Owner income$1.1M-$4.6M

Owner income$1.1M-$4.6MHow Much Does a Buffet Restaurant Owner Make? $1086M EBITDA Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.1M-$4.6M  Net margin33% to 54%

Net margin33% to 54% Revenue for target pay$3.3M

Revenue for target pay$3.3M Business difficultyHard

Business difficultyHard

You’re estimating owner take-home for a US independent buffet restaurant, not a guaranteed salary This five-year planning view uses researched assumptions including 300 weekly covers in Year 1, $150 midweek and $250 weekend AOV, and $1086M Year 1 EBITDA before taxes, debt principal, reserves, and owner distributions

Owner income$1.1M-$4.6MNet margin33% to 54%Revenue for target pay$3.3MBusiness difficultyHardWant to test your buffet owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, labor, reserves, debt, and operating discipline.

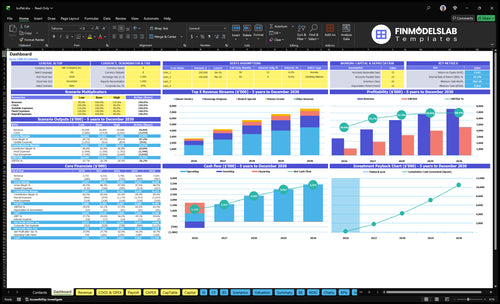

How do you check owner income in the Buffet Restaurant model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the Buffet Restaurant Financial Model Template.

Owner-income model highlights

- Owner take-home sits on dashboard

- Revenue, EBITDA, cash show clearly

- Year 1 to 5 scenarios compare

How much do food cost, labor, and waste change buffet profit?

If you're modeling a Buffet Restaurant, the biggest swing is food cost: guests choose portions, and the kitchen has to refill trays before demand is certain, so profit can move fast. For a starting point, What Is The Estimated Cost To Open And Launch Your Buffet Restaurant Business? sits behind a Year 1 model with food inventory at 90% of sales, beverage inventory at 50%, guest supplies at 15%, card fees at 25%, and payroll at $730k. Small changes in waste, batch timing, and scheduling can lift owner income, but treat any savings as sensitivity, not a guarantee.

Key cost drivers

- Food cost moves with portions.

- Waste rises with overproduction.

- Payroll is $730k in Year 1.

- Card fees add 25%.

What changes profit

- Batch timing cuts spoilage.

- Scheduling trims idle labor.

- Guest supplies add 15%.

- Use savings as sensitivity, not certainty.

Is an owner-operated buffet more profitable than a manager-run buffet?

If the owner replaces the $90k restaurant manager, a Buffet Restaurant can keep more cash, but it stops being passive income. Here’s the quick math: spreading that payroll over 300 weekly covers in Year 1 is about $5.77 per cover, and over 560 weekly covers in Year 5 it drops to about $3.09. So, owner-operated can be more profitable, but only if the owner covers shifts and keeps waste, labor, and service tight.

Owner-run payoff

- Save the $90k manager salary.

- Raise take-home if you cover shifts.

- Trade cash savings for more work.

- It is not passive income.

Scale check

- Covers rise from 300 to 560.

- Volume can offset management payroll.

- Food waste has to stay controlled.

- Service quality has to stay steady.

How much revenue does a buffet restaurant need to pay the owner?

You can’t pin this down from gross sales alone. For a Buffet Restaurant, work backward from the owner’s target pay: required sales = (target owner pay + reserves + debt service + taxes) ÷ post-cost margin. In the researched model, Year 1 carries 180% COGS and variable expenses, plus $318k in annual fixed overhead and $730k in payroll, with breakeven in Month 3 and payback in 10 months.

Owner pay math

- Start with target owner pay.

- Add reserves, debt service, taxes.

- Divide by post-cost margin.

- Model sales, not just gross margin.

Year 1 pressure

- COGS and variable costs hit 180%.

- Fixed overhead is $318k a year.

- Payroll is $730k a year.

- More reserves or debt raises sales needs.

Want the six drivers that move buffet income?

1

300-560/wkGuest volume

More covers feed the whole model; volume climbs from about 300 to 560 weekly covers across the plan, and that is the fastest way to lift owner take-home.

2

$150-$350Ticket size

Midweek tickets run $150 to $200 and weekends $250 to $350, so a better mix pushes revenue without adding seats.

3

15%-18%Food waste

Food, beverage, and variable guest costs sit around 15% to 18% of sales, so tighter prep and batch control drop cost straight to EBITDA.

4

$730K-$1.18MLabor efficiency

Payroll rises from about $730K in year 1 to $1.183M in year 5, so staffing and scheduling move profit fast.

5

$26K/moFixed overhead

Rent, utilities, marketing, systems, and support total about $25.5K a month, so low traffic still burns cash.

6

$520KOwner role

EBITDA is not spendable cash, so owner draws only make sense after the $520K month-3 buffer is safe.

