Owner income$220k

Owner income$220kBrownfield Redevelopment Owner Income: 39-Month Payback Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$220k  Net marginN/A

Net marginN/A Revenue for target payN/A

Revenue for target payN/A Business difficultyHard

Business difficultyHard

You’re tying owner income to project exits, cleanup risk, financing, and reserves, not a simple salary This United States brownfield redevelopment services model covers 7 projects over 60 months, with payback in Month 39 and a cash trough of -$10627M

Owner income$220kNet marginN/ARevenue for target payN/ABusiness difficultyHardWant to test your brownfield owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, labor, overhead, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It does not model taxes, legal liability outcomes, or grant certainty.

Want the brownfield financial model view?

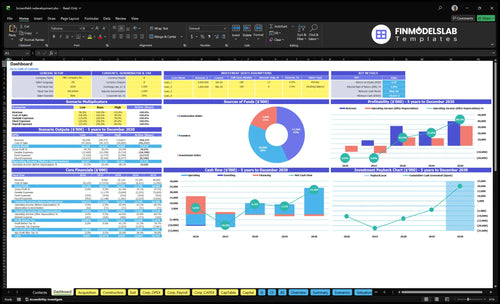

The Brownfield Redevelopment Services Financial Model Template is a planning dashboard that links project assumptions to owner take-home. It covers dashboard, acquisition schedule, construction budget, sale timing, variable expenses, fixed overhead, payroll, capex, cash flow, scenarios, and owner distributions.

Owner-income model highlights

- Owner distributions drive take-home

- EBITDA tracks by year

- Scenarios test cash timing

What costs reduce brownfield redevelopment owner income?

For Brownfield Redevelopment Services, owner income gets cut first by environmental due diligence and cleanup, especially Phase I Environmental Site Assessment, Phase II sampling, remediation scope, and disposal tied to What Are Operating Costs For Brownfield Redevelopment Services?. The biggest drag is cash flow: $46,200 a month of fixed overhead before payroll, plus $825,000 in Year 1 payroll rising to $2.035M by Year 5. Remediation contingency starts at 100% in Year 1 and only steps down to 50% by Year 5, so don’t minimize environmental liability.

Biggest income drains

- Phase I ESA delays close

- Phase II sampling adds cost

- Remediation scope can expand fast

- Disposal and vapor mitigation hit margins

Carry and risk costs

- Groundwater issues raise spend

- Insurance and legal fees stack up

- Permitting slows revenue timing

- Interest carry burns project cash

How does a brownfield redevelopment business make money?

Brownfield Redevelopment Services makes money from development fees, project management fees, the acquisition-to-exit spread, sale proceeds, lease income, incentive reimbursements, and carried interest. The owner’s pay is separate from company revenue, and if the owner serves as Managing Director, that salary can be $220,000, plus distributions after reserves and investor obligations.

Company revenue

- Development fees fund upfront work

- Project management fees pay for oversight

- Sale proceeds drive exit profit

- Lease income adds recurring cash

Owner pay and model fields

- $220,000 Managing Director salary if applicable

- Distributions come after reserves

- Investor obligations get paid first

- Track fees, grants, debt service, reinvestment

How many brownfield projects does an owner need to make a living?

There isn’t a fixed number: for Brownfield Redevelopment Services, it depends on whether the owner pays themself through salary, distributions, or both. In this plan, 7 projects over 60 months create the path, with first breakeven in Month 22 and payback in Month 39; that’s why staggered exits matter. Construction runs 10 to 20 months, and sale timing can stretch to Month 60, so income stays lumpy.

What sets the pace

- 7 projects over 60 months

- Breakeven starts in Month 22

- Payback lands in Month 39

- Sales can extend to Month 60

What improves cash flow

- Build a deeper project pipeline

- Keep capital access ready

- Use specialized partners

- Maintain municipal relationships

Which six levers move owner income most?

1

$12.85MAcquisition Basis

Lower entry cost sets the margin ceiling and cuts the equity check before cleanup starts.

2

$28.9MRemediation Control

Keeping cleanup spend near plan protects cash and stops margin bleed on each site.

3

$10.6MFinancing Mix

A leaner funding stack lowers the cash trough and reduces how much owner cash must go in.

4

Month 39Exit Value

Sale timing sets how fast owners get cash back, and the model reaches payback in Month 39.

5

$115K/moOverhead Discipline

Holding fixed burn near this level preserves salary coverage until the first assets close.

6

Month 22Incentives

Breakeven lands in Month 22, so any credits or abatements that land early improve take-home.

