Owner income-$262k

Owner income-$262kHow Much Does A C2B Platform Owner Make? $150K Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$262k  Net margin-89% to 17%

Net margin-89% to 17% Revenue for target pay$865k

Revenue for target pay$865k Business difficultyHard

Business difficultyHard

A C2B platform owner can plan around a $150,000 CEO salary in this model, but early take-home is not supported by operating profit First-year revenue is $303,575, while EBITDA after planned payroll is about -$411,500 In the mature-year case, the platform processes $483 million of GMV and produces about $132 million of revenue, with roughly $96 million of operating profit after payroll before taxes and reserves These are planning assumptions, not guaranteed earnings or distributions

Owner income-$262kNet margin-89% to 17%Revenue for target pay$865kBusiness difficultyHardWant to test your C2B platform owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the C2B Platform model?

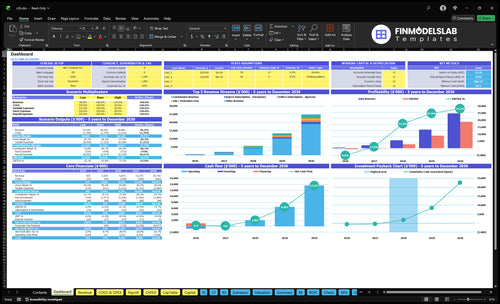

The screenshot shows assumptions, GMV build, revenue, margins, runway, scenarios, and owner pay in the C2B Platform Financial Model Template.

Owner-income model highlights

- CEO pay: $150,000

- $747,500 year-one GMV

- $303,575 year-one revenue

- $483M mature-year GMV

- Revenue versus EBITDA chart

- Scenario outputs and runway

When can a C2B platform owner pay themselves?

A C2B Platform owner can pay themselves only after acquisition, technology, support, trust and safety, payroll, reserves, and reinvestment are funded; What Is The Main Goal Of Your C2B Platform? should tie that pay decision to cash flow, not ego. In the first-year model, $303,575 revenue still lands at about -$411,500 EBITDA, a proxy for operating cash profit, after planned payroll, so distributions are not supported even if the target CEO salary is $150,000.

Pay later

- Fund customer acquisition first

- Cover technology and support

- Protect trust and safety

- Keep cash reserves intact

Pay capacity

- Year 1 revenue: $303,575

- Year 1 EBITDA: -$411,500

- Planned CEO salary: $150,000

- Mature operating profit: about $96 million

Can a C2B platform be profitable at small scale?

At the modeled numbers, a C2B Platform is not comfortably profitable at small scale: first-year revenue is $303,575, while acquisition spend is $125,000, fixed overhead is $87,600, and planned payroll is $460,000. An owner-operated version can cut payroll pressure, but the founder then absorbs support, verification, and dispute work. Hiring adds capacity, but take-home stays tight until transaction density catches up, and reserves should come before distributions.

Small-scale math

- $303,575 first-year revenue

- $125,000 acquisition budget

- $87,600 fixed overhead

- $460,000 planned payroll

What changes the outcome

- Owner-run model cuts payroll pressure

- Founder absorbs support work

- Automation must beat 30% support cost

- Buyer retention must improve first

How much GMV does a C2B platform need to pay the owner?

Owner pay has to come from GMV after take rate, fixed fees, subscriptions, payroll, and reserves. In the C2B Platform model, first-year GMV is $747,500 and revenue is $303,575, but EBITDA is still negative after payroll, so there’s not enough cash flow to pay the owner well yet. By the mature year, GMV reaches $483 million with about $132 million in revenue, and owner pay becomes possible only if buyer conversion, repeat orders, and AOV hold up.

First year

- $747,500 GMV is too small

- $303,575 revenue still misses profit

- EBITDA stays negative after payroll

- Owner pay needs outside capital

Mature year

- $483 million GMV supports scale

- $132 million revenue drives cash flow

- Enterprise AOV can hit $7,000

- No universal GMV threshold works

Want to see the main C2B platform income drivers?

1

$747K-$483MGMV

Gross merchandise value (GMV) sets the fee pool, so more order value quickly lifts owner income.

2

12%-10%Take Rate

A better mix of commissions and subscriptions raises revenue on each order without adding much cost.

3

$80-$150Buyer CAC

Buyer acquisition cost falling from $150 to $80 shortens payback and keeps paid demand from eating margin.

4

$160-$250Seller Supply

Stronger seller fit and reliable fulfillment keep completed orders high, so each seller brings more revenue per dollar spent.

5

3.4%-5%Margin Leak

Payment fees, support, refunds, and disputes can trim 3.4% to 5.0% of revenue, and that loss hits cash fast.