Buffet Restaurant Core Six Income Drivers

Guest Volume And Seat Utilization

Guest Volume And Seat Utilization

Guest volume and seat utilization is how many covers flow through the same rent, utilities, systems, and base management. Here, weekly covers rise from 300 in Year 1 to 560 in Year 5, or about 87% more traffic. Because Monday is closed, the business has to win more demand across the other six days, with Saturday growing from 80 to 140 covers.

More covers usually lift owner income by spreading fixed cost over more checks, so gross profit and cash flow improve if food and labor stay controlled. The key inputs are covers per day, meal-period mix, seat turns, and local demand. What this estimate hides is staffing pressure: if prep, line work, and cleaning rise faster than guest count, profit per cover can slip.

Track Covers Before You Add Labor

Track covers by day, seat turns, and peak meal periods first. If Saturday is the strongest day, staff and prep for that spike, then test whether lunch and dinner can carry more volume without hurting the buffet line. One clean rule: fill seats, but do not flood labor.

- Compare covers to seats daily.

- Measure Saturday separately.

- Watch labor hours per cover.

- Cut prep waste before adding staff.

If guest count climbs slower than labor and production, the extra sales won’t reach owner pay. Keep a weekly dashboard on covers, seat turns, labor hours, and food output by meal period. That shows whether each added guest is improving fixed-cost absorption or just adding noise.

1

Average Ticket And Pricing Power

Average Ticket And Pricing Power

In a buffet, average ticket is the price per cover, so revenue starts with pricing before guests change what they eat. Here, midweek ticket rises from $150 to $200 and weekend ticket from $250 to $350 over five years, while beverage mix moves from 250% to 290% and private events from 50% to 90%.

That raises revenue per seat and can lift owner pay without adding the same number of covers. The risk is simple: if price outruns perceived value or local competition, traffic falls and cash flow weakens. Watch guest count, day pricing, beverage attach rate, and private-event mix together.

Track Price By Day, Not By Feel

Measure covers, ticket by weekday, beverage sales, and private-event bookings every week. Here’s the quick math: a weekend move from $250 to $350 adds $100 per cover before food behavior changes, so it can improve profit faster than chasing more seat turns if traffic holds.

Test small price steps against guest reviews and repeat visits. If weekend covers soften after a change, you’ve likely crossed the value line. Keep the buffet premium, but stay close to what local diners will pay so higher ticket turns into real take-home income, not just higher posted revenue.

2

Food Cost, Waste, And Menu Mix

Food Cost And Menu Mix

Food cost control is a margin story, not a traffic story. Here, food inventory means ingredient spend, spoilage, tray waste, and guest portion behavior. If food inventory improves from 90% to 80% of sales, that frees 10% of sales for profit; at $100,000 in sales, that is $10,000 back to gross margin and owner draw.

Waste is not a separate line, so it sits inside food inventory and ops sensitivity. Beverage inventory improving from 50% to 40% adds another margin lift. Smaller batch refills near close and lower-waste menu design protect cash flow, but trays that look too thin can trigger complaints and hurt repeat visits.

Control Batches And Waste

Track food cost by meal period, then compare it with covers, refill timing, and spoilage. Here’s the quick math: sales × 10% is the margin swing if food inventory moves from 90% to 80%. That is the number that tells you whether menu mix and batch size are helping owner income.

- Covers by meal period

- Tray refills near close

- Spoilage and leftover pans

- Beverage mix and take rate

If complaints rise when trays look thin, increase refill frequency instead of letting portions drift. The goal is steady presentation with less overproduction, so more sales turn into cash after ingredients, payroll, and fixed overhead.

3

Labor Scheduling And Service Efficiency

Labor Scheduling And Service Efficiency

Self-service cuts some table work, but buffet labor still has to cover prep, replenishment, bussing, dishwashing, cashiering, cleaning, and management. With payroll rising from $730k in Year 1 to $1.183M in Year 5, profit depends on keeping labor hours in step with covers, not just filling the room.

The key roles are a $150k executive chef, a $90k restaurant manager, service staff from 40 to 80 FTE, and kitchen staff from 30 to 60 FTE. If slow midweek shifts are overstaffed, EBITDA per cover drops fast. Owner labor should be tracked separately from paid labor so profit and draw stay clear.

Control Labor By Cover Count

Track labor against covers by daypart, not just weekly payroll. The clean test is labor hours per cover, split by midweek, weekend, brunch, and dinner. That shows where staff is too heavy for the traffic and where service is thin.

- Log covers, hours, and FTE by shift.

- Separate owner hours from payroll.

- Trim slow midweek staffing first.

- Protect prep, bussing, and replenishment.

Here’s the quick math: if payroll keeps climbing but cover counts do not, margin gets squeezed before cash shows up in the bank. The fix is tighter schedules, cross-trained staff, and manager coverage matched to the busiest meal periods.