Brownfield Redevelopment Services Core Six Income Drivers

Acquisition Basis

Acquisition Basis

Acquisition basis has a high income impact because the purchase price sets the profit ceiling before cleanup and exit. On the disclosed $1,285M of owned acquisition costs across 5 sites, the average basis is about $257M per site, so a weak buy can squeeze owner distributions before remediation even starts.

Here’s the quick math: every extra dollar paid for contaminated property must come back through lower cleanup cost, higher sale value, incentives, or cheaper financing. Buy at a discount that covers contamination risk, and you protect margin. Overpay, and the project may still work, but the owner’s take-home gets thinner fast.

Buy with cleanup room

Track basis against as-is value, the site’s value before cleanup, plus probable remediation, carrying cost, and exit value before you close. Make the buy decision on risk-adjusted return, not just land price. If the discount does not cover contamination uncertainty, the seller may be taking profit that should have stayed in the project.

Use a simple gate on each site: required discount, expected cleanup range, and recovery sources. Keep federal, state, and municipal incentives separate from price so you do not double count them. One clean rule: if the basis leaves no room for overruns, owner pay is the first thing to suffer.

- Model basis by site, not portfolio.

- Stress test overpayment by dollar.

- Document recovery sources before closing.

1

Remediation Cost Control

Remediation Cost Control

This driver is the full cleanup bill: disposal, vapor mitigation, groundwater work, monitoring, and change orders. If the scope is off, cash gets used up faster, the sale or lease takes longer, and the owner’s promote and distributions shrink.

Use the professional environmental assessment as the base case. The reserve model uses 100% in Year 1, 80% in Year 2, 70% in Year 3, 60% in Year 4, and 50% in Year 5, so early overruns hurt the most. One bad estimate can turn a good project into delayed payback and thin take-home cash.

Control Cleanup Overruns

Track each cleanup line item against the assessment and rebid when field facts change. The key question is simple: are actual remediation costs staying inside the reserve curve, or are they eating the cash needed for owner distributions?

- Test disposal and haul-out costs.

- Separate vapor and groundwater scope.

- Watch monitoring and change orders.

- Reforecast when bids move.

Stress-test the model for higher cleanup scope before closing. If the estimate misses contamination depth or cleanup duration, cash needs rise fast and the project can look profitable on paper while the owner waits longer to get paid.

2

Incentive Capture

Incentive Capture

Incentive capture has a medium-to-high income impact because grants, tax credits, and public financing can reduce equity needs and make a site financeable. For the owner, that can mean less cash tied up before sale and a better chance of taking money out sooner, but only if the award is real and eligible.

Model federal, state, and municipal support separately. Track expected award, timing, reimbursement lag, matching funds, and disallowance risk. A delayed or denied award does not just cut proceeds; it can widen the cash trough and reduce or delay owner distributions.

Track Each Award Source

Build the model from confirmed eligibility, not hope. Use one line per incentive source and stress test a zero-award case so you can see how much equity the project really needs without support. That tells you whether the deal still protects owner income if one program slips.

- Separate federal, state, municipal lines

- Log award date and reimbursement lag

- Test matching funds before closing

- Flag disallowance risk by site

- Reforecast equity after each award

The real income gain is not the headline award. It is lower capital strain, a better cash trough, and a higher chance of owner distributions. If reimbursement lands after cleanup spend, the project still needs cash first, so timing matters as much as the dollar amount.

3

Exit Value

Exit Value

Exit value is the price at sale or the value of a hold, and it drives the owner’s payout after cleanup. In this model, the real test is whether the site can sell, lease, or reuse at a price that beats remediation and carry. A Month 22 exit usually frees cash sooner; a delayed Month 60 exit can leave EBITDA (earnings before interest, taxes, depreciation, and amortization) positive but owner cash flow weak.

What matters most is market demand, zoning and permit rights (entitlements), tenant interest, and cleanup completion. Compare sale, lease-up, mixed-use reuse, industrial reuse, and hold value side by side. If cleanup and approvals are not finished, the exit price tends to fall faster than the remaining cleanup cost, and that cuts distributable profit.

Track exit timing, not just price

Model exit value from the bottom up. Use the expected sale price, lease-up cash flow, or hold value, then test each against the cleanup finish date and the actual financing carry. One clean rule: if the site cannot clear the market by the planned exit month, owner distributions usually slip too.

- Track demand by asset type.

- Confirm entitlements before pricing.

- Watch tenant interest and LOIs.

- Compare sale, lease, and hold.

Here’s the quick math: a stronger exit only helps if the cash arrives before the carry eats it. So tie the model to the actual month of sale, not the hoped-for value, and reforecast whenever cleanup, approvals, or tenant sign-up moves.

