |

Planning note: Scenario ranges are researched planning assumptions from the model, not exact vendor quotes or loan quotes.

Related Products

- Bridge Loan Financing Service Porter's Five Forces Analysis

- Bridge Loan Financing Service BCG Matrix

- Bridge Loan Financing Service Business Model Canvas

- What 5 KPI Metrics For Bridge Loan Financing Service?

- Bridge Loan Financing Service Business Plan Template in Pre-Written Word

- How Increase Bridge Loan Financing Service Profits?

- What Are Operating Costs For Bridge Loan Financing Service?

- Bridge Loan Financial Model Template in Excel

- How Much Can A Bridge Loan Financing Owner Make On $20M In Loans?

- How To Start A Bridge Loan Financing Service In 3 To 9 Months

- How To Write A Business Plan For Bridge Loan Financing Service?

- Bridge Loan Financing Service Marketing Mix

- Bridge Loan Financing Service Marketing Plan

- Bridge Loan Financing Service Business Proposal

- Bridge Loan Financing Service PESTEL Analysis

- Bridge Loan Financing Service Pitch Deck Example Editable PPTX

- Bridge Loan Financing Service Business SWOT Analysis

- Bridge Loan Financing Service Value Proposition Canvas

Frequently Asked Questions

Loan capital is the main funding need, but it is not a normal startup expense The researched model assumes $200M in Year 1 loans and $195M in interest-bearing liabilities Setup costs cover the platform, people, compliance, and systems, while loan principal, warehouse lines, private notes, and reserves belong in liquidity planning