Owner income$120k

Owner income$120kHow Much Does a Building Maintenance Company Owner Make? $120K Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k  Net margin-61% to 51%

Net margin-61% to 51% Revenue for target pay$474k

Revenue for target pay$474k Business difficultyHard

Business difficultyHard

Key Takeaways

- Recurring contracts help cover $8,300 in monthly overhead.

- Pro and Elite work raise revenue per account.

- Higher technician utilization improves gross profit, not just payroll.

- Dense routes cut drive time and protect margins.

Owner income$120kNet margin-61% to 51%Revenue for target pay$474kBusiness difficultyHardWant to test your building maintenance owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income changes with revenue, margins, payroll, debt, reserves, and taxes. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Building Maintenance model?

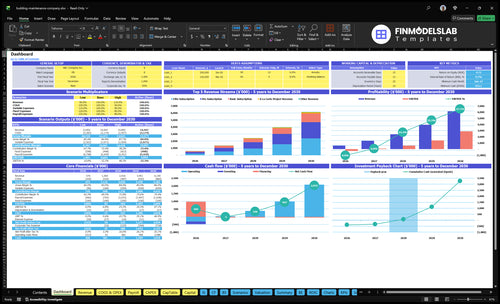

The Building Maintenance Financial Model Template ties dashboard, revenue, labor, COGS, and cash flow to owner pay; it also shows $165,000 capex, $50,000 Year 1 marketing, $500 CAC, $435,000 minimum cash, Month 18 breakeven, and 38-month payback. Open the model to see the full links.

Owner-income model highlights

- Owner pay and reserves

- Revenue, EBITDA, cash

- Scenarios, breakeven, payback

How much revenue does a building maintenance company need to pay the owner?

There’s no universal revenue number for Building Maintenance, because owner pay depends on margin, overhead, and crew costs. In this model, Year 1 revenue of about $474,000 still leaves -$289,000 EBITDA after payroll, overhead, marketing, and a $120,000 owner salary. By Year 2, implied revenue of about $1.204 million supports about $93,000 EBITDA, with 74% to 75% contribution margin and $99,600 of fixed overhead.

Year 1 pressure

- $474,000 implied revenue

- -$289,000 EBITDA after costs

- $120,000 owner salary included

- 74% contribution margin

Year 2 support

- $1.204 million implied revenue

- $93,000 EBITDA with same pay

- 75% contribution margin

- $99,600 fixed overhead yearly

How much can a building maintenance company owner make?

A Building Maintenance owner can make a $120,000 annual CEO/founder salary in this model, but true take-home depends on profit and cash timing; What Is The Most Important Indicator Of Success For Building Maintenance? explains the KPI side. Owner income has two parts: wages for replacing labor and profit distributions, which are not guaranteed.

Income Model

- $120,000 salary from Month 1

- -$289,000 EBITDA in Year 1

- $93,000 EBITDA in Year 2

- $564,000 EBITDA in Year 3

Profit Reality

- $1.403 million EBITDA in Year 4

- $2.894 million EBITDA in Year 5

- Owner-operator work can raise early pay

- Crew model needs payroll and reserves

Is a building maintenance company profitable as it scales?

Building Maintenance can be profitable as it scales, but only after it survives early payroll, vehicles, tools, marketing, and working-capital strain. The model’s breakeven is around Month 18, needs about $435,000 in minimum cash, and shows a 38-month payback. As it grows, it adds technicians, lead technicians, operations managers, sales, and admin; that improves control with supervisors and systems, but overhead also rises, and slow-paying or poorly scoped accounts can drain cash fast.

Why it can work

- Month 18 breakeven target

- $435,000 minimum cash need

- 38-month payback period

- Recurring accounts steady revenue

What can hurt cash

- Early payroll hits hard

- Vehicles and tools cost cash

- Poor scopes shrink margin

- Slow payers drain working capital

Want the six building maintenance profit drivers?

1

100-714 acctsRecurring Volume

Year 1 marketing spend of $50K at a $500 CAC can buy about 100 accounts, and Year 5 can support about 714 at $350 CAC, so contract adds drive the whole model.

2

$500-$2.8KPricing Mix

The monthly price ladder runs from $500 Basic to $2,800 Elite by Year 5, so shifting more work into higher tiers lifts owner take-home fast.

3

2-10 FTETechnician Utilization

Maintenance tech staffing grows from 2.0 FTE to 10.0 FTE, so tight scheduling is what turns payroll into billed work instead of idle cost.

4

26%Labor Control

Direct labor and materials start at 26% of revenue in Year 1, so every point saved on subcontractors, supplies, fuel, and commissions drops straight to income.