6

$460K-$520KPayroll

Payroll and automation decide how much gross profit survives, so lean headcount matters as volume scales.

C2B Platform Core Six Income Drivers

GMV And Transaction Volume

GMV and Transaction Volume

Owner income starts with completed paid activity, not registrations or listings. In year one, GMV is $747,500 across 655 completed orders; at maturity, it reaches $483 million and 19,875 orders. The mix matters: startup average order value (AOV) rises from $500 to $700, SMB from $1,500 to $1,900, and enterprise from $5,000 to $7,000.

Liquidity means buyers can find reliable sellers fast. If that breaks, paid orders slow and GMV stalls even when signups look healthy. GMV is the sales base that fees are charged on, so weak volume cuts commission revenue, cash flow, and owner pay. The inputs that matter are buyer mix, repeat orders, and AOV. No paid jobs, no owner draw.

Track Liquidity, Not Signups

Track completed orders, repeat purchase rate, and AOV by segment. GMV only improves when interest becomes paid work, so a heavier share of $1,900 SMB and $7,000 enterprise orders can lift revenue faster than more listings.

- Completed paid orders

- Repeat orders by segment

- AOV by buyer type

- Seller depth in key categories

Watch supply depth in the busiest categories and fix gaps first. If buyers wait or bounce, conversion falls and cash flow slips. Keep the goal simple: more matched orders per buyer, not more inactive accounts.

1

Take Rate And Monetization Mix

Take Rate And Monetization Mix

The income driver is the fee stack on each completed order: gross merchandise value (GMV) times the platform’s kept share, plus a fixed fee per order, plus subscriptions, ads, promotion fees, and payment-related fees. In the model, variable commission falls from 120% in year one to 100% in the mature year, while fixed commission rises from $5 to $7 per order.

Year-one subscriptions already add $81,600 from sellers and $129,000 from buyers, or $210,600 before ads and payment fees. This helps owner income only if the fee load does not slow conversion. Higher fees can lift gross margin, but they can also hurt buyer conversion, seller retention, and competitive position.

Track fee yield per order

Measure revenue per completed order, subscription attach rate (the share of users who pay), and churn by buyer and seller segment. If fee changes raise revenue but cut repeat orders, owner draw can fall even when topline looks better. Keep ads, promotion fees, and payment fees editable so you can test price moves without guessing.

Watch the trade-off on the fixed fee closely: moving from $5 to $7 helps only if order volume holds. If renewal softens or onboarding slows, back off fast and protect cash flow, because this monetization mix only works when buyers keep buying and sellers keep listing.

2

Business Buyer Acquisition And Retention

Buyer Acquisition Cost

When the platform pays to acquire buyers, owner income depends on whether those buyers place enough repeat orders to cover CAC (customer acquisition cost). At $75,000 in buyer marketing and $150 CAC, the model gets about 500 buyers; the supplied growth path later shows $10 million, $80 CAC, and 12,500 buyers. If orders do not repeat, paid traffic turns into cash burn fast.

The key inputs are buyer budget, CAC, segment mix, repeat orders, and completed order count. Repeat order frequency improves from 15 to 19 for startups, 12 to 16 for SMBs, and 8 to 12 for enterprises. That matters because more repeat buying lowers acquisition pressure per order and protects contribution margin, which is what ultimately funds owner pay.

Track payback by buyer segment

Measure CAC, repeat orders, and payback by startup, SMB, and enterprise. The quick test is simple: does each acquired buyer generate enough completed orders to earn back the initial $80 to $150 acquisition cost?

- Track CAC by channel.

- Track repeat orders monthly.

- Pause spend if payback slips.

3

Seller Supply Quality And Onboarding

Seller Supply Quality And Onboarding

Weak seller onboarding turns GMV into margin leakage. The owner’s income depends on qualified sellers who convert, fulfill on time, and keep buyers buying again; in this model, seller CAC improves from $250 to $160, but the seller acquisition budget also rises from $50,000 to $750,000, so bad supply quality gets expensive fast.

Use seller count, approval rate, activation rate, refund rate, dispute rate, and support tickets to estimate this driver. Better profiles, verification, and delivery standards cut rework and protect margin. If sellers look good on paper but fail delivery, cash still leaves the business and owner pay drops.

Track Seller Quality Before You Scale Spend

Start with a tight gate: verify identity, work samples, and service standards before activation. One clean seller is worth more than five cheap signups. Track activated sellers, first-job completion, on-time delivery, refunds per seller, and support tickets per 100 orders.

- Approve complete profiles only.

- Verify skills before launch.

- Measure refunds by seller.

- Watch disputes per order.

- Cut tickets before scaling CAC.