4

Fixed Overhead And Facility Cost Pressure

Fixed Overhead Pressure

Large buffet rooms keep burning cash on slow days, so owner income depends on how fast sales absorb fixed costs. The disclosed monthly fixed overhead is $265k, including $15k rent, $35k utilities, $12k insurance, $25k marketing, $800 systems, $1k professional services, $18k cleaning and maintenance, and $700 security.

The key metric is fixed cost as a share of sales. The disclosed annual fixed overhead is $318k, so weak traffic keeps profit thin and can block owner pay. When covers rise and the room fills, the same overhead is spread across more sales and income improves fast.

Track Burn Rate by Mo nth

Measure monthly fixed costs against sales, not just against budget. Track covers, revenue, and each overhead line every month, then compare the total to sales mix. If sales lag while fixed costs stay flat, cash flow tightens before food or labor fixes can save profit.

Match space to demand and keep a close eye on the room as traffic matures. One clean test: when sales rise faster than fixed overhead, more cash can reach owner pay; when they don’t, the business is just funding an empty dining room.

5

Owner Role, Management, And Reserves

Owner Draw And Reserve Discipline

Owner pay here is not passive. With a $90k restaurant manager on payroll, the owner’s draw still depends on shift coverage, oversight, debt service, repairs, taxes, and how much cash stays in the business. EBITDA (earnings before interest, taxes, depreciation, and amortization) is only a starting point; it is not all spendable.

The safety check is liquidity. Startup capex is $610k, and minimum cash need reaches $520k in Month 3. If reserves are thin, owner draw should stay low even when sales look fine, because cash has to cover repairs, tax bills, and debt payments first. Owner pay follows cash, not paper profit.

Fund Reserves Before Draws

Measure draw after a cash floor, not after reported profit. Start with monthly cash flow, then set a reserve policy for debt service, tax set-asides, and repairs. If the owner works shifts, track whether that labor replaces paid hours or just adds cost. The goal is safer take-home, not bigger early withdrawals.

Keep one simple rule: pay the owner only after reserves are funded.

- Track monthly cash floor.

- Forecast debt and tax dates.

- Approve draws after reserves.

- Document owner shift coverage.

- Review repair spend weekly.

6

Compare low, base, and high buffet owner income scenarios

Owner income scenarios

Owner income moves with weekly covers, average check, and the cost load from food, drinks, and labor. Higher traffic and better mix lift EBITDA fast, but payroll and rent stay heavy.

| Scenario | Low CaseDownside | Base CaseBase | High CaseUpside |

|---|---|---|---|

| Launch model | This is the slower earnings path with lower traffic, lower checks, and enough volume to cover the core fixed base. | This is the modeled run rate with steady midweek and weekend demand and a balanced mix of sales lines. | This is the stronger earnings path with fuller dining rooms, higher checks, and better spread across drinks and events. |

| Typical setup | About 300 weekly covers with $150 midweek and $250 weekend checks, 18.0% food and variable load, and a leaner staffing base. | About 470 weekly covers with $180 midweek and $310 weekend checks, 16.6% food and variable load, and the planned staffing base. | About 560 weekly covers with $200 midweek and $350 weekend checks, 15.0% food and variable load, and the highest staffing plan. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.1MYear 1 case | $3.3MYear 3 case | $4.6MYear 5 case |

| Best fit | Use this to stress-test a soft opening, weaker weekday demand, or a slower ramp in private events. | Use this as the main planning case for budgets, debt, and owner draws. | Use this to test what happens if the room runs hot and beverage and event sales outpace plan. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets; taxes, reserves, debt service, and owner draws can reduce cash paid out.

Related Products

- Buffet Restaurant Porter's Five Forces Analysis

- Buffet Restaurant BCG Matrix

- Buffet Restaurant Business Model Canvas

- 7 Core KPIs to Track for Your Buffet Restaurant

- Buffet Restaurant Business Plan Template in Pre-Written Word

- Increase Buffet Restaurant Profitability: 7 Essential Financial Strategies

- How Much Does It Cost To Operate A Buffet Restaurant Monthly?

- How Much Does It Cost To Open A Buffet Restaurant? $113M Plan

- Buffet Restaurant Financial Model Template in Excel

- How To Open A Buffet Restaurant: 4-9 Month Launch Plan

- How to Write a Buffet Restaurant Business Plan in 7 Steps

- Buffet Restaurant Marketing Mix

- Buffet Restaurant Marketing Plan

- Buffet Restaurant Business Proposal

- Buffet Restaurant PESTEL Analysis

- Buffet Restaurant Pitch Deck Example Editable PPTX

- Buffet Restaurant Business SWOT Analysis

- Buffet Restaurant Value Proposition Canvas

Frequently Asked Questions

A buffet restaurant can be profitable when guest volume covers labor, rent, waste, and reserves In the researched case, EBITDA is $1086M in Year 1 and $4567M in Year 5 That is operating profit before taxes, debt principal, reinvestment, and owner distributions, so it is not the same as guaranteed take-home pay