5

5%-4%Route Density

Vehicle operating cost falls from 5.0% to 4.0% of revenue by Year 5, and denser routes help you keep that gap from widening.

6

$500-$350Retention Renewals

CAC falls from $500 to $350, so renewals matter because losing repeat accounts forces you to buy growth back at a higher cost.

Building Maintenance Core Six Income Drivers

Recurring Contract Volume

Recurring Contract Volume

Recurring contracts give this business predictable monthly revenue, which is what pays payroll, owner draws, and reserves. With fixed overhead at $8,300 per month, contract count and average monthly contract value matter more than one-off jobs because they set the cash base before repairs hit.

Here’s the quick math: 17 Basic accounts at $500 cover about $8,500 a month, 7 Pro accounts at $1,200 cover $8,400, and 4 Elite accounts at $2,500 cover $10,000. One clean line: more stable contracts mean less sales pressure.

Track Monthly Coverage

Measure contract count, average monthly contract value, billing consistency, and renewal rate. Use the mix to forecast owner income, because missed renewals or late billing can turn a healthy book into a cash squeeze fast.

- Basic: $500 monthly

- Pro: $1,200 monthly

- Elite: $2,500 monthly

- Risk: underpriced scope

What this estimate hides: if scope creeps but price stays flat, the contract can become a recurring loss. Protect margin by documenting response times, exclusions, and emergency call rules before you sign.

1

Pricing And Service Mix

Pricing and Service Mix

Your income rises when the mix shifts from low-tier accounts to higher-tier work. Year 1 uses 40% Basic at $500, 30% Pro at $1,200, 15% Elite at $2,500, plus 10% project work and 5% emergency risk. More Pro and Elite work lifts revenue per account and owner pay, but emergency calls need a surcharge or they burn labor capacity and squeeze margin.

Price for scope, not just time

Track revenue by tier, project dollars, and emergency surcharge collected. Price by scope, response time, and materials, then compare each job’s gross margin to the plan. If after-hours calls or extra visits are common, raise the fee or split them into a project line item so the subscription base keeps its cash flow.

- Measure mix by tier monthly.

- Bill emergency work separately.

- Push upgrades to Pro and Elite.

2

Technician Utilization

Technician Utilization

Technician utilization is the share of paid field time that turns into billable work. It includes billable hours, callbacks, idle time, schedule gaps, and drive time. With $180,000 in Year 1 direct field payroll for one lead technician and two maintenance technicians, low utilization turns payroll into overhead and cuts gross profit before owner draws.

By Year 5, direct field payroll reaches $760,000, so wasted time gets expensive fast. If paid hours do not become invoiceable work, the owner pays more labor but keeps less cash. Better scheduling, tighter dispatch, and fewer callbacks lift gross profit first, which is what creates room for owner take-home pay.

Measure Billable Time First

Track billable hours ÷ paid field hours each week, then split the gap into drive time, idle time, and callbacks. That tells you where payroll is leaking. If a tech looks busy but is not billable, the labor cost still hits margin, so the schedule is not pulling its weight.

Use route grouping, clear job blocks, and fast callback review to fill schedule gaps. Watch these inputs: billable hours, callbacks, idle time, schedule gaps, and drive time. When that mix improves, more of the wage dollar supports gross profit before owner distributions.

- Measure billable hours weekly.

- Separate drive time from work time.

- Track callbacks by technician.

- Fill gaps before adding headcount.

3

Labor And Subcontractor Cost Control

Labor Cost Control

Payroll, overtime, subcontractors, and supervisors can wipe out profit if jobs are priced off sales, not true labor cost. In this model, subcontractors fall from 10% of revenue in Year 1 to 8% in Year 5, while total payroll rises from $490,000 to $1,260 million as stated. If direct labor is not split from overhead payroll, EBITDA gets squeezed fast and owner pay gets less reliable.

Track Direct Labor Weekly

Measure technician payroll, lead technician payroll, subcontractor percent, overtime hours, and supervisor load by job type. Here’s the quick math: if labor runs high on recurring work, the subscription fee is too low or the scope is too broad. Keep direct labor separate from overhead payroll so you can see which accounts pay their way.

- Track billable hours by tech

- Flag overtime on each job

- Review subcontractor share monthly

- Price emergency work separately

4

Route Density And Travel Time

Route Density

Dense routes cut windshield time, fuel, vehicle wear, and unbillable labor. For a maintenance crew, the key inputs are jobs per route, drive minutes, same-area accounts, and dispatch efficiency. When accounts are clustered, more paid work fits into each day, so the same technician payroll produces more billable service and better owner take-home.