With seller CAC at $160, every seller who never transacts pushes payback out. As the acquisition budget scales from $50,000 to $750,000, small quality leaks can wipe out contribution margin and slow the owner’s ability to take money out of the business.

4

Payment Fees, Refunds, And Disputes

Payment Fees, Refunds, and Disputes

This driver is the cash lost between gross sales and what the owner keeps after payment processing, refunds, chargebacks, hosting, ads, and support. The model assumes payment processing falls from 30% in year one to 22% in mature year, cloud hosting from 20% to 12%, digital advertising and content from 60% to 40%, and scalable support from 30% to 22%.

Refund and chargeback rates are not supplied, so the forecast needs editable allowances. On $483 million GMV, every extra 1% of leakage cuts about $4.83 million before owner pay. Small loss rates matter because they scale with GMV.

Track Leakage Per Order

Measure GMV, order count, AOV, processing fee rate, refund rate, chargeback rate, and dispute support cost. Then compare leakage as a percent of GMV by buyer segment, because a high-ticket order can hide more damage per ticket even when volume looks fine.

- Set a refund reserve in the model.

- Track chargebacks by seller.

- Review fees by payment method.

Use clear refund rules, seller checks, and fast dispute handling to keep cash from leaking out. If the model skips refunds and chargebacks, owner pay is overstated. Test leakage at 1%, 2%, and 3% of GMV so you can see how fast profit moves.

5

Operating Structure And Automation

Fixed Cost Load

$7,300 a month of overhead is only $87,600 a year, but payroll is the real drag on owner take-home. With $460,000 in first-year payroll, total fixed operating cost is about $547,600; in fully staffed years, it rises to $607,600.

That structure means contribution must clear fixed cost before the owner gets paid. The planned team includes a CEO at $150,000, CTO at $140,000, Head of Product at $120,000 after year one, and a Lead Engineer at $110,000. Hire too early, and distributions get pushed back fast.

Automate Before You Hire

Track support tickets, compliance hours, and payroll run rate monthly. The win is simple: if automation cuts repetitive support and compliance work, the platform can hold headcount flat longer and keep more contribution available for owner pay.

Use a hiring gate tied to volume and workload, not hope. Founder savings can fund speed, but they also raise execution risk if growth slows. One clean rule: do not add a full-time role until automation has already removed a meaningful share of manual work and the forecast still covers $547,600 in year-one fixed cost.

6

Compare lean, base, and high C2B platform income scenarios

Owner income scenarios

Seller and buyer mix drive owner income here because commissions, subscriptions, and payroll scale at different speeds. Owner take-home still depends on reserves, taxes, reinvestment, and lender limits.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the downside earnings path, with Year 1 still negative and owner pay limited. | This is the modeled middle path, where volume and fees turn EBITDA positive. | This is the stronger path, where mature-year scale supports larger owner draws. |

| Typical setup | The business is still in the heavy-build phase, with $125,000 acquisition spend, $460,000 payroll, and 655 orders. | This is the scaled middle case, with $700,000 acquisition spend, $520,000 payroll, and 5,309 orders. | This is the mature case, with 19,875 orders, $175,000 acquisition spend, and $520,000 payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Negative drawLow Case | Six-figure drawBase Case | Seven-figure drawHigh Case |

| Best fit | Use this to stress test cash and founder pay if growth comes slower than planned. | This is the main budgeting case for planning founder pay, reserves, and reinvestment. | Use this to test upside if enterprise buyers and repeat orders scale faster. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- C2B Platform Porter's Five Forces Analysis

- C2B Platform BCG Matrix

- C2B Platform Business Model Canvas

- Track Key Performance Indicators for C2B Platform Growth

- C2B Platform Business Plan Template in Pre-Written Word

- 7 Strategies to Increase C2B Platform Profitability and Scale

- Running Costs for a C2B Platform: How Much Does It Cost Monthly?

- C2B Platform Startup Costs: Plan For $200k+ In Launch CAPEX

- C2B Platform Financial Model Template in Excel

- How To Start A C2B Platform In 10–20 Weeks With First Buyers

- How to Write a C2B Platform Business Plan in 7 Steps

- C2B Platform Marketing Mix

- C2B Platform Marketing Plan

- C2B Platform Business Proposal

- C2B Platform PESTEL Analysis

- C2B Platform Pitch Deck Example Editable PPTX

- C2B Platform Business SWOT Analysis

- C2B Platform Value Proposition Canvas

Frequently Asked Questions

The model includes $150,000 of planned CEO pay, but profit-funded take-home is not realistic in the first year First-year revenue is $303,575 and EBITDA after payroll is about -$411,500 In the mature year, revenue reaches $132 million and EBITDA after payroll is about $96 million before taxes and reserves