4

Financing Structure

Financing Structure

Financing structure decides how much of the project’s profit reaches the owner after debt service, preferred returns, guarantees, and investor splits. In this model, the project can show 185% IRR and 207 ROE, but owner cash still depends on the waterfall, not just the project total. Month 39 payback means the cash stack must hold through a long carry period.

Key inputs are loan balance, interest rate, equity share, preferred return, reserve policy, guarantee terms, and hold length. Longer holds raise carry cost and reduce take-home. Here’s the quick math: if cash is trapped in reserves or paid to lenders first, project profit can look strong while owner distributions stay thin until exit.

Track the waterfall, not just IRR

Build a monthly waterfall that shows project profit versus owner share after debt service and investor payouts. Test the cash trough against the disclosed minimum cash of -$10,627M and rerun it for slower exits, higher rates, and longer remediation. If the deal needs too much carry, the owner may own a strong asset but still wait too long to get paid.

Track three controls: debt cost, distribution order, and reserve draw. Keep an eye on reimbursement lag, preferred return accrual, and reinvestment needs. Shorter hold periods, tighter reserves, and cleaner financing terms protect owner draw; longer holds do the opposite and can turn paper gains into weak cash income.

5

Overhead Discipline

Overhead Discipline

Fixed overhead of $46,200 a month keeps burning while projects wait for permits, cleanup, construction, or sale. That is $554,400 a year before payroll, so delays cut project margin and can squeeze owner pay even when the asset still has value. Idle sites are cash drains.

Payroll also climbs from $825,000 in Year 1 to $2.035M in Year 5, so the business needs a steady pipeline to support the burn. If overhead grows faster than project starts and exits, cash flow gets tight and distributions get pushed back.

Keep Burn Tied to Active Projects

Track overhead as a monthly run rate against live jobs, not just booked revenue. The key inputs are permits pending, sites in cleanup, sites in construction, legal spend, insurance, and contractor use. Keep staffing lean, use specialist contractors where needed, and cut any nonproject spend that does not move a site closer to sale.

If a project slips, trim burn fast. Review pipeline timing each month so fixed costs do not outrun the number of sites that can actually convert to cash. That is what protects owner income when sales are delayed.

6

Compare low, base, and high brownfield owner-income scenarios

Owner income scenarios

Owner income swings with exit timing, remediation variance, reserves, and overhead across a seven-project pipeline. The base model reaches Month 22 breakeven and Month 39 payback, but cash bottoms at about -$10.6M.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Owner income stays weak when projects exit later and reserves run higher than planned. | Owner income follows the modeled seven-project path with breakeven in Month 22 and payback in Month 39. | Owner income improves when cleanup variance comes in low and exits clear at stronger values. |

| Typical setup | Fewer realized gains, longer sale timing, and heavier cleanup contingency use keep cash tight. | Seven projects move through the stated acquisition, construction, and sale schedule with no major plan drift. | Projects close on time, reserves stay lean, and sale prices beat plan without new overhead. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Negative to modest incomeLow Case | Modeled owner income bandBase Case | Strong upside income bandHigh Case |

| Best fit | Use this to stress delayed exits and reserve pressure. | Use this as the core planning case for budgets and lender talks. | Use this to test upside if exits are stronger and remediation stays tight. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Brownfield Redevelopment Services Porter's Five Forces Analysis

- Brownfield Redevelopment Services BCG Matrix

- Brownfield Redevelopment Services Business Model Canvas

- What 5 KPIs Should Brownfield Redevelopment Services Business Track?

- Brownfield Redevelopment Services Business Plan Template in Pre-Written Word

- How Increase Brownfield Redevelopment Services Profitability?

- What Are Operating Costs For Brownfield Redevelopment Services?

- Brownfield Redevelopment Startup Costs: $705K CAPEX Plus Project Capital

- Brownfield Redevelopment Financial Model Template in Excel

- How To Start A Brownfield Redevelopment Company In 6 To 12+ Months

- How To Write Brownfield Redevelopment Services Business Plan?

- Brownfield Redevelopment Services Marketing Mix

- Brownfield Redevelopment Services Marketing Plan

- Brownfield Redevelopment Services Business Proposal

- Brownfield Redevelopment Services PESTEL Analysis

- Brownfield Redevelopment Services Pitch Deck Example Editable PPTX

- Brownfield Redevelopment Services Business SWOT Analysis

- Brownfield Redevelopment Services Value Proposition Canvas

Frequently Asked Questions

Owner take-home is usually back-ended and depends on exits, reserves, and capital splits In this model, EBITDA is -$9682M in Year 1, -$11619M in Year 2, and $13699M in Year 3 The $220,000 Managing Director salary is payroll distributions come later if cash remains after reserves and obligations