The money leak is distance. Chasing far-apart accounts raises payroll and fuel without adding matching billings, so margin gets thinner fast. Vehicle operating costs are 5% of revenue in Year 1 and 4% by Year 5, so route planning matters most when you’re trying to protect cash and pay the owner from recurring profit.

Cluster by Zip Code

Track jobs per route, drive minutes, and fuel cost by technician each week. Put same-area accounts on the same day, then watch whether route time drops and billable hours rise. If a new account adds long drive time, price it higher or pass unless it fills a dense gap.

Build the schedule around geography, not just urgency. Here’s the quick math: more stops per route means less dead time, which lowers vehicle cost as a share of revenue and leaves more gross profit for reserves and owner pay. If dispatch is loose, the business can look busy while take-home income stays flat.

- Track accounts by zip and route.

- Record drive minutes per job.

- Flag low-density accounts fast.

5

Retention And Renewals

Retention and Renewals

When accounts renew, the owner keeps recurring revenue without reopening the sales funnel. That lowers sales pressure and helps cover fixed overhead like the $8,300 monthly b ase cost. The key metrics are renewal rate, payment reliability, and margin by account, because one strong contract can fund payroll while a weak one quietly drains cash.

Here’s the quick math: replacing a lost account wastes the onboarding cost again, even when CAC drops from $500 in Year 1 to $350 in Year 5. Slow payers and loose scopes also hurt cash flow and crew planning. If a contract keeps growing without a price increase, scope creep can turn a “good” customer into a low-margin one fast.

Track Renewals by Profit, Not Just Volume

Measure each account’s renewal probability, days late, added work, and price lift at renewal. Use margin by account after labor, materials, and subcontractors, so you can see which contracts actually pay owner draw. One clean rule: renew the work that pays on time and prices up cleanly.

- Track renewal rate by contract type

- Watch overdue balances and late payers

- Reprice after scope changes

- Drop weak-margin accounts early

Better account quality protects staffing plans and reserve levels. If onboarding takes cash but the client won’t renew, the owner pays twice: once to win the job and again to replace it. Stable renewals reduce that leak and make take-home income steadier.

6

Compare low, base, and high building maintenance owner-income scenarios

Owner income scenarios

Income shifts with contract ramp, labor coverage, and service mix. Early cash is tight, then owner pay improves as recurring work and margin hold up.

| Scenario | Low CaseCash risk | Base CaseOwner role | High CaseMargin strength |

|---|---|---|---|

| Launch model | Owner income starts light because contract ramp is slow and labor gaps pressure cash. | Owner income follows the modeled path with a $120,000 salary and breakeven around Month 18. | Owner income rises faster when contract density improves and recurring work shifts toward Pro and Elite mix. |

| Typical setup | The business leans on smaller jobs, higher subcontractor use, and delayed owner pay while fixed costs stay in place. | The model supports $435,000 minimum cash, a 38-month payback, Year 1 EBITDA of -$289,000, and Year 2 EBITDA of $93,000. | The business runs with stronger pricing power, lower variable cost percentages, and faster EBITDA growth toward Year 5 at $2.894 million. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Delayed owner drawDraw delay risk | $120,000Owner salary path | $120,000+Higher owner draw |

| Best fit | Use this to stress test tight cash and a slower start. | Use this as the core operating case for planning pay and cash. | Use this to test upside if operations stay tight and repeat work grows. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Building Maintenance Porter's Five Forces Analysis

- Building Maintenance BCG Matrix

- Building Maintenance Business Model Canvas

- 7 Critical KPIs for Building Maintenance Success

- Building Maintenance Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Building Maintenance Profitability and Margins

- Analyzing the Monthly Running Costs for a Building Maintenance Business

- Building Maintenance Startup Costs: $165K CAPEX And $435K Cash

- Building Maintenance Financial Model Template in Excel

- How To Start A Building Maintenance Business In 4–8 Weeks

- How to Write a Building Maintenance Business Plan (7 Steps)

- Building Maintenance Marketing Mix

- Building Maintenance Marketing Plan

- Building Maintenance Business Proposal

- Building Maintenance PESTEL Analysis

- Building Maintenance Pitch Deck Example Editable PPTX

- Building Maintenance Business SWOT Analysis

- Building Maintenance Value Proposition Canvas

Frequently Asked Questions

Plan for a serious reserve, not just one month of bills This model shows a $435,000 minimum cash need, with the lowest point around Month 18 That reflects early payroll, $165,000 of startup capex, $50,000 Year 1 marketing, and losses before breakeven Cash protects payroll and